R3: REQUIRED RETAIL READING

March 31, 2010

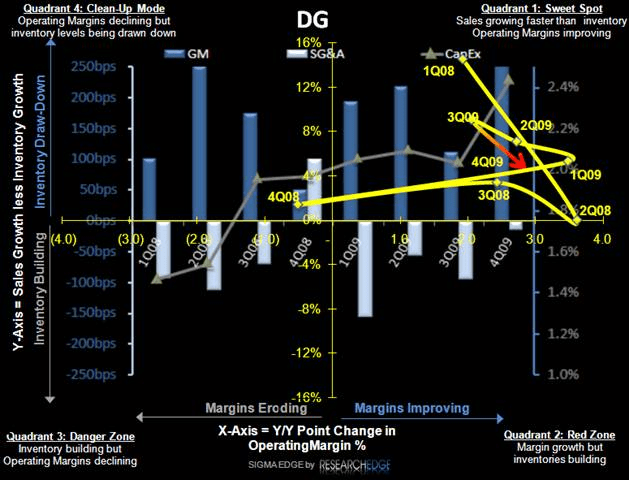

TODAY’S CALL OUT - DG: The Last of the Good?

Based on what we see thus far, this solid print appears to be the post-offering peak for DG as it relates to rate of acceleration in business growth. Comp guidance is suggesting deceleration, GM yy compares get very difficult effective immediately, and SG&A/capex begins to accelerate along with stepped up square footage. If you want to buy this name, KKR will likely give you another shot at buying theirs. Be wary.

This morning Dollar General reported 4Q results, and by most measures this was as solid a quarter as one could envision. The biggest surprise was the nearly 200 bps of gross margin expansion, not the robust same store sales growth of 7.4% which was in-line with expectations. Clearly the company’s strategy of working with less vendors and focusing on category management is helping to produce volume discounts- which in turn is helping to reduce COGS. As one of the few true growth stories (units and comps), it’s not surprising to see vendors step it up at a time when other more traditional formats are standing still. We just wonder how sustainable this process can be over the course of 2010, especially when growth will begin to slow from peak levels.

Recall that we’ve been cautious on Dollar General and the overall space that generally caters to low income consumers. Our view has not been that the sector is going to fall off of a cliff, but rather the marginal growth in the low income demographic is slowing while at the same time capacity (i.e new store openings) is accelerating. This supply/demand disconnect is a scenario that will unfold over time, and one that is clearly not impacting current results. We know this. But what we also know is that 2010 represents a year where both top and bottom line compares for DG will be at their toughest in the company’s history. Same-store sales momentum will slow and reliance on margin enhancing strategies such as “better buying”, increased private label penetration, and improvement in more discretionary categories such as home and apparel is far more speculative and risky than it has been over the past year. We continue to believe momentum will slow on the margin, much like it has already done with the pace of Americans entering the “sweet spot” of the DG demographic. For the near-term, it’s likely we’ll see another stock offering before there is a meaningful correction in the company’s momentum. We have no knowledge of the exact timing of a secondary, but we’re pretty sure there is a road show coming to town very soon.

Eric Levine

Director

LEVINE’S LOW DOWN

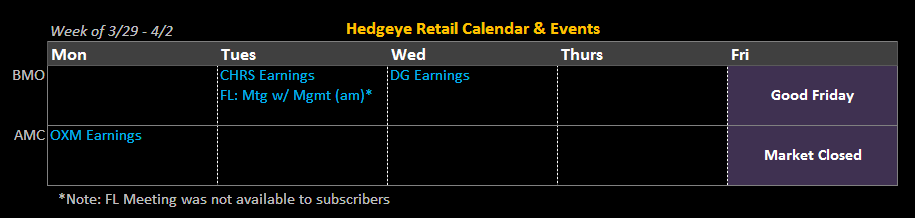

- In an effort to drive traffic to its newly rebuilt website, CHRS has implemented amongst other features a universal checkout across business concepts (i.e. Lane Bryant, Catherine’s, & Fashion Bug) as well as free shipping to store locations. Surprisingly, 25% of customers are opting to ship to the store resulting in increased traffic at the store level as well.

