“I like to listen. I’ve learned a great deal from listening carefully. Most people never listen.”

-Ernest Hemingway

We’re on Day 2 of a 3-day roady where my fellow Data Dependent, Darius Dale, and I are meeting with Institutional Investors in both NY and CT. This is one of the big competitive advantages I have with my job. Listening to the world’s best, that is.

If you listen, you learn. Not only do you get new pieces of information and unique perspectives, but you learn a lot about consensus narratives. After 3-days of meetings, I can tell you where the Pain Trades are going to be.

I can only tell you that because I take what I hear and marry that to where I have a chronic listening bias – the data. Embedded in both economic and market data is a tremendous amount of information about consensus too.

Back to the Global Macro Grind…

For now (based on calls, meetings, data, etc.) here are some consensus narratives we’re hearing:

- CHINA: “we’re going to get a trade deal with China by March, so we can’t be too bearish ahead of that.”

- USA: “since the Fed is dovish, that’s bullish for stocks now – bottom is probably in, but there’s not a lot of upside.”

- EUROPE: “oh yeah, we’re bearish after being bullish a year ago… but it’s probably priced in.”

I’d rank the discussions we have in that order too. Almost everyone starts with “China”… then we get to the “nice call on Quad 4 in Q4” part and how it’s “probably priced in”… and eventually we get to Europe.

Give this 3-6 months (after said “China deal”, which we don’t think will change #ChinaSlowing) and I think most meetings might start with how to risk manage recessions in parts of Europe… and who can go dovish faster, the Fed or the ECB.

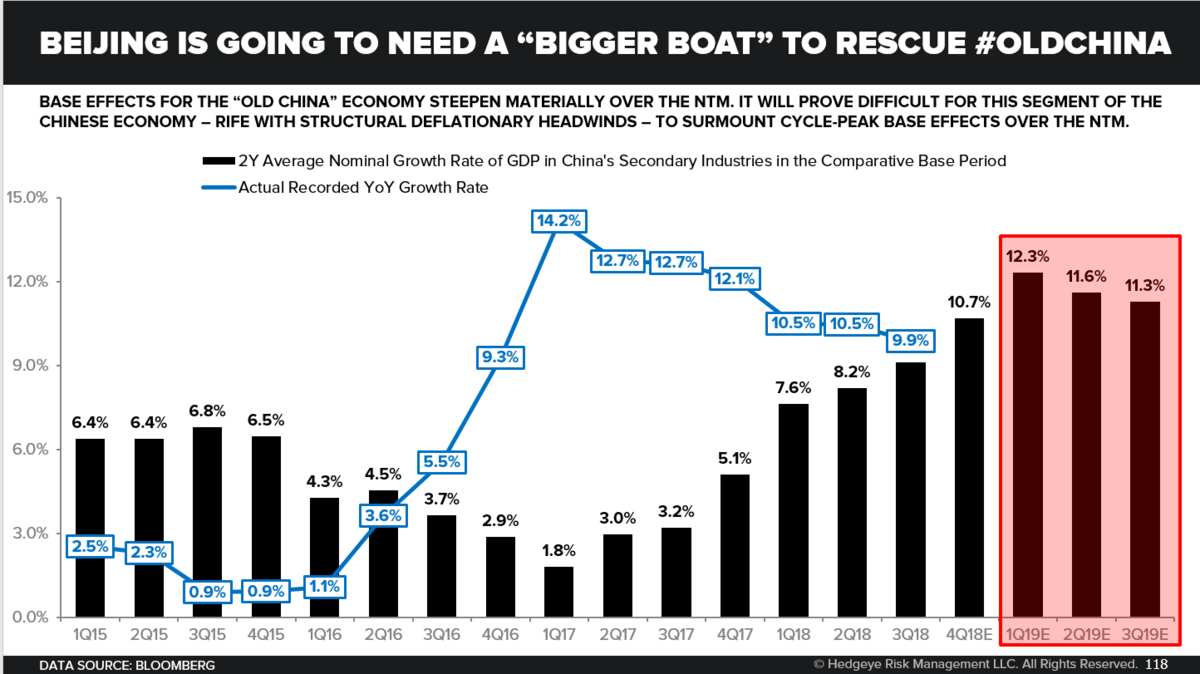

The Chinese have been going dovish at an accelerating rate since NOV-DEC… and they’re reiterating all of their cowbell again this morning. But what has all of this stimulus achieved? Nothing. China continues to slow into steepening base effects.

