Over $17 trillion has been erased from global equity markets since 2018’s highs. Yes, that’s officially bear market territory (down more than -20%).

For the record, the Hedgeye Macro team proactively prepared our subscribers for this last January.

Guess what?

Our 2019 global outlook remains decidedly bearish.

We want you to be prepared for the year ahead. Watch the replay of this special free edition of The Macro Show below hosted by CEO Keith McCullough, plus an excerpt transcribed from the show. Keith discusses our current market outlook and prepares you (and your portfolio) for the year ahead.

|

Keith McCullough: First on Japan, down hard overnight. This was the first day of the year for the Japanese stock market. If you want an update on that it is careening toward a crash. Now a crash, as defined by most people that have run money in their life, is a greater than 20% drop in a straight line. Japan, as you can see, peaked in October and was down -2.3% and remains bearish trend at Hedgeye. So we remain bearish on Japanese stocks and with a big breakout makes the Japanese Yen bullish trend, which is also new at Hedgeye. And finally what I’d say about Japan is what’s a very good indicator of both global growth and inflation expectations is the yield on JGBs or Japanese government bonds. JGBs now have a yield of -0.05%, down 11 basis points in the last month alone. The Japanese see what we’ve been seeing for a long time at Hedgeye, for over a year, and it’s that the global economic cycle peaked in January of last year and now we go on and on with that being priced-in by markets. |

|

McCullough: Point number two this morning is counter-trend bounces. We see countertrend bounces in China, Copper, Europe, in the U.S. equity market, in Tech, which got absolutely body bagged yesterday. Don’t forget that the Nasdaq yesterday got to down -20.3%. That’s a crash. You don’t want that. You want to have your shorts on. So on the downside of yesterday’s move the Nasdaq is down -20.3% from where it was at the end of August, when the U.S. economic cycle peak and the corporate profit cycle peaked. Now, we’re going to constantly see these counter-trend bounces because everyone who missed it is trying to tell you that it’s over with. They’re confusing dips with disasters. Dips are not disasters. For two and a half years going into September, I was bullish on growth stocks, Tech and FAANG fully-loaded. That changed in September for us. That was a really important pivot. When you go from being long growth to short growth, then you’re long Treasuries. And there you have a smart buying opportunity this morning on the Jobs Report. |

|

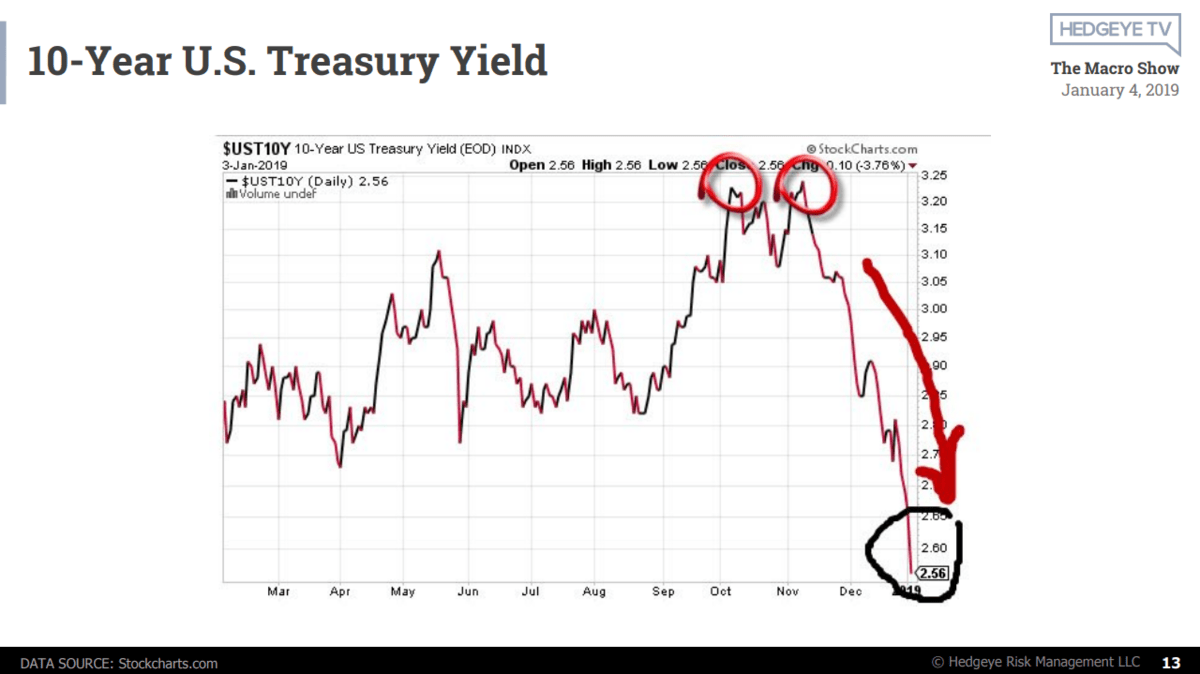

McCullough: Point number three this morning is the 10-year yield. There are late cycle indicators in Macro and there are early cycle indicators in Macro. The latest of late cycle indicators, the latest of late, is wages. Look at these wage inflation charts, 3.5% on average hourly earnings. Do you think that this chart has gone up quite a bit. Those charts look pretty bullish to me, hitting a 9-year high. That’s called a big pain in the you-know-what for corporations that have to pay people wages. So again this is quintessentially what happens at the end of the economic cycle. In every economic cycle, wages always increase into a recession and therefore perpetuate a recession. So wages go up, companies’ revenue start to slow and margins get compressed. And then guess what, you have to fire people. That’s how the labor market works. If you didn’t know that now you know. This is going to put a new nail in the coffin for people who have been saying ‘The Fed has to cut interest rates tomorrow.’ They’re not going to do it with that kind of a labor report. What I want you to focus on doing today is buying Treasuries and or securities that are linked to falling bond yields. What we think and continue to think, and we’re one of the first firms to make the turn on growth to slower growth is that bond yields would fall from those peaks in September and October. You didn’t want to be shorting Treasuries up there, which is what a lot of Macro hedge funds did. You can beat most Macro hedge funds by using Hedgeye. So we’re going to get the bounce. How much lower we’re going to go from here is a function of the Risk Ranges, which the low end of the range is currently at 2.54%. So we’ll consider it probable that over the intermediate term, which is different than the immediate term at 2.54%, could easily go down to 2.50% and then lower. So we’re going to stay with that and all the functions of that: Buying Utilities at the low-end of the range and REITs, Gold and Housing stocks at the low-end of the risk range. |