- While OXM’s year-end results reveal an improved balance sheet compared to last year, last I checked a 58% Net Debt/Total Capital ratio does not qualify for ‘fortress’ status. Nonetheless, management was disturbingly enthusiastic about increased M&A activity and the possibility of growing the business via acquisition. Other uses of cash noted included accelerating Tommy Bahama store growth. With a lone star brand in an otherwise challenged portfolio, OXM might just find itself on the other side of the table in an acquisitive environment.

- Add Swoozies to the list of retailers facing liquidation. After filing Chapter 11, the 43 store stationary/gift retailer was unable to execute a credible reorganization effort. As a result, the entire chain is now entering liquidation. At one point early in its growth, Swoozies was dubbed the “hip Hallmark” and was thought to have one of the more innovative retailers in the card/gift space.

HEDGEYE CALENDAR

MORNING NEWS

Annual SGMA Report on Fitness and Sport Participation - The fastest growing activity in the country is Pilates. With 8.6 mm Americans participating in ’09, it’s up 456% since 2000. The activity most Americans participate in is walking (110 mm) followed by bowling (57.3 mm). Thanks to the UFC, viewing of mixed martial arts might be on the rise, but only 6.5 mm Americans participated in the cross disciplined sport in 2009, down 3.8% from last year. There are now 44 mm runners in the US, up 6.7% vs. 2008. <cnbc.com>

Sizing Up the Chinese Market - Industry leaders and local government officials discussed their outlook for the Chinese luxury goods market at a conference over the weekend, touching on a range of topics such as the untapped potential of third and fourth tier cities and whether Chinese consumers are ready to accept Chinese made luxury products. In a recent report, Bernstein Research estimated that the Mainland Chinese market for luxury goods was worth 6.6 bn euros, or about $8.9 bn. The report went on to state that Greater China, comprising the Mainland, Hong Kong, Taiwan and Macau, accounts for 10% of the world’s demand for luxury goods. Japan accounts for 12% while Europe and the Americas count for 39% and 29% respectively. <wwd.com/business-news>

Hong Kong Government Boost for Textile and Clothing - Hong Kong apparel and textile companies will be benefited from the government's latest launch of research and development cash rebate scheme that will be launched at the start of April. The R&D Cash Rebate Scheme aims to reinforce a research culture among enterprises and encourage them to establish stronger partnership with public research institutions. Under the Scheme, enterprises conducting applied R&D projects will enjoy a cash rebate equivalent to 10% of their invested amounts. The preliminary forecast is that HK$20 mm will be disbursed in 2010-11. <fashionnetasia.com>

Hon Kong February Sales Surge - Hong Kong retail sales surged by 35.8% in terms of value in February due to improved labor market conditions that boosted consumer confidence. The growth was faster than the 6.5% growth in the previous month. However, growth in retail sales was smaller than the consensus forecast of 39%. The statistical office said retail sales tend to show greater volatility in the first two months of a year due to the timing of the Lunar New Year. "As the Lunar New Year fell on February 14 this year but on January 26 last year, it is more appropriate to analyze the retail sales figures for January and February taken together in making year-on-year comparison." In the first two months of the year, retail sales value increased 18.8% compared to the same period of the previous year and retail sales volume grew 15.1%. <fashionnetasia.com>

EU General Court Rules Against Claims from 5 Chinese Footwear Exporters - Chinese footwear exporting producers, notably Brosmann Footwear, Seasonable Footwear, Lung Pao Footwear and Risen Footwear, argued against the EU Commission’s decision to consider Market Economy Treatment (MET) claims of only sampled producers and not of all producers who applied for MET. <fashionnetasia.com>

Tommy Hilfiger to Assume Direct Control of China - The brand reached an agreement with its licensee Dickson Concepts (International) Ltd. to assume direct control of its Chinese wholesale and retail business as of March 1 next year. Dickson will continue on as licensee for the brand in Hong Kong, Macau, Taiwan, Singapore and Malaysia until 2019. “This acquisition is in line with our strategy to consolidate brand management and approach the market in the most coordinated manner possible,” said Fred Gehring, chief executive officer of Hilfiger, which is set to be acquired by Phillips-Van Heusen Corp. in a $3 billion deal unveiled this month. <wwd.com/business-news>

