R3: REQUIRED RETAIL READING

April 6, 2010

Sports Authority is accelerating square footage growth, in another step to dress the pig in lipstick for a 2H IPO. Good for most of the supply chain, incl NKE, UA, COLM, KSWS and even FL, DKS and HIBB. The problem is that we’d argue that TSA need not exist. Another ‘brilliant idea’ until it proves to be a disaster.

TODAY’S CALL OUT

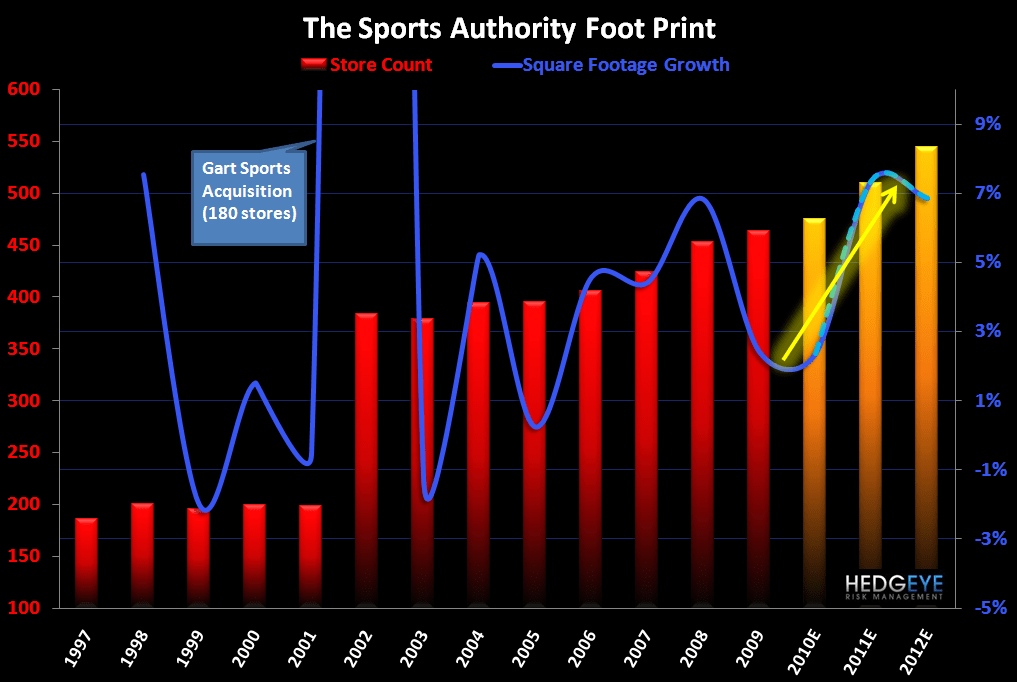

We think the most notable recent nugget out of retail is that The Sports Authority noted it is looking to step up expansion in 2011/2012 with the opening of approximately 35 units each year. The company also noted it is stepping up its store remodel efforts as well as its marketing and advertising messages. TRANSLATION = TSA is dressing itself up for an IPO. Accelerating unit growth, better product/comp cycle, leveraging fixed costs for the first in 3+ years. Sound familiar? Yes, Dollar General. Do we really NEED more Sports Authority’s? Only to the magnitude that we needed Linens ‘N Things and Circuit City. But the reality is that this will help Nike, Under Armour, Columbia, North Face (VFC) and most other brands that sell into this channel. It also helps the competition in that a better cycle eases up on the need for incumbents (DKS, FL, etc…) to get aggressive on price. Ultimately, this will sound like a really good idea until we all wake up one day and it will prove to be disaster.

Other Details…

- Store growth slowed to 9 store openings over 2008 and 2009. By 2011 expansion rate is expected to reach the 35 stores a year target which last occurred in 2007.

- Expansion will be focused in the Northeast and Midwest (Ohio Valley) with both mall and strip center locations.

- Texas market will get ‘special attention’ because TSA is locked in a tight battle with Dick's and Academy.

- Merchandise mix changing to accommodate more fitness at the expense of outdoor.

- TSA is teaming up more with New Balance to incorporate more activewear and the new NB toning shoes.

LEVINE’S LOW DOWN

- Add New Balance to the list of athletic footwear manufacturers to introduce a “toning” shoe. The latest entry called the “Rock & Tone” aims to mimic other “rocker” shoes, but with a lower profile sole and a lighter weight. Additionally, New Balance is planning to follow up with the launch of a “balance-board” shoe, called truebalance. This show will be actually be launched in July at upscale retailer, Fred Segal. Looks like New Balance is hoping to get a jumpstart on the LA scene with this one…

- Add social media and blogging to the list of tools Ann Taylor is employing in an attempt to revitalize its LOFT brand and get in touch with a younger, style conscious customer. The company recently launched “live. love. Loft.”, a blog that essentially reads like a fashion mag with product placement. Lots of LOFT product mixed with beauty, travel, food, home and health tips. With the publishing world in disarray maybe retailers will start hiring their own staff to publish content?

