Since OPEC+ announced its 1.2 million barrel per day (b/d) production cut on December 7, the market has responded with a lack of confidence that the move will balance projected oversupply in 2018.

Indeed, two weeks after the OPEC meeting, oil prices are ironically lower today.

Certainly oil markets are under pressure due to macroeconomic factors that have nothing to do with oil fundamentals (see the Hedgeye Macro team’s excellent Quad 4 during Q4 analysis).

However, there continues to be concerns that the cuts may not be enough to counter a supply surge in 1H 2019 or that cut compliance will not be sufficient. We think these oversupply of oversupply concerns are misplaced. We said on December 7 that the cuts were credible, and the total cuts are actually closer to 1.7 million b/d when you add involuntary cuts from Iran and Venezuela.

We expect to see in the coming weeks hard evidence of the expected cuts and other data that will provide confidence that tighter oil markets are around the corner.

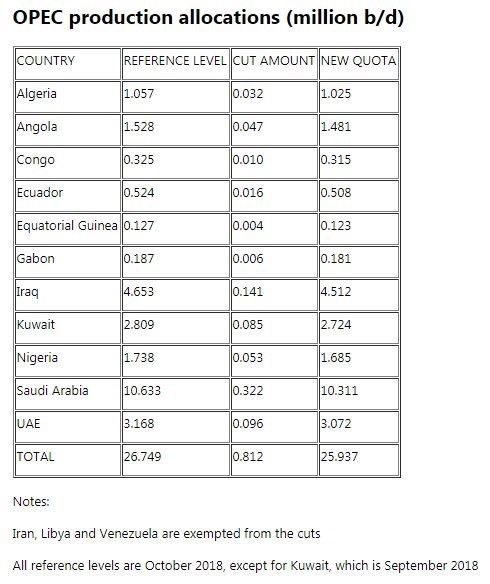

OPEC took a big step forward Thursday when it released a table of cuts from participating producers in the OPEC+ group. When the OPEC decision was announced on December 7, only the top line numbers of the 1.2 million b/d cut were released. We were expecting a table of country quotas to quickly follow in the following days but it did not happen. At the time, some analysts and reporters decried OPEC’s “fuzzy math” in the cut agreement. We think the lack of transparency about the individual country cuts has contributed to the market’s lack of confidence in the OPEC+ cuts. We see OPEC providing the table of individual country cuts as positive for market transparency and confidence, and we provide the tables below (courtesy of Platts).

Saudi Arabia is leading the group with an official cut quota of 322,000 b/d from the October baseline. However, Saudi production in November was 11.1 million b/d and this translates into a total cut of nearly 800,000 b/d from the Kingdom. Moreover, Saudi Energy Minister Khalid al-Falih said in December that he expected Saudi production to be 10.2 million b/d in January so Saudi Arabia will be cutting 900,000 b/d in production from November and will be significantly below its quota of 10.311.

Saudi Arabia’s announcement Tuesday of its largest budget in history should serve as the clearest sign of the Kingdom’s determination to push prices higher. Minister al-Falih underscored this in comments to the press on Wednesday:

“On fundamentals, I can tell you with a high degree of confidence, we will achieve balance between supply and demand in 2019. Make no mistake about it. We are united within the Kingdom and with our partners within OPEC. It is a strong agreement that will bring down the inventory build that has happened in the last several weeks.”

Based on these comments and past production levels, we think the market should be prepared for a surprise in January and a larger Saudi cut closer to 10.0 million b/d that would be similar to January 2018. Saudi energy officials have telegraphed the 10.2 million b/d production figure already. But we translate al-Falih’s recent comments and the budget announcement this week as raising the probability of a surprise even lower production number to jolt the market to heed the Saudi commitment to cuts.

In addition, Saudi Arabia has already cut exports to the US, and we believe you will start to see larger inventory draws in EIA data as a result. The weekly reminder of the inventory draws in January will be additional hard evidence to the market that the OPEC cuts are real.

There has been a great deal of attention to Russia’s participation in the production cuts. On one hand, we read headlines that Russia is now in control of OPEC while other press articles highlight Russia’s expected lack of compliance in the new cuts. Russia has pledged 230,000 b/d in cuts but as we said in our OPEC meeting week notes, we expect that the Russians would gradually reduce production much as they did in 2017. Russian press reports suggest that Russia will cut only about 70,000 b/d in January, which is about one-third of its cut commitment. Saudi Arabia is more than making up for this under-compliance in January, and we expect Russia will increase its cuts in February.

Lastly, there has been little attention paid to the continued involuntary cuts from Iran and Venezuela. Platts reported that Iran production in November wasvdown by 300,000 b/d, and we think this reduction will rise by at least 400,000 b/d in December. Venezuela is expected to lose another 100,000 b/d in January from October levels. This totals an additional 500,000 b/d in cuts on top of the OPEC+ 1.2 million b/d cuts. Of course, we are not even taking into account recent news that Libyan production was halted by 400,000 b/d due to a security incident and is unlikely to be stable in the coming months.

The OPEC decision on December 7 was designed to address the oversupply in the market in 2019, and we believe OPEC and related events will more than achieve this goal. The market is suspect about of these steps due to Iran waivers and the Saudi supply surge before the US mid-term election in November. But soon the market will receive some hard data that will be difficult to ignore.