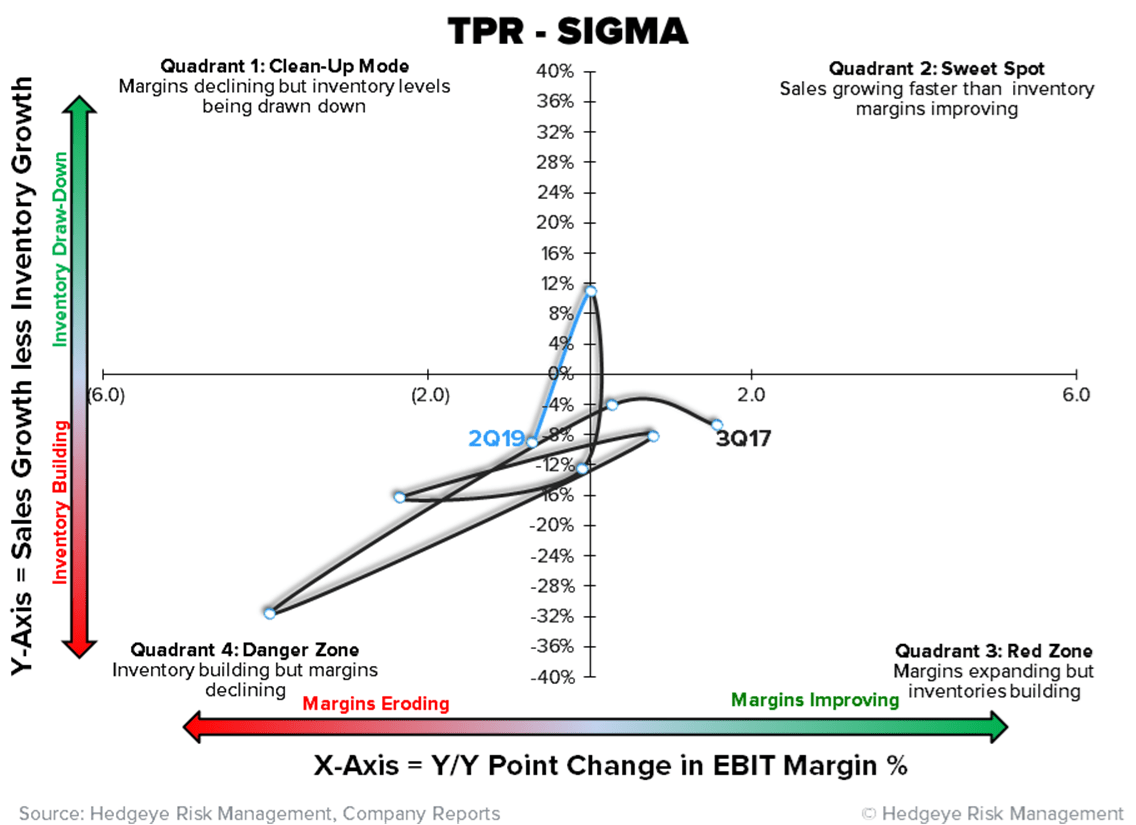

I took TPR down towards the bottom of my Best Idea list on 11/4 with the Stock at $42.85 due to concerns over China and Hedgeye Macro's 'Quad 4' call. But today at $32 – or just 7x a very defendable EBITDA number and sub 11x EPS – the market is looking through an inflection in growth and margin profile that should happen this quarter, at the same time when the rest of retail slows on the margin. The easy and emotional response is to downgrade/cut bait entirely on a weak guide and visceral reaction like this. The right response is to unemotionally assess what has changed (or hasn’t, for that matter), update our earnings model, and make the right call in marrying up the TREND and TAIL duration. In doing so, at $32 I think that we’re looking at 3 to 1 upside/downside over a TREND duration – with a roadmap to a double over a TAIL duration – particularly as TPR repositions/takes back/buys in the KATE license portfolio (like RL did in the 2000s). Without the license angle, I might sit back and be more patient. But this remains a hugely underappreciated part of this story, and one that is unique to TPR.

Usually when a company guides down like this, you have to wait a good year for the business to regain momentum and for the financial model to work. In the case of TPR, I think you have to wait less than a quarter. The stock isn’t trading off by 18% bc of the four cent miss…it’s trading down because of the $0.20 guide down just 13 weeks after it took up guidance for the year. The company is giving the impression that something changed fast – and that it doesn’t have the chops to manage a multi-brand portfolio. I don’t think either of those is the case. The quarter wasn’t squeaky clean by a long shot – with KATE comping down 11% as it cleared the channel of product in advance of the product refresh that hit two weeks ago (and moved the goods to outlets instead of promoting heavily – which carries its own issues), and with Coach being slightly (and I mean SLIGHTLY) more promotional. Kate is the primary variance in our model (i.e. it’s where I was flat-out wrong). But that changes in the quarter we’re currently sitting in.

What’s not apparent at face value is that TPR arguably didn’t have to guide like it did. This is a company that hasn’t missed a quarter since December 2013. The CFO’s last day on the job is tomorrow, and the interim CFO just happens to be the head of IR – yes, the same person that is key in setting guidance. She won’t be falling on her sword in May when TPR reports 3Q. Conversely, the company will likely be reporting a 1,500bps+ acceleration in comps at Kate Spade, a rebound in Stewart Weitzman as it laps the gaffes from last year, improved margins in core Coach as investments from the past year roll off, and we see accelerating accretion from TPR’s license acquisition strategy.

Ultimately we’re at $2.80 for the year – the top end of where consensus was before the company ’over-conservatively’ guided down, and I think that there’ll be a more defined path towards $4.00 in TAIL earnings power within 12 months. My biggest concern at $32 is if the Macro climate slows meaningfully from what our Macro team is currently calling for. The factor that could make my ‘path to a double’ statement wrong is if I am just flat-out wrong on all the work we’ve done around licensing optionality. But that was far more of a risk factor at $43 than $32.