Below are analyst updates on our seven current high-conviction long and short ideas. Please note that we removed W.W. Grainger (GWW) and Tallgrass Energy (TGE) from the short side of Investing Ideas this week. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

IDEAS UPDATES

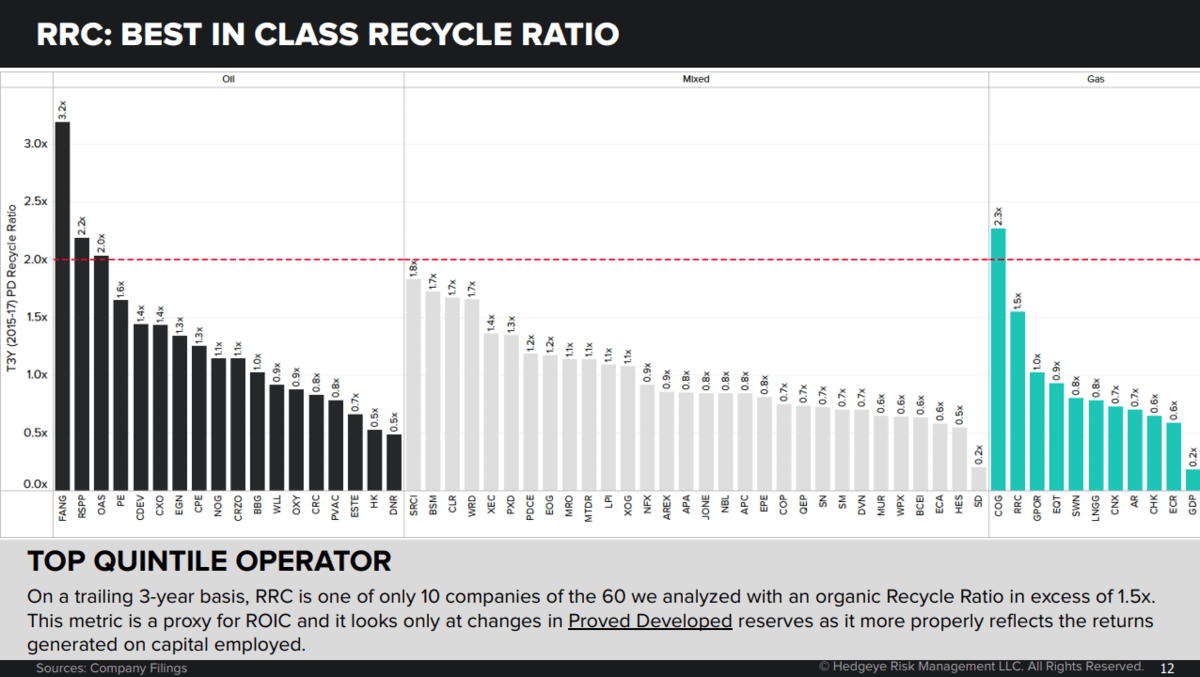

RRC

Click here to read our analyst's original report.

Range Resources (RRC) is amongst the most hated E&Ps in the energy sector due to the company’s previously poor capital allocation decisions. With a name as widely out of favor as RRC, management has the opportunity to create its own catalysts by delivering on expectations promised to the market. That means efficiently operating the company’s prolific Southwest Pennsylvania assets – something it has been quite adept at historically.

We continue to believe that Range offers one of the best risk/rewards in all of E&P, given the relative valuation for an asset base that has produced best in class recycle ratios and full-cycle margins for years. The balance sheet is in much better shape with leverage on 3Q18 EBITDA annualized at 3.0x; 2.8x pro forma the $300MM asset sale.

We estimate Fair Value for RRC to be $25 /share, significant upside from the current price of around ~$11.

(In case you missed it and for more detail on our long call on Range Resources, click here to watch Energy analyst Alec Richards' appearance on The Macro Show recently. Richards' updated commentary on RRC begins at 4:27.)

DFRG

Click here to read our analyst's original report.

Last week Del Frisco's (DFRG) reported positive comparable restaurant sales during Q4. The numbers showed weaker trends in November than October but accelerated in December and carried over into 2019 across all four brands. While management’s decision making process has been a bigger concern for the stock, the brands are healthy and the stock is trading at a significant discount to the value of the brands.

SGRY

Click here to read our analyst's original report.

"As I outlined recently on our Q1 Macro Themes call, one of the Sector Exposures I want to be getting net SHORT of right now is Healthcare," explains Hedgeye CEO Keith McCullough. "I especially want to be short low-quality Healthcare companies that are levered. Surgery Partners (SGRY) has been a fantastic short for Tom Tobin's Healthcare team."

We think margin expansion is going to be very difficult for SGRY.

