Below are analyst updates on our eight current high-conviction long and short ideas. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

IDEAS UPDATES

RRC

Click here to read our analyst's original report.

Range Resources (RRC) retains some of the most economic and productive acreage in the U.S. E&P space and has decades of drilling runway.

Yet, within a sector that has earned a reputation for value destruction, Range has been one of the worst offenders. In the past 5 years, RRC checked the usual boxes of E&P value destructive behavior such as excessive debt and equity issuance to fund production and reserve growth. But what separates RRC from its peer group was the $4.4B equity financed acquisition of Memorial Resource Development (MRD) in 2016. The transaction gave MRD holders 31% of the proforma company and eviscerated ~$4.2B of RRC’s market value. The company is taking concrete steps in order to repair its reputation in the public equity markets by spending within cash flow, using FCF to pay down debt, and reconstituting its Board of Directors.

The EIA released its Short Term Energy Outlook on Tuesday, January 15th calling for an incremental increase in dry natural gas production of ~7 Bcf/d. That’s off a base of 83.3 Bcf/d in 2018. 2020 dry natural gas production is forecasted to be 92.2 Bcf/d in 2020. Dry natural gas production exited Dec-2018 at 88.6 Bcf/d, meaning that 2019 production is forecasted to grow ~1% from the current production base. The market has absorbed the 2018 production build as evidenced by the depleted inventory base. Taken in concert with added LNG export capacity, we continue to be relatively positive on the commodity.

The question is, where will the incremental supply come from. With WTI at ~$50/bbl, associated gas growth will likely underdeliver in 2019 from original expectations. And, with natural gas levered equities not being rewarded for growth, we expect more companies to prioritize capital discipline at the expense of growth. GPOR and AR have already been the first movers in that respect in the first few weeks of 2019. That would stand to benefit RRC, which we think has a best in class acreage position and efficiency metrics

DFRG

Click here to read our analyst's original report.

Del Frisco's (DFRG) reported positive comparable restaurant sales during Q4. The numbers showed weaker trends in November than October but accelerated in December and carried over into 2019 across all four brands. While management’s decision making process has been a bigger concern for the stock, the brands are healthy and the stock is trading at a significant discount to the value of the brands.

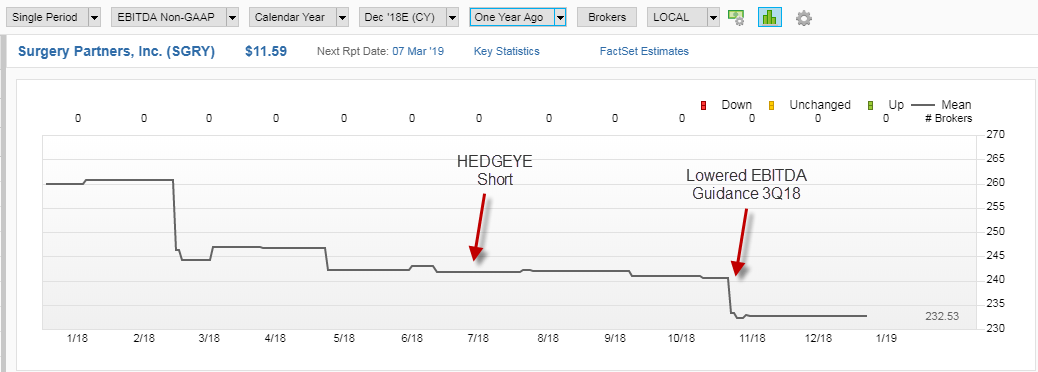

SGRY

Click here to read our analyst's original report.

At JPM recently, Surgery Partners (SGRY) reiterated the 2018 guidance they gave in early November when they reported Q3 earnings. We thought consensus EBITDA estimates were too high in July 2018, and looked for a guidance cut to be a catalyst on the short side. Timing and the thesis has played out well since then, but we still think 2019 EBITDA estimates are too high (see table below) and many elements of our short thesis are still in play such as:

- Low quality assets / poor case mix and

- Overleveraged balance sheet.

The company has shown a remarkable inability to generate free cash flow as they continue to take on more debt to fund their acquisition strategy. At the current rate, they will have to tap capital markets again later in 2019. From a valuation perspective, we can get to a $8 stock or 30% downside from here in 2019 if we are right on the fundamentals and catalysts. In our bear case scenario, we can see the stock going to $0. We expect the company to release 2019 guidance when they report Q4 earnings in February.

MCHP

Click here to read our analyst's original stock report.

You can’t own Microchip Technology (MCHP) for industrial HPA like performance with organic growth, singular focus on share gains in large markets, and innovation curves that continue to prove out.

The organic share gains are done, the second biggest revenue category is a creation of Analog Frankenstein that doesn’t grow much, and Microsemi Corp (MSCC), now at ~30% of revenue, will be dilutive to the growth rate of the entire entity. The long game of fixing vertical analog product inside a general purpose company is not a no-brainer fix and maybe hasn’t really been done successfully in the past. Investing, healing, and re-growing individual product lines wrapped up in the MSCC mess will take some time. In addition, capital intensity and taxes seem to remain as surprise factors.

MCHP just ended a long happy cycle streak of volume growth. The question for forward thinking semis analysts and PMs today; will this downturn be a shallow one like June 2015 and then back to the races, or is the long period of awesomeness since ~2012 coming to an end implying a steeper unit trough (or shallow recovery) and lower GM% across that forward horizon as utilizations come down?

AVLR

Click here to read our analyst's original report.

At its core, Avalara (AVLR) is still a growth company. But they may not be a tech company. Consider: The various parts of their engine were nearly all built via acquisition and the company (allegedly) re-architected much of their product after meeting a tiny competitor who is now suing them for appropriating his architecture despite having an NDA with the company.

The lack of addressable market is real in many ways: AVLR is selling an expensive version of something that is available at cheaper price points with better pricing transparency, and into a market that has a mixed opportunity set of open and closed doors.

SPLK

Click here to read our analyst's original report.

Splunk (SPLK) is still priced on go-go growth but multiple recent tailwinds begin to fade on a forward basis. Accelerations that drove the stock higher will not repeat next year including ~600-700bps benefit from the shift to ASC606, a big data center spending bump, plus the Machine Learning and Analytics splurge in the last year.

The company also faces secular headwinds on the margin with its tools always among the most expensive in its peer group, but also providing the most value. A recent pivot in the industry to separate expensive compute costs from cheap storage costs means there are some deflatable costs in the SPLK model, which bundles both at the higher price.

is still priced on go-go growth but multiple recent tailwinds begin to fade on a forward basis. Accelerations that drove the stock higher will not repeat next year including ~600-700bps benefit from the shift to ASC606, a big data center spending bump, plus the Machine Learning and Analytics splurge in the last year.

CGC

Click here to read our analyst's original report.

Recently, Canopy Growth (CGC) came out with a “hey, just a reminder, we have hemp,” press release (available HERE), just in case anyone forgot about their position in the market over the holiday break. One quote in the release stood out to us:

“Extracted product can be stored as inventory over the long term as regulatory paths to the Canadian market are defined. At this time, there is no path to the US market for CBD derived from Canadian-grown hemp.”

In other words, they have nothing to do with their current inventory! The release was a lot more of, what we can do, rather than what we have achieved. Either way, we believe the growth potential in this market is baked into their stock price given the bullishness around the potential products they can produce in partnership with STZ.

DPZ

Click here to read the short Domino's Pizza (DPZ) stock report Restaurants analyst Howard Penney sent Investing Ideas subscribers earlier this week.