THE HEDGEYE EDGE

Is Redfin (RDFN) a real estate brokerage, a technology company or a little bit of both? The bull case depends on Redfin continuing to be valued not as a real estate broker, which they maintain they are, but rather as a disruptive technology company where profitability is a question for another day.

The fundamental RDFN short thesis has and continues to revolve around three central tenets:

- Slowing top line growth

- Disappointing operating leverage; and

- A still sky-high valuation that reflects a Tech/TAM multiple rather than a brokerage multiple.

Ultimately, we think the market will decide that this company is more traditional broker than disruptive tech engine and will value it accordingly.

INTERMEDIATE TERM (TREND)

The real estate brokerage business has been ripe for disruption for years, but many would-be disruptors have failed to cross the moat, let alone breach the industry's walls. Redfin is seen as the first company to potentially succeed where others have failed.

The residential real estate market remains highly fragmented with major brokerages Keller Williams, Realogy, and Re/Max accounting for just one third of transaction volume. Redfin has less than 1% market share, but has been steadily gaining share over the last several years by charging less and offering better technology, at least for now. The market expects, and we agree, that Redfin will continue to take share from the traditional market in the years to come.

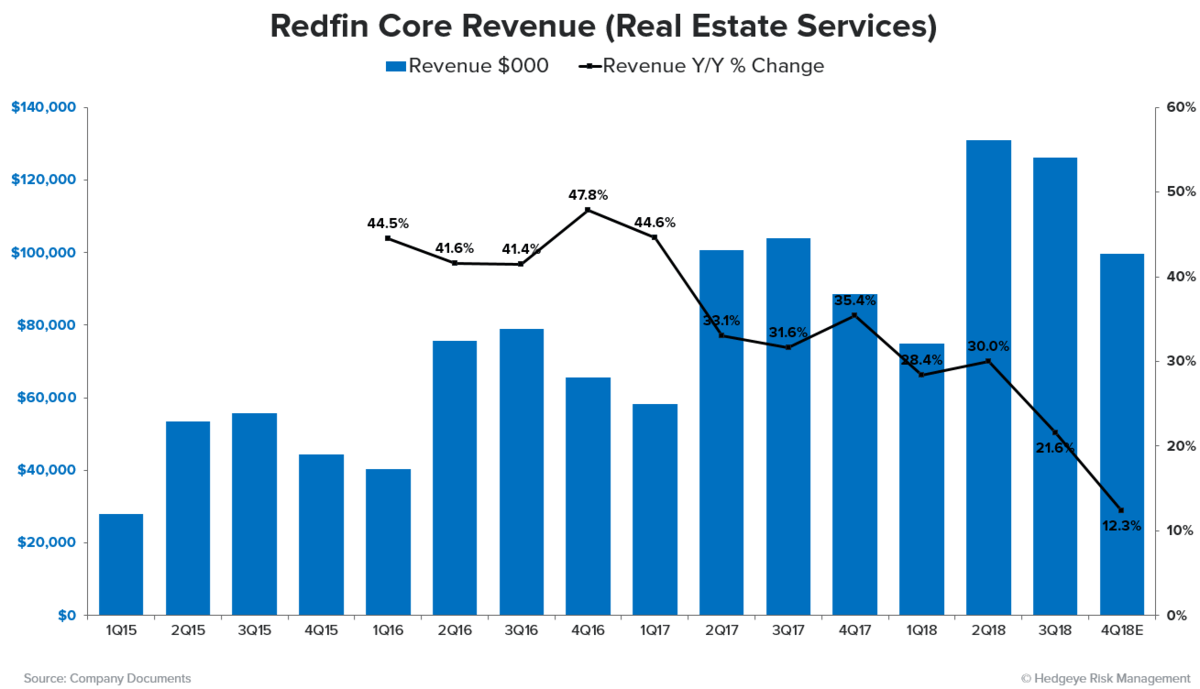

Top Line. Slowing growth has been an ongoing trend at Redfin since the IPO. The core Real Estate business growth rate is expected to be in the low teens in 4Q18. For perspective, as the below chart shows, this compares with growth in the mid-40%'s in 2016, mid-30%'s in 2017 and high-20%'s in 1H18.