The Misses Category in Fashion - Over the last two years, everything from overhauling the executive and design ranks to cost-cutting, modernizing collections to installing “brand filters” has occurred at Ann Taylor, Talbots, Dress Barn, Chico’s, J.C. Penney, Macy’s, Liz Claiborne and Jones Apparel, stirring a sense this could at last be the year the sector crawls out of its hole and reverses declines. Retailers say they’ve been waking up to what women want and imbuing what were mundane “missy” lines with higher-grade fabrics, detailing, embellishments, color, closer fits and stretch, not to mention taking inspiration from contemporary and designer styles for a younger, sexier appeal but with age-appropriate sizing and moderate to better pricing. The NPD Group estimates that, for the last fiscal year, misses’ apparel generated $45.84 bn in sales in the U.S., compared with $48.35 bn the year before. NPD said the total women’s apparel market came to $108.7 bn last year. A dressy cycle, layering pieces, jacket alternatives and a shift in knits to crafted looks, fabric manipulation and embellishments are fueling misses’ sales. So is activewear, either functional or spectator-oriented, including terry and velour separates, track suits, hoodies and brands such as Nike, Adidas and Puma. <wwd.com/retail-news>

First Kohl’s and Avril Lavigne, then Wal-Mart and Miley Cyrus, and recently J.C. Penney with Mary-Kate and Ashley Olsen. Gomez, the 17-year-old star of Disney Channel’s “Wizards of Waverly Place,” is taking the fashion line she’s launching for back-to-school exclusively to Kmart’s 1,327 stores across the U.S. and in Puerto Rico. With retail prices capped at $24, Dream Out Loud by Selena Gomez will play a central role in Kmart’s strategy to double the size of its juniors section, where the company will weed out lesser-known labels, introduce new brands and create a shopper-friendly space. Gomez’s team is dreaming big: Retail sales are projected to hit $100 million in the first year. <wwd.com/footwear-news>

`Luxury Is Not Dead' as Americans Seek $490,000 Watches, $16,000 Weekends - Samantha von Sperling realized luxury shoppers had regained some of their confidence last month when her clients began booking $16,000 weekend excursions to Manhattan that included Jean Georges dinners and shopping sprees at Barneys and Giorgio Armani. <bloomberg.com/news>

Consumers Look More Kindly on Online Ads - A new survey suggests that online advertising has not worn out its welcome. In the new poll, conducted this month, 51% of respondents said they're "very likely" or "somewhat likely" to read and act upon e-mail offers, up from 47% last year. There were similar upticks in the numbers saying they're at least somewhat likely to read and respond to sponsored search-engine links (from 39% last year to 40% this year), banner ads (from 25% to 28%) and pop-up ads (from 13% to 19%). 53% this year (vs. 51 percent last year) said they're at least somewhat likely to read and respond to "articles that include brand information." <brandweek.com/bw/>

An online retailer settles with American Apparel - Online retailer NYCBlanks.com has reached a settlement with American Apparel Inc., which sued the e-retailer for allegedly violating the consumer brand manufacturer’s policy against selling unembellished American Apparel garments. <internetretailer.com>

LuLuLemon.com hit its stride with online shoppers in 2009 - Having only launched e-commerce in April, the web ended up accounting for 4% of total sales for LuLuLemon Athletica last year. <internetretailer.com>

Australian Retail Sales, Building Approvals Tumble as Rate Increases Bite - Australian retail sales and building approvals unexpectedly tumbled in February, adding to signs the central bank’s interest-rate increases are cooling domestic demand. <bloomberg.com/news>

Borders Said to Be Close to Arranging Financing to Repay Loan Due April 1 - Borders Group Inc., the unprofitable U.S. book retailer, is close to arranging financing that would allow it to repay a loan due this week, two people with knowledge of the matter said. <bloomberg.com/news>

Collective Licensing International and Bioworld Merchandising - Collective Licensing International (CLI) announced today that it has entered a three-year agreement with Bioworld Merchandising to license apparel and accessory lines under the Vision Street Wear brand. Under the design and manufacturing licensing agreement, Bioworld will help accelerate the momentum that Vision Street Wear has experienced since its re-launch in Summer 2009. <marketwatch.com>