R3: REQUIRED RETAIL READING

March 30, 2010

TODAY’S CALL OUT: OXM/CHRS, and the Market’s Broad Brush

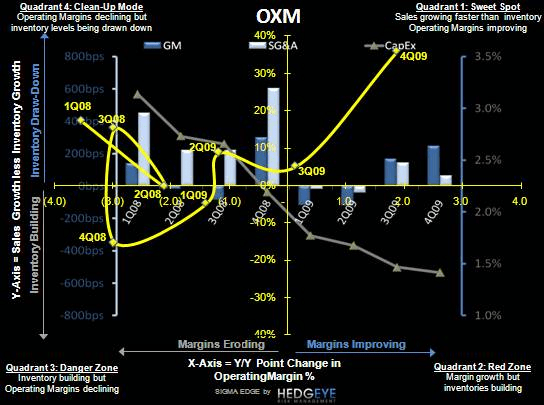

OXM and CHRS each reported polar opposite quarters – but weakish guidance is all it takes to take away the bid on these names. OXM is showing an improving sales trajectory, and a far better balance sheet relative to sales. CHRS can’t get out of its own way, with higher margins, but one of the biggest sequential negative changes in inventory/sales in retail this quarter. Higher margins with inventories building? Good luck. Despite the very different SIGMA positions below (let me know if you need interpretation), the stock movements are not too dissimilar this morning. We’re at the point where all it takes is a hint that beating estimates/guidance is no longer a reality – and buyers evaporate.

LEVINE’S LOW DOWN

- As Apple iPad launch day approaches (April 3rd), the big question is where can consumers go to find the latest super hyped gadget. Interestingly, while all Apple stores will have the product on day one, not all Best Buy’s will carry it. Best Buy will only stock the iPad at locations that are staffed with Apple Solutions Consultants. Apple.com will also be the only online retailer to carry the device at launch.

- According to research firm compete, the average American holds 4.4 credit cards but regularly only uses about 1.9 of those cards. Interestingly, 36% of cardholders base usage on specific deals offered such as reward points or specific merchant savings. Another 18% of cardholders actually have no particular reason for choosing one card vs. another. We note this is all in light of another recent study that revealed 54% of consumers actually prefer to use cold hard cash for purchases.

- ‘Exploding’ gift cards are quickly becoming a thing of the past. With most national retailers forced to eliminate expiration dates and dormancy fees on gift cards to comply with restrictions adopted by 40 states, the Fed has ruled that retailers have until August 22, 2010 to remove all such cards from the shelves. The new rules will require that dormancy fees start no less than 1-year after the issue date and expirations no sooner than 5-years. More importantly, related details will be detailed on cards after this summer. The real change is likely to temper the typical post holiday rush a time when consumers have felt compelled to cash their cards in before realizing they’ve expired worthless.

HEDGEYE CALENDAR

MORNING NEWS

SGMA Sport Participation Report - According to the Sporting Goods Manufacturers Association's Sports, Fitness, and Recreation Participation Overview (2010 edition), baseball, football and basketball all continued to show notable declines in participants in 2009. Outdoor soccer and outdoor softball saw smaller declines. But notable gains were seen in lacrosse, rugby and ice hockey. <sportsonesource.com>

UA Dips into Tennis - Under Armour has signed into an agreement with the Junior Tennis Champion Center at College Park, Maryland. The company will supply gear to the centers' coaches and instructors who will wear and test new products. <sportsonesource.com>

High End European Outlet Mall Operator Sees Increases - Value Retail plc, which operates nine high-end outlet malls in Europe with a total of 850 stores, reported a 21% increase in sales in 2009, reaching the 1 billion euro-mark, or $1.39 billion at average exchange rates. The number of visitors rose 11% last year. In particular, the number of shoppers hailing from China grew 80%. Visitors from the Middle East jumped 122% and those from South East Asia climbed 67%. <wwd.com/business-news>

Positive Outlook on Italy's Textile and Apparel Industry - Italy’s textile and apparel industry has overcome “the most dramatic phase of the current recession,” according to Sistema Moda Italia, one of the country’s main fashion associations. In 2009, the textile and clothing industry registered revenues of $62.8 bn at average exchange rates, down 16.5% compared with the previous year. Exports fell 20.3%, while the value of production slipped 13.8%. <wwd.com/business-news>

WalMart Welcomes Latino Apparel Brands - Chucho and Palomita, new young men's and juniors' Latino clothing brands, have rolled out at select Walmart stores across Arizona, California and Texas. Both brands are manufactured by DLI and are distributed by West Coast Novelty. WCN also has relationships with NFL, NBA and MLB.

In other Walmart news, the retailer plans to begin selling 3-D televisions leading up to the holiday shopping season. Other retailers such as Best Buy, Sears and Amazon.com have already begun carrying 3-D TVs. <licensemag.com>

Japanese Retail Sales Rise on Government Subsidies for Green Cars - Japanese retail sales rose 4.2% higher in February from a year earlier, according to government data released Monday. The result far exceeded the 1.8% average forecast from a Reuters survey, and was the largest gain since a 12.4% spike in March 1997, according to Dow Jones Newswires. Part of the rise was attributed to government subsidies for fuel-efficient cars. <marketwatch.com>

JOEZ Signs Footwear License Agreement - Joe's Jeans Inc. announced today that it has signed a new license agreement with Burano LLC to manufacture and distribute Joe's® branded footwear for women. The initial term of the agreement is for three years with minimum net sales commitments of $5.5 mm over the term. The first shipment consists of ballet flats in a variety of embellishments and textures and began shipping this month to major department and specialty store retailers, Company owned retail stores and its Internet store with a retail price of $120 to $145. In April, a line of wedges, flat sandals and casual heels is expected to begin shipping and the Fall line, including boots, is expected to begin shipping in July. <money.cnn.com/news>

Haiti Hopes To Increase Textile Production Volume - The Haitian apparel industry has asked the Obama administration and Congress to increase the volume of textiles and apparel that can be shipped here duty free in an effort to help its domestic industry get back on its feet following the devastating earthquake in January. The higher duty free levels are necessary to encourage significant investments in Haiti’s garment sector, which suffered significant hardships from earthquake damage, said Georges Sassine, president of the Association of Industries of Haiti and executive director of the CTMO-HOPE, a government-sponsored commission. <wwd.com/business-news>

Hugo Boss Cuts Dividend - The supervisory and executive boards of Hugo Boss AG have proposed a 30% cut in the firm’s dividend for 2009. Shareholders are to receive 0.96 and 0.97 euros, or $1.29 and $1.30 at current exchange rates, per common and preferred shares, respectively, down from 1.37 and 1.38 euros, or $1.84 and $1.85. The company said Monday that the lowered dividend would ensure “sufficient financial resources for future growth.” <wwd.com/business-news>