Below are analyst updates on our nine current high-conviction long and short ideas. Please note that we added Tallgrass Energy (TGE) to the short side this week. We removed Foot Locker (FL) and United Natural Foods (UNFI) from the short side. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

IDEAS UPDATES

RRC

Since we recently added Range Resources (RRC) to the long side of Investing Ideas, let's recap the most recent quarter (3Q18):

- Adjusted EPS in the quarter was $0.26 vs. expectations of $0.19. Production of 2.27 Bcfe/d equated to 14% growth YoY and 3% QoQ.

- The production profile was heavily weighted to the SW PA acreage position where production growth of ~30% YoY offset production declines in NE PA and N. Louisiana.

- Cash OpEx, including net marketing expense, increased from $1.61/Mcfe to $1.67/Mcfe QoQ due to higher midstream costs.

- Unhedged EBITDAX per Mcfe of $1.67 increased 38% YoY on a 19% increase in realized prices.

- The most important metric from our perspective is the ~$80MM the company generated in FCF ex. hedge losses and before changes in working capital. FY2018 CapEx guidance of $941MM was kept flat for the year.

We continue to believe that Range Resources offers one of the best risk/rewards in all of E&P, given the relative valuation for an asset base that has produced best in class recycle ratios and full-cycle margins for years.

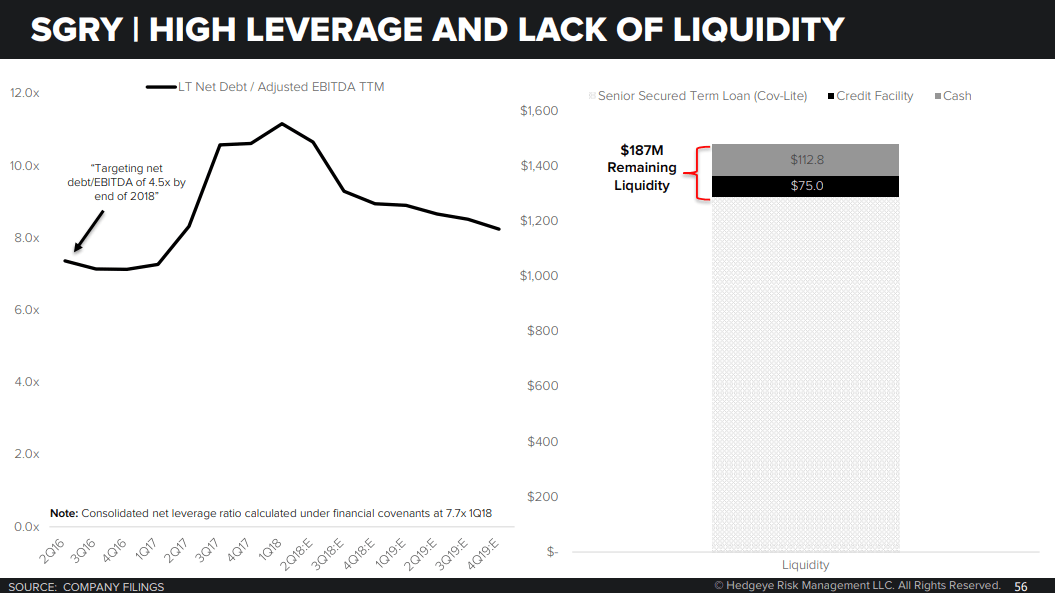

SGRY

Click here to read our analyst's original report.

We are more bearish on Surgery Partners (SGRY) following the preliminary 3Q18 release and news of incremental capital raise (which was successful). High-beta, high-leverage, no cash flow makes for a great Quad 4 short, and the stock remains significantly overvalued.

From a valuation perspective, we question how much common equity value there is given SGRY's indebted capital structure and lack of free cash flow after minority interest obligations. The company is not earning cost of capital, has limited liquidity and looming debt obligations.

DE

Click here to read our analyst's original stock report.

Deere (DE) is facing a challenging market with rising input costs, lower US crop prices, and elevated expectations. Wholesale sales have tracked ahead of retail, and pricing has been flat in recent quarters.

Meanwhile, there's a longer term structural headwind. Deere faces the youngest Ag equipment fleet in decades: The boom in Ag Equipment investment resulted in a young fleet and plenty of excess used equipment. This isn’t something that can be fixed except by time, usage, and reduced production. In other words, we reiterate our short call on Deere.

MCHP

Click here to read our analyst's original stock report.

The Microchip Technology (MCHP) long term short view is unchanged:

- MCHP is in transition from an HPA-like model to an ON-like model, with different valuation and holders lists

- The company’s pitch is no longer high-quality growth and FCF, but rather, ‘we like buying crap semis’

- What if Jimmy P (former MSCC CEO) is right in his defamation lawsuit and Steve has to recuse himself from running the company?

On bounces in MCHP, we think the company remains shortable into 2019.

GWW

Click here to read our analyst's original report.

