This was a round trip for us:

We started this journey at $44. The stock exactly hit our downside target with a ~35% drop, and now is right back to where we started. We couldn’t (and still can’t) get comfortable with the LONG so we left it on, even though we highlighted that sales should accelerate in 1H19 and that the strategy would be to short any bounces. In hindsight, we should have taken the stock off then. A lesson for us in risk-management. No matter – with one more sales acceleration quarter ahead (March-Q Report, June-Q guide) we can step to the side for now. For those paying attention...the stock is back to expensive at 9x EV/S with no path to FCF being supportive for valuation in the next 24 months.

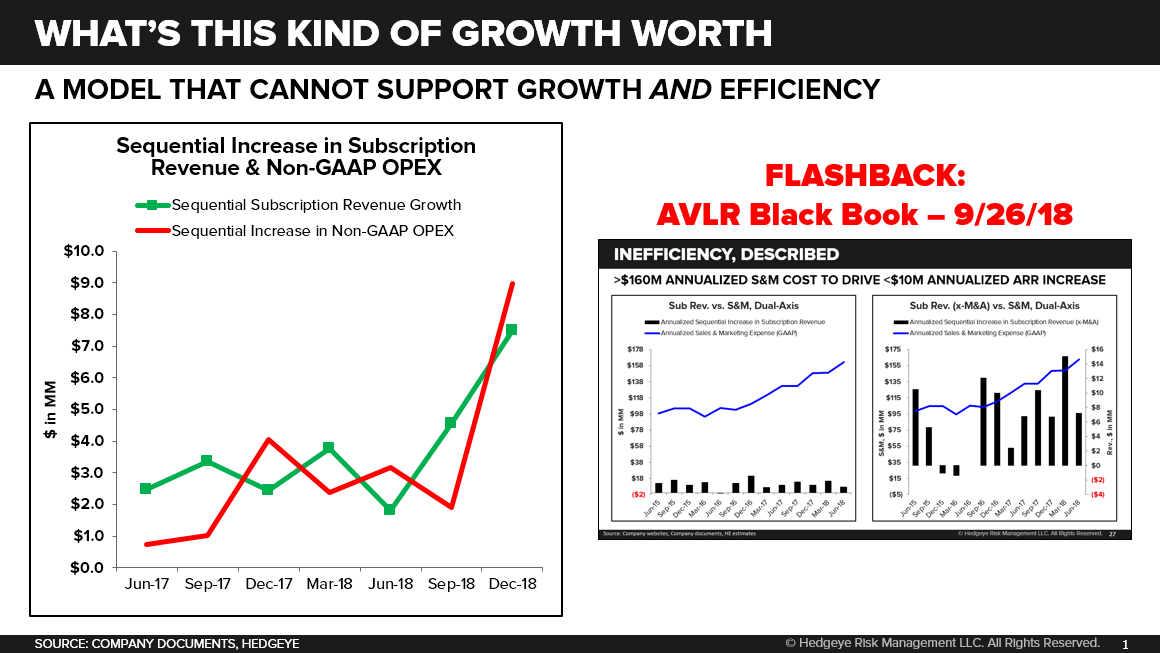

Our bearish view of Avalara is reaffirmed by, among many other things (like sales inefficiency and lack of tech prowess), the company’s M&A strategy – which sort of reveals the whole joke. On the one hand, AVLR bought an alcohol license company and claimed that many of its own customers (who by the way, are mostly won thanks to an ERP refresh cycle) are naturally demanding help with obtaining their alcohol licenses (does anyone else see the joke in that?). And its other recent acquisition of Indix, which management touted has “changed the game” – clearly has not, having been shut down as a product after once boasting to having revolutionized the state of retail… But more important is that Indix’s technology is something that AVLR should have built from the beginning, that is, if they were actually a technology company – and whose existence (in droves of similar startups) shows that the arbitrage of taking publicly available tax laws and running “multiplication” for clients will not be a high dollar draw forever. In other words, if new generation companies can do this with automation, they will get there faster, cheaper, and a heck of a lot more efficiently than Avalara. If all else fails, at least AVLR can help customers apply for their liquor license. With that in mind, we’ll pour ourselves a cold one and revisit AVLR in the summer. We see ~$8 of upside risk, ~$14 downside risk, with the accel we will hope for closer to the top of this range to revisit.

Please call or e-mail with any questions.

Ami Joseph

Managing Director

Yosef Vaitsblit

Analyst