Position: Long UUP; Short MUB and HYG

Ahead of European leaders meeting in Brussels this Thursday and Friday for an EU Summit, the media frenzy continues to beg for guidance on how Europe and/or the international community will respond to Greece’s sovereign debt issues. However, if German Chancellor Angela Merkel has her way—and she recently said there’s no need for EU leaders to make any “concrete decisions” on Greek aid at the Summit—we’d expect to see continued volatility in markets deemed to have sovereign debt issues, and carry-over weakness in the EUR versus the USD.

With respect to the work we’ve done outlining Sovereign Debt in recent weeks, both at home and abroad, we recently came across a great chart from Stratfor (first chart below) that outlines unit labor costs across Europe, including the US as a frame of reference. What the chart helps quantify is one of the many metrics that demonstrate the uneven nature of Eurozone countries, in this case regarding labor efficiency, or lack thereof in terms of the PIIGS. Note the ~ 25% spread between Germany and Greece.

While we don’t have a crystal ball to predict how this will all end, we’ve positioned ourselves in our model portfolio to take advantage of, or steer clear of, some of these macro moves. We’re long the US dollar (UUP), a proxy for taking advantage of EUR weakness; short US municipal bonds (MUB) and short high yield corporate bonds (HYG).

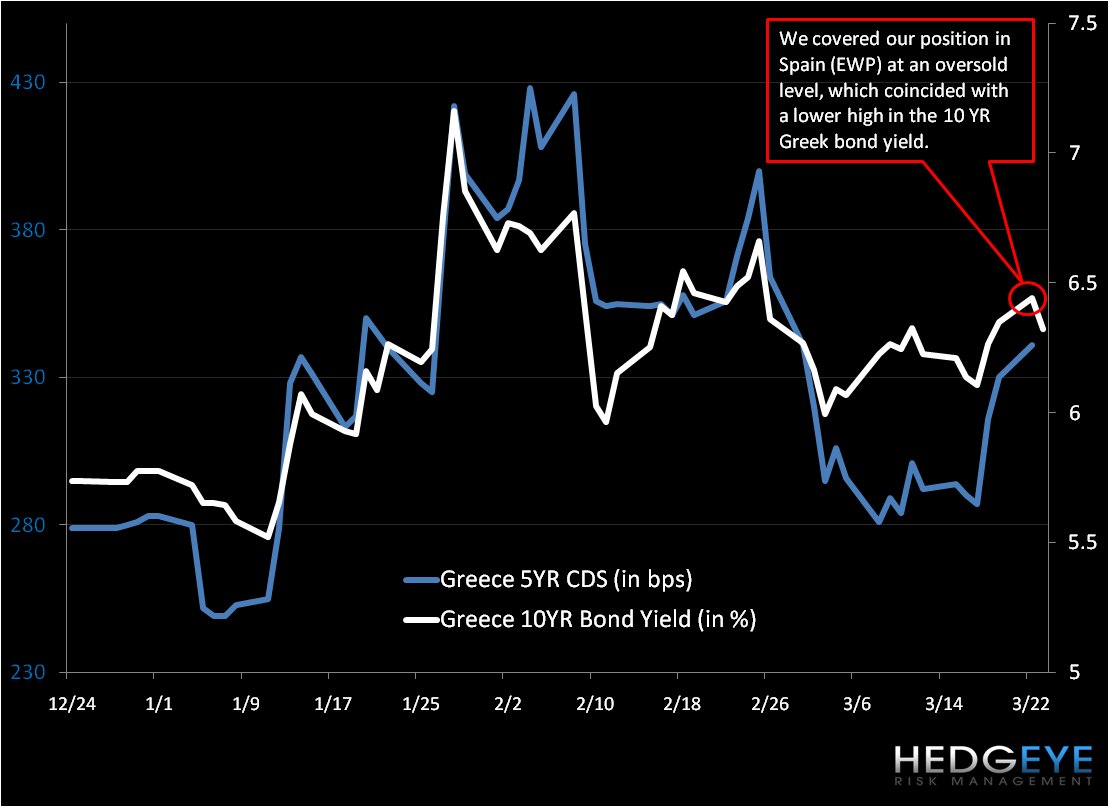

The second chart below of Greece’s 10YR bond yield and Greek 5YR CDS prices demonstrates that heightened fears surrounding Greece (and the PIIGS) persist, even post PM Papandreou’s global road show to garner economic support earlier in the month. You’ll note that we covered our tactical short position in Spain (via the etf EWP) at an oversold level on 3/22, which coincided with a lower high in Greece’s 10YR yield.

Matthew Hedrick

Analyst