- New York-based Le Tigre, the popular American apparel brand of the 1980’s purchased by KCP in 2007, is creating a buzz with its timely billboard campaign on the West Side Highway sporting the tagline “Golf’s original Tiger. For those who play a round.” Don’t be surprised to see polos with the tiger signature among the crowds at Augusta this week as fans choosing not to support Team Tiger now have a more discrete way to protest his return.

HEDGEYE CALENDAR

MORNING NEWS

The Democratization of Fashion - As crowdsourcing continues to gain force, consumers are having their say about specific designs and being compensated for them monetarily, with prizes, discounts or other recognition. The trend is huge in Holland, San Francisco, New York and Chicago. Crowdsourcing is largely underused in the apparel industry. Threadless.com, FashionStake.com, and Made.com utilize this tactic. Threadless.com lets consumers decide which designs it produces in graphic T-shirts. And when FashionStake.com bows this fall, shoppers will be able to offer their two cents about collections and buy stakes in designer collections that will lead to discounts, freebies and fashion show invitations. Launched last week, Made.com, a London-based designer furniture site that only produces what consumers vote for and sells directly to them, is already looking into expanding the concept to clothing. By relying solely on crowdsourcing for its assortment, the site reduces the odds of having unsold inventory, eliminates the middleman altogether and offers voters discounts should they choose to actually buy the furniture. <wwd.com/business-news>

Home Depot's Blake Adds Jobs for First Time in Four Years on Sales Rebound - Home Depot Inc., the largest U.S. home-improvement retailer, is adding store jobs for the first time in four years in anticipation of a rebound in sales. <bloomberg.com/news>

Tory Plans Do Not Include a VAT Increase - The Conservative Party has insisted that it would not need to increase VAT in order to cut the deficit if it forms the next Government as Prime Minister Gorgon Brown is today expected to confirm that the next general election will be held on May 6. <drapersonline.com>

Spain Retail Tough in Downturn - Sales in Spain’s fashion industry slid 8% last year from 2008 to 18.3 bn euros in 2009. A 19% jobless rate has left 4.1 mm unemployed; GDP fell by 3.6% last year, the steepest drop in decades, and the deficit is a whopping 11.4% of GDP. Key to the sector’s revitalization is an immediate boost in consumer demand, greater globalization and a more viable made-in-Spain image, especially in foreign markets. The biannual apparel fair has taken a hit in recent editions, losing roughly 50% of its vendors. <wwd.com/retail-news>

Crocs Feel the Love Campaign - Crocs is on a mission to show consumers the "soul" and "foot-loving sole" of its shoes. The brand debuted a new campaign on March 29 centered on a single message of "Feel the Love," and it focuses on a proprietary technology called Croslite, which is built into every Crocs shoe. The campaign, created by the band's new lead agency Cramer-Krasselt/Chicago, is now rolling out in the U.S. and Europe. It spans TV and print (books such as Real Simple and InStyle), out-of-home, POP, and includes a major social media/digital component. <brandweek.com>

K-Swiss Enters a Sponsorship and Endorsement Deal - K-Swiss has entered into a sponsorship deal with Home Team Marketing to put its name in about 100 high schools in the Dallas, Houston, Los Angeles and Pittsburgh markets. K-Swiss indicated the list could grow to 1,000 in 2011 if successful. K-Swiss announced a global endorsement deal with "Biggest Loser" trainer and coach Jillian Michaels. She will represent K-Swiss and participate in interactive retail and consumer-facing programs throughout the year. In the future, Michaels will develop collaborative product line with K-Swiss. <sportsonesource.com>

Hugo Boss's Revamped E-Commerce - Hugo Boss opens its redone e-commerce site in the US today. It is part of a major worldwide initiative by the German luxury brand to update its Internet presence. The U.S. site will be on a new platform with entirely new design, navigation and functionality compared with the e-commerce sites running in Europe, which will eventually also relaunch on the new platform. The company’s efforts will turn to Asia next year. Chief executive officer Claus-Dietrich Lahrs predicted in November that Hugo Boss would sell more than 50 mm euros of goods online within two years, up from about 10 mm euros. <wwd.com/retail-news>

The Men’s Wearhouse Expands Prom Rep Program - Launched last year, the program offers teens 10% off their tuxedo rentals for every friend who rents at the Men’s Wearhouse. Ten referrals translates into a free tux. Female prom reps who earn a free tux rental can either transfer it to a friend or opt for a $100 Visa gift card. In 2009, participants had to visit a store to take advantage of the program, but this year, the company has instituted more social and online tools.<wwd.com/retail-news>

Wal-Mart Loses Fashion Driver from the Board - Allen Questrom is saying goodbye to Wal-Mart Stores Inc. After three years on the retailer’s board of directors, Questrom has decided to not seek reelection. Questrom saw little chance remaining to influence the company, though his expertise in apparel retailing and overhauling store presentations could come in handy considering Wal-Mart has a strong reputation for offering the lowest prices, but has limited fashion appeal. Two years ago, the giant discounter beefed up its New York apparel office in an attempt to stay on top of trends and elevate its apparel. Questrom was chairman and chief executive officer of JCP, Macy’s and Barneys New York. <wwd.com/retail-news>