As we go through what our Macro team calls Quad 4 (i.e. U.S. Growth and Inflation slowing), we should see growth slow and inflationary pressures ease. That should apply downward pressure on interest rates and input costs, a positive for names like MHK. We expect slowing growth, disinflation, and easing supply chain stress to be negative for names like Grainger (GWW).

We highlighted the relationship between web traffic and GWW sales growth. After all, ERP punchouts typically just launch the user’s browser to grainger.com. Web traffic reaccelerated a bit in the last couple of weeks, which was not our expectation. The comps steepen mightily (we are still comping down traffic in the most recent reading) as tax reform purchase activity drove much of the upside. This is worth watching, we think, as GWW will be facing several secular and cyclical headwinds in the next 6 months, after 3Q18 results showed fractures on toughening comps.

AVLR

The hair is still there for the Avalara (AVLR) short thesis:

- The recent lawsuit points to an innovation problem inside the company;

- The M&A path points to the same problem as most of the key functionality of the software has been acquired over time;

- The employee disaffection is real and makes us think the December lock-up expiration will be met with jubilatory selling;

- The lack of addressable market points is real in most ways: AVLR is selling an expensive version of something that is available at cheaper price points with better pricing transparency, and into a market that has a mixed opportunity set of open and closed doors.

So we aren’t willing to give this a premium by any stretch. Mid-20%s growth rate in the next few quarters will sunset by mid-2019 on a comps basis and sag to below 20% growth. There is no salvation from that corner.

GPS

Since we added GAP (GPS) to Investing Ideas recently, let’s recap the most recent quarter and explain why we continue to think this company is a short:

Weak quarter in absolute terms…deleveraging 6.5% revenue growth into -4% EBIT. But let’s face it…the fact that GPS can grow top line 6.5% in any environment is a positive callout. Old Navy strength is bullish, though the company strangely set a high expectation, implying that the brand will accelerate in 4Q against a 600bp compare. The big story is once again Gap Brand (-7% comp this Q, 200bps decel, 550bps 2 year decel). CEO Art Peck is getting fed up. He addressed Gap’s structural issues, saying ecom and outlet have been fine/healthy, but specialty…

“The specialty store channel is also a tale of 2 businesses. We have 775 Gap brand specialty stores globally. On a cash basis, this part of the fleet returns a very modest contribution. But importantly, the range from the very best to the very worst stores is extremely broad. Addressing the bottom half of the fleet could represent over $100 million of earnings contribution opportunity and it is that portion of the fleet that is dragging down the brand.”

A specific issue he noted was “A big one specifically is the real estate obligations that currently encumber the business”. That signals structural pressures around selling apparel in weak mall locations, which is very real for GPS as it has exposure to many malls. We like being short structurally impaired businesses with US macro in Quad 4 and the street still expecting positive comps and margin expansion in 2019.

RDFN

We see continued slowing growth inside Redfin Corp's (RDFN) core business:

Top Line: Slowing growth has been an ongoing trend at Redfin since the IPO. The core Real Estate business growth rate is expected to be in the low teens in 4Q18. For perspective, as the below chart shows, this compares with growth in the mid-40%'s in 2016, mid-30%'s in 2017 and high-20%'s in 1H18.

Gross Margins: Beyond the slowing top line, gross margins have shown little improvement. Firmwide gross margins have declined Y/Y in each of the last three quarters. Meanwhile, gross margins in the core business have also declined Y/Y in each of the last three quarters.

TGE

Below is a note from CEO Keith McCullough on why we added Tallgrass Energy (TGE) to the short side of Investing Ideas this week:

|

Looking for Energy Shorts? You should be. It's a Top 3 Sector SELL during Quad 4. That's why Energy stocks have been bloody dogs for Q4 to-date. One of our Energy analyst Al Richard's favorite shorts remains Tall Grass Energy (TGE). Here's an excerpt from Al's Institutional Research note recapping part of the recent quarter: 3Q18 Results Recap…… Tallgrass reported adjusted EBITDA, which now includes deficiency payments, was $220MM in the quarter, slightly higher than consensus of $219MM. Proportionately consolidated operating EBITDA excluding deficiency payments was ~$258MM, flat sequentially and +9% YoY. The company took ~$410MM of REX debt onto its balance sheet in the quarter. Leverage at TGE stands at 3.5x 3Q18 annualized EBITDA and 4.5x annualized 3Q18 EBITDA on a proportionally consolidated basis. Flows at Pony were again strong at 340 Mb/d, 2% lower QoQ and up 26% YoY. Contracted volumes remained at 309 Mb/d and haven’t moved much despite the company placing the Platteville, CO and Kansas extensions online. The GP&T segment reported EBITDA ex. deficiency payments of $15MM, -6% QoQ and -2% YoY. Freshwater volumes went to zero as WLL finished up its DJ DUC program – WLL is contracted through 2020. The North Dakota water assets did ~$7MM in revenue, or ~$14MM through the first 9 months of the year. This approximates a 5.2x EV/sales multiple on the $95MM Buckhorn acquisition. In total, the GP&T asset base has increased by ~$430MM since 3Q17 with only EBITDA degradation to show for it. Sell the bounce, KM |