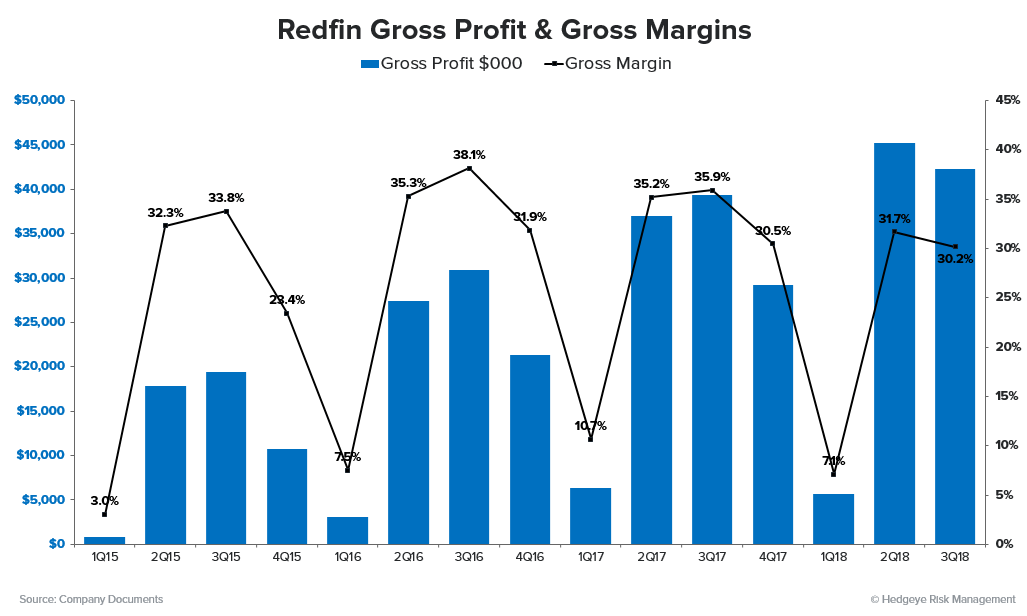

Gross Margins. Beyond the slowing top line, gross margins have shown little improvement. Firmwide gross margins have declined Y/Y in each of the last three quarters. Meanwhile, gross margins in the core business have also declined Y/Y in each of the last three quarters.

LONG TERM (TAIL)

Redfin generates neither positive net income nor positive EBITDA on a full-year basis. As such, it's a bit difficult to benchmark from a valuation standpoint. One novel approach we've undertaken is to compare it on the basis of market cap relative to market share.

Real estate brokerage competitors Realogy (RLGY) and Re/Max (RMAX) have market caps of $2.1bn and $570mn, respectively, while also having market shares of 16% and 10%. This equates to a valuation range of $60 - $130mn per point of market share. By contrast, Redfin has 85 bps market share and a current valuation of $1.35bn. This equates to a valuation of $1.6bn per point of market share, or roughly a multiple 12x that of Realogy and 26x that of Re/Max.

While it's true that Redfin has higher growth than Realogy and Re/max, consider what's implied by these valuations. Redfin is growing market share at 14-15 bps/year and currently has 85 bps market share. This trajectory implies it will take Redfin 60 years to reach 10% market share and 100 years to reach 16% market share. So either growth needs to accelerate dramatically (revenue growth has, in fact, decelerated dramatically) or the current valuation appears unsupportable.

We wouldn't go so far as to argue that $60-130mn is the right valuation. Redfin is growing, after all. But assume the company continues growing 15 bps/year for the next ten years. In 2028 they'll have 2.35% market share, which today would be worth $140-300mn vs the current valuation of $1.5bn.

ONE-YEAR TRAILING CHART