UA is starting to look interesting again. Today we saw two sell-side downgrades based on Valuation, and I got pinged with two separate emails about concern that apparel will hit a wall as footwear launches. I’ll never flat-out ignore valuation. But if you want to put on a short based on valuation for a company that is going to beat numbers, print accelerating top line growth at a time when growth for retail is in question, and give further evidence that the company will double in size – again – over three years, then be my guest.

I think the most interesting call out here is that ‘UA will hit a wall like Nike did when it was young.’ Something tells me that the people chirping about that thesis aren’t actually diving into the margin characteristics over the past 30-years for Nike, and comparing UA’s progression. If they did, then this would be a tough argument to make.

Why?

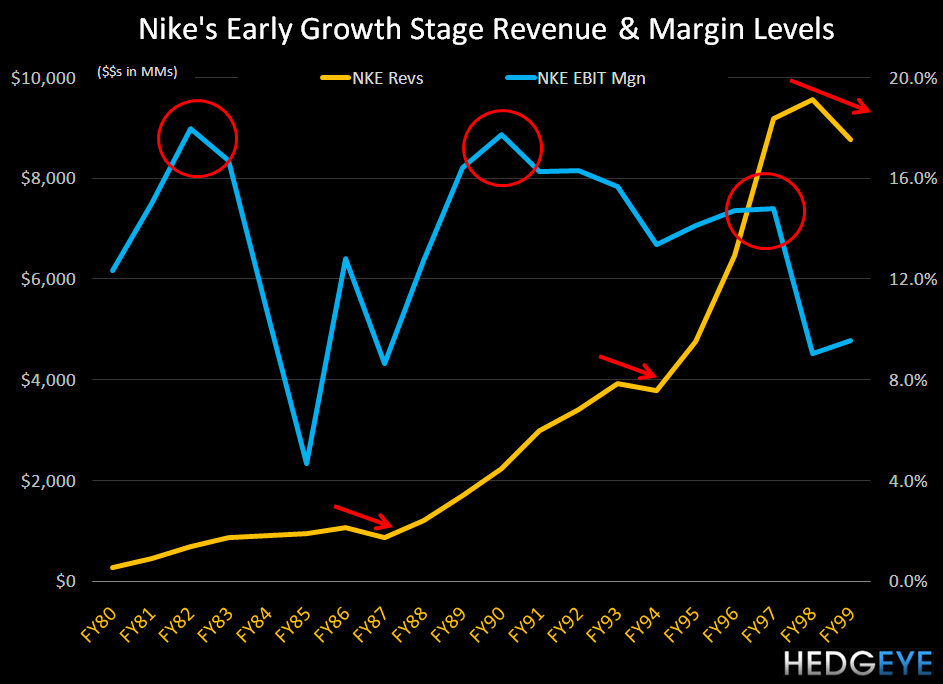

Check out the chart below. It shows Nike’s revenue growth over a 20-year period starting in the early 80s, and the margin level realized (or implemented) to achieve such growth. The bottom line is that EVERY time Nike hit a so-called ‘wall’ – such as at the initial volatilitility in building a shoe biz in the US (when a ‘sneaker culture did not exist at the time), the end of its US footwear growth burst in the late-1980s, and growing too fast in US apparel by the late 1990s – it was preceeded by a prolonged period of over-earning on the margin line. There’s no way an early cycle company in this business should be printing 15-18% EBIT margins.

To that end, can ANYONE show me ANY evidence that UA overearned at any point in time? Compare it to early Nike, compare it to ‘fad-ish’ trends where the companies don’t reinvest enough to have a sustainable infrastructure from which to grow, and then compare it best of breed companies in other consumer spaces. Seriously, UA’s behavior as it relates to capital deployment has been textbook as a baseline for success. The Street could care less about this analysis over the near-term. But we care – it usually presents great opportunities to buy great businesses when the market is freaking out for the wrong reasons.

I don’t know if I’d call UA ‘hated’, but the sentiment has definitely deteriorated. Today’s downgrades have the percent of Buy ratings down to 20%. We like that. UA is quickly making its way back towards the top of our queue.