But the core of any balance sheet short is that this company is not earning it’s cost of capital. It continues to burn cash which means that they’re going to have to raise capital at a time where they’re already significantly levered. This company is about 9X levered.

One of the points we made is that they just don’t have enough liquidity given that cash flow is already negative. Leverage is so high it’s going to be difficult for the company to fuel the roll-up strategy and hit consensus numbers. Sources of cash are being drawn down so it’s going to be difficult for the company to do enough acquisitions to close on the pipeline and hit numbers. They need to spend about $150-$200 million in acquisitions to hit 2019 estimates. At the end of 1Q19, at the current pace, they would only have $122 million so there’s a gap that’s emerging.

The company pre-announced saying that they’re going to raise additional capital to fund acquisitions going forward. This is really not what you want to see as an equity holder when they probably should be deleveraging, since there is so much risk to this model.

MCHP

Click here to read our analyst's original stock report.

"After very few analysts on the Old Wall warned you that the Semi-Cycle peaked 6-9 months ago, there’s plenty of fun and speculation going on in semis (SMH) today that The Cycle is back (per the same analysts), baby!," writes Hedgeye CEO Keith McCullough earlier this week. "Or not... and it’s just one of the many bear market bounces we’ve seen for months now. Ami Joseph's favorite Semiconductor Short remains Microchip Technology (MCHP), so I see no reason not to send you a SELL signal here, signaling immediate-term TRADE #overbought within a Bearish @Hedgeye TREND research view."

Looking at the longer-term bearish research call, on the most recent earnings call, no one asked about the lawsuit or the risk that Steve might have to recuse himself from the CEO role. The company is fixing MSCC operationally but the ongoing evidence of excess inventory (over 8 months for high-reliability products) only buttresses our view that real growth for MSCC was even worse organically than the feeble numbers we had scrubbed to.

In other words, the point of buying MSCC…is to hurry up and buy another semi company. Steve even noted that his strategy is to buy underperforming semiconductor assets, which is a fine strategy, but does not come with a premium or high performance analog multiple.

AVLR

Click here to read our analyst's original report.

"With Tech and Industrials now signaling #1 and #2 on the short side from a Sector Style perspective, I'm happy to see one of Ami Joseph's favorite Tech Shorts (Avalara (AVLR) bounce to lower-highs on decelerating volume again," wrote Hedgeye CEO Keith McCullough earlier this week. "Who knows how many more selling opportunities we're going to see like the ones we're seeing so far this week."

Here are some key takeaways on our long-term bear thesis regarding AVLR:

- The various parts of their engine were nearly all built via acquisition.

- The company (allegedly) re-architected everything after meeting a tiny competitor who is now suing them for appropriating his architecture despite having an NDA with the company.

- Then you stack additional items, such as:

- Disaffected sales force

- A ‘sales-oriented’ company

- A litany of problems inside the corporate culture

- Revolving door at the leadership role on the tech side

- A large platform reseller sitting on its best market opportunity

- A large software vendor totally deflating the value proposition at the mid-low end of the market

- States not necessarily able to enforce compliance (today) and who tolerate best effort

With adoption curve much slower than go-go SaaS companies, and valuation in-line or better on EV/S, a mixed opportunity set, deflationary competitive elements, a company with a lot of baggage, and a host of pent-up potential sellers on the lockup in December, we think this stock still hasn’t found the right valuation center… but we still think it's lower.

SPLK

Click here to read our analyst's original report.

"Obviously shorting Splunk (SPLK) was the biggest timing mistake I've made in months (shorting anything Tech in the last week of December turned out to be a bad decision)," wrote Hedgeye CEO Keith McCullough earlier this week. "A bigger mistake would have been adding to the short idea before the SP500 ramped back to the top-end of its @Hedgeye Risk Range... And I think another mistake would be not shorting more now that SPLK is signaling immediate-term #overbought alongside the High Beta US Equity signal. Covering shorts and capitulating to the bull side is what consensus has been doing at the beginning of every month, for the past 4 months."

Looking longer-term we're sticking with the Splunk short call because while the story for Splunk is by no means over. Splunk is at a point similar to other large software companies when they hit similar revenue run rates who pivoted towards M&A. In this case, that’ll be the primary use for newly growing FCF. We think the pivot from go-go growth EV/S ratios to slower rates of growth, acquisitions, and EV/FCF ratios usually doesn’t sort out so smoothly.

We are not telling Longs to hit the competition-panic button, but the combination of slower growth and shift to FCF based valuation will at least present a sideways equation, and in our view sets up for a 20-25% downside risk profile as we enter 2019.

CGC

Click here to read this short Canopy Growth (CGC) stock report Cannabis analysts Howard Penney and Shayne Laidlaw sent Investing Ideas subscribers earlier this week.