The guest commentary below was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst on December 3rd.

Last week Federal Reserve Board Chairman Jay Powell blinked and thereby changed the monetary narrative. We suspect that this is just the start of a tactical retreat by the Fed in the face of mounting evidence of financial stress. Like the sailors who traveled to the New World with Columbus, Powell said something about nearing the “neutral rate” and promptly trimmed his sails for fear of encountering a reef. That reef, dear readers, is the sudden move in credit spreads.

Equities rallied and, more important, corporate bond spreads narrowed a bit last week, slowing a worrisome trend towards the repricing of credit that almost certainly implies bad times ahead. The fact of a mountain of mis-priced corporate debt has become an almost commonplace topic in the financial media. We know that bond covenants have been weakened to an absurd degree, stripping investors of assets or any legal right to the supposed security. We also know that the Fed’s manipulation of interest rates and the term structure of same has likewise distorted the pricing of risk.

Yet default rates remain extremely low, begging two questions: First, how much of the downward skew in current defaults is due to the Federal Open Market Committee? Second, how quickly will credit spreads reprice, especially with a market that is tightening by the day as the Fed’s bond purchases slowly run off. Even were Powell and his colleagues on the FOMC to do one more rate hike this year and then pause in 2019, the runoff from the FOMC System Portfolio would continue to shrink the US deposit base and thereby tighten liquidity. Thus the term “quantitative tightening.”

Unknown to most Fed analysts, Chairman Powell actually has a great deal of leeway in terms of the Fed’s “data driven” policy. Even with no further rate cuts, the liquidity in the US markets will continue to tighten apace. Every dollar of Treasury debt that runs off from the Fed’s books means a dollar’s worth of bank deposits disappears (HT to Lee Alder at The Wall Street Examiner). While many economists inside and outside of the central bank continue to waffle about the need to raise rates to enhance future “policy flexibility,” a truly bizarre construct, in fact the only decision that matters today is whether the FOMC is a net buyer of Treasury debt. Ponder that.

Next week we’ll be releasing the Q4 edition of The IRA Bank Book, which will delve into this phenomenon of domestic bank deposit shrinkage more deeply. Suffice to say that the Fed and Treasury are alter egos, two faces of the same fiscal ledger, so that what one manifestation of America gives in terms of market liquidity the other takes away.

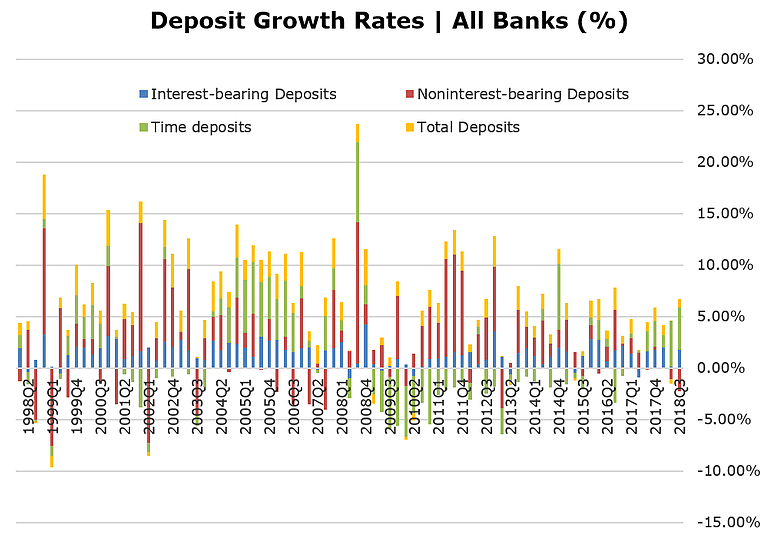

Thus in our day job we see core bank deposits trading at a healthy mid-single digit premium again after years of no premium or even discounts. And yes, non-interest bearing bank balances at US banks fell again in Q3 2018. With non-interest bearing deposits falling, offset of note by growing foreign inflows into US banks, the bias for US deposits overall is flat to down, as shown in the chart below.

Ralph on the left coast notes that the fund community is already gearing up for the opportunity to purchase busted corporate bond deals, especially the collateralized loan obligations or “CLOs” that first became famous in the financial crisis. These deals typically have a weighted average rating factor or “WARF” in single digits for “B” rated debt, meaning that if too much of the collateral in the deal is downgraded below that rating, then the covenants kick in to protect the senior debt. Ralph sees several new funds with WARFs of 50% “CCC” being created to clean up the impending mess in corporate debt.