Btw, why do you think they’re stimulating at a faster rate?

A) Because growth has stabilized?

B) Because they think a trade deal is pending?

C) Because they’re slowing at a faster rate?

Alex, I’ll take C) for 2 & 20. As Darius pointed out in one of our data-detailed process notes this morning, this is not the “big bang they need to comp these comps. China’s monetary impulse is currently well shy of the initiatives we saw in 2H15-2016.”

If you don’t know what the Chinese Comps are, I have no idea how you’d know why March is going to be a bullish economic catalyst. It may very well be a catalyst for a week or a day-trade (from a low price). But it’s not a catalyst to change The Cycle.

Let’s listen to Alexa, I mean Darius, on The Global Economic Cycle update this morning:

- It’s Still Too Early To Buy EM: When we authored the call to be broadly short/underweight of EM equity, credit, and currency risk around this time 1yr ago, the call was met with a tremendous degree of pushback – which was to be expected at the cycle-peak of the mid-2016 to JAN ‘18 “Globally Synchronized Recovery”. Staying short of EM here is far less controversial, but that doesn’t mean it’s not the right tactical asset allocation decision. Specifically, neither our market signals nor the GIP data have inflected in a bullish manner, as most recently confirmed by the annual growth rates of Chinese Exports (↓ -850bps to 0.2% YoY in DEC), Chinese Imports (↓ -1080bps to -3.1% YoY in DEC), Indian Industrial Production (↓ -790bps to 0.5% YoY in NOV), and Turkish Industrial Production (↓ -937bps to -6.47% YoY in NOV). Further, our GIP Model has these not-inconsequential EM economies in Quads 3 and 4 here in 1Q19E, as comparative base effects for Real GDP growth continue to steepen for each economy (CH, IN, TR). We’ve been saying for upwards of three quarters now that EM won’t be broadly interesting on the long side until the Fed implements a full dovish policy pivot (read: not just pausing at the current level of rates and pace of balance sheet runoff) – a pivot that will allow Chinese policymakers to do a lot more on the monetary easing front than they have to date.

- Eurozone Recession Risk Rising: We discussed discombobulating dynamics within the Eurozone manufacturing economy in great detail in our Friday Early Look note, so I’ll be brief here: Eurozone Industrial Production growth slowed -450bps to -3.3% YoY in NOV, the slowest growth rate since the nadir of the region’s Sovereign Debt Crisis in NOV ’12. Further, the scenario analysis generated from our stacked sequential momentum model suggests YoY Eurozone Industrial Production growth is likely to bounce around between 0% and -3% over the NTM. As the title of the aforementioned note implies, you’re probably not short enough global cyclicals in light of that prospective catalyst.

Discombobulating-data-driven-dynamics, eh. Even a Canadian can listen to them in the context of consensus.

It’s not my job to miss the bottoming process China, EM, or Europe. If there was any data (economic or market signal) to support it, my job is to listen very closely to it and start getting long things we’ve been short for over a year now.

Might I miss the bottoms? Of course I will. But why on God’s good earth would I subscribe to anyone’s narrative that “the bottom is in” if they never properly timed the tops of these cycles being in to begin with?

Ironically enough on the US Equity Market, in the immediate-term my TRADE signal says the bottom is in, for now. It also says the top is in. But the bottom of the @Hedgeye Risk Range (2449 SPX) seems to be a bigger draw in discussions…

In terms of our non-consensus Long Treasuries (across the curve) call, the signal says lower-highs and lower-lows for the UST 10yr Yield. But that’s not a position consensus narratives nailed, so it’s not a big topic of discussion, yet.

As always, as volatility changes, my risk ranges change. So every day I have an opportunity to improve my positioning.

While a lower-low vs. the SPX DEC 24th low isn’t probable in the next 3-6 days. It is probable in the next 3-6 months. That would be Pain Trade 2.0 for anyone who is sure that the Chinese, EM, and US stock market “bottoms are in.”

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND views in brackets) are now:

UST 10yr Yield 2.56-2.80% (bearish)

UST 2yr Yield 2.40-2.61% (bearish)

SPX 2 (bearish)

RUT 1 (bearish)

NASDAQ 6 (bearish)

Shanghai Comp 2 (bearish)

DAX 105 (bearish)

VIX 17.17-30.19 (bullish)

USD 94.50-96.40 (neutral)

EUR/USD 1.13-1.15 (bearish)

Oil (WTI) 44.40-53.95 (bearish)

Gold 1 (bullish)

Copper 2.56-2.70 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}