Claims data this morning showed further improvement. Claims dropped 14k week over week to 442k from 456k (last week was revised down 1k), while the 4-week rolling average declined by 11k to 454k from 465k. The following chart shows the rolling average trend line. Below that we show the raw data.

It is worth noting that the seasonal adjustment factors were updated this past week, as they are annually, which had the effect of lowering claims by 10k more than they would have been under the old methodology. We think it's also worth noting that while the rolling average claims remain outside our 3-standard deviation channel as depicted in the above chart, the one-week claims data is now tracking the high side of our channel suggesting further improvement ahead. We continue to expect to see a claims tailwind throughout the Spring months (April, May) as census hiring picks up and weather-related effects dissipate.

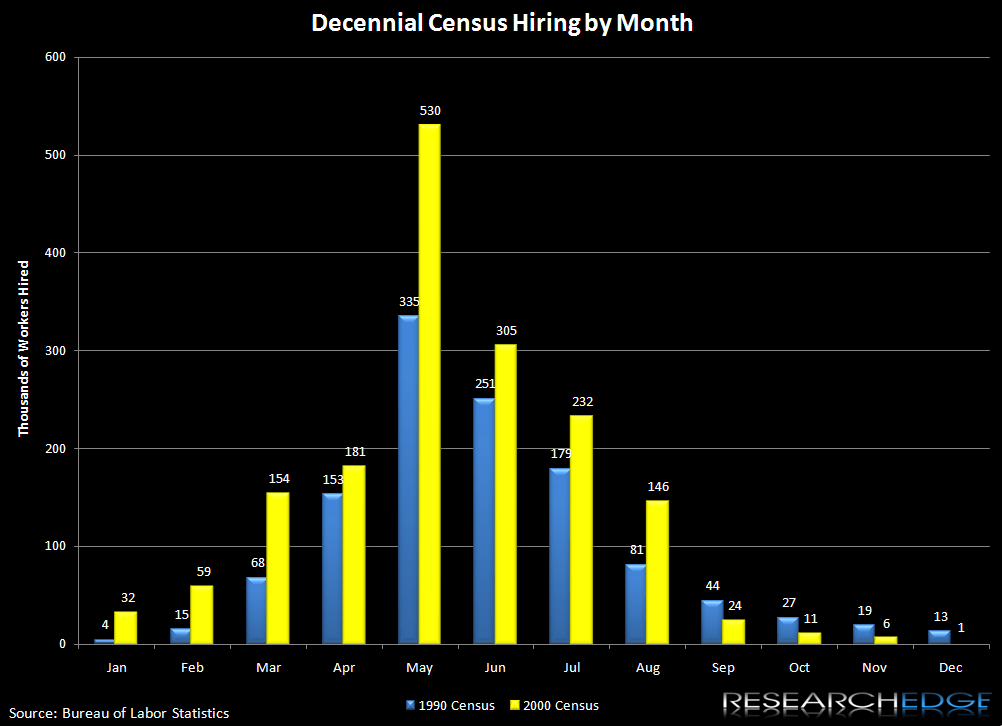

The following is the census hiring chart showing hiring in the 2000 and 1990 census by month, which should be a reasonable proxy for hiring this Spring.

Joshua Steiner, CFA

{kind=link}