“In nutshell, the new deals are designed to allow for up to 50% CCC with no WARF test, so they will be in perfect position to be buyers of the newly downgraded CCCs that will be puked up across the whole CLO surface,” opines Ralph. Yummy. It needs to be said that out of every market contagion, great fortunes are created. But the fact of these large opportunities to profit also attracts swarms of politicians, regulators and members of the trial bar.

Just as there is a great concentration of public companies around the “BBB” investment grade band, there also is a large pile of “B” rated crap inside CLOs that is just perfectly situated to slide down into “CCC” nowhere land at the right moment. Again, ponder the velocity of the transition from apparent credit ratings visible today to where they ought to be in a world without the Fed. Sound like 2008? The value of QE and "Operation Twist" in terms of option adjusted duration is an important question in this regard.

The gradual repricing of risk will not only bust more than a few CLOs, but may also provide some surprises in the world of investment grade credit. Consider a home owner in CT or CA or NY who has a FICO score north of 800, seven figure income and a home that in theory is worth $5 million. At the moment, however, there is no bid near that valuation. The home has a 50% mortgage on an appraised value of $4.5 million and is being rented for less than half of the monthly carrying costs.

Q: How long will the affluent home owner fund the negative carry asset?

A: We’ll find out. It's called "strategic default" by the way.

Q: What is the true loan-to-value ratio of this mortgage?

A: Higher than 50%.

Just as there is an awful lot of toxic corporate exposures inside the world of CLOs, there is also a fair amount of apparently prime credit that are, in fact, susceptible to a forced reset due to the prospect of a buyers market in residential or commercial real estate. Indeed, the current vapor lock in high end residential property reminds us an awful lot of 2005, when the real estate market began the long slide that did not end until 2012. When the loan sales volumes at WaMu and Countrywide started to fall, you could tell that the party was over. And loan volumes have been falling for years.

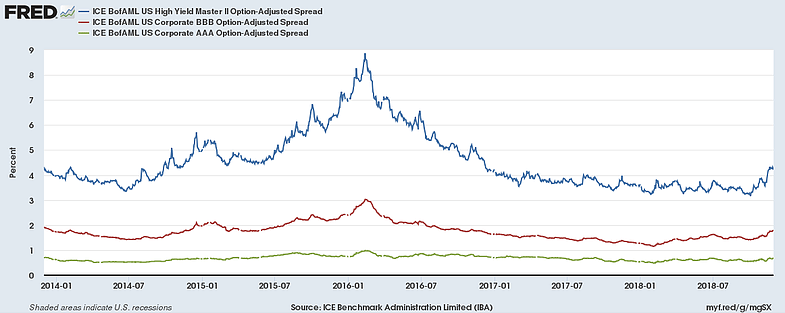

The toggle that starts the repricing process is not merely the absolute level of interest rates but rather spreads. We know that Chairman Powell and his colleagues watch many types of market indicators, but the most important and fast moving over the past month has been the rate of change in high-yield (HY) credit spreads. The folks at the Fed may want to increase interest rates to provide increased flexibility, but they are also trying to avoid a repeat of 2016, when worries about China drove high-yield spreads through the roof. Notice that even the modest uptick in spreads at the far right side of the chart was enough to almost destabilize the US equity markets.

Owing to the China syndrome in the first part of 2016, when high yield spreads rose to more than 800 bp over Treasury yields, the bond and ABS markets were basically dead for six months. Nobody on the FOMC wants to repeat that experience. In plain English, when high-yield spreads jump 20 percent in a 30-day period, you can be pretty sure that the spaceship is approaching the neutral rate. Thankfully Chairman Jay Powell noticed. Yet even his soothing words last week are unlikely to slow the exodus of investors from CLOs and corporate debt more generally.

Of note, the Fed is considering big change in how it sets US interest rates, possibly targeting the OBFR instead of the fed funds rate. But what is the OBFR? The Fed tells us that, "The overnight bank funding rate is calculated using federal funds transactions and certain Eurodollar transactions." All we can say is that Europe is short dollars and always has been. When the next idiosyncratic event strikes – Italy, Deutsche Bank, BREXIT, a New Hanseatic League – look for the dollar cost of credit in Europe to spike large.

EDITOR'S NOTE

This Hedgeye Guest Contributor piece was written by Christopher Whalen, author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington. This piece does not necessarily reflect the opinion of Hedgeye.