Below is an excerpt transcribed from a recent conversation between MacroVoices podcast host Erik Townsend and Hedgeye CEO Keith McCullough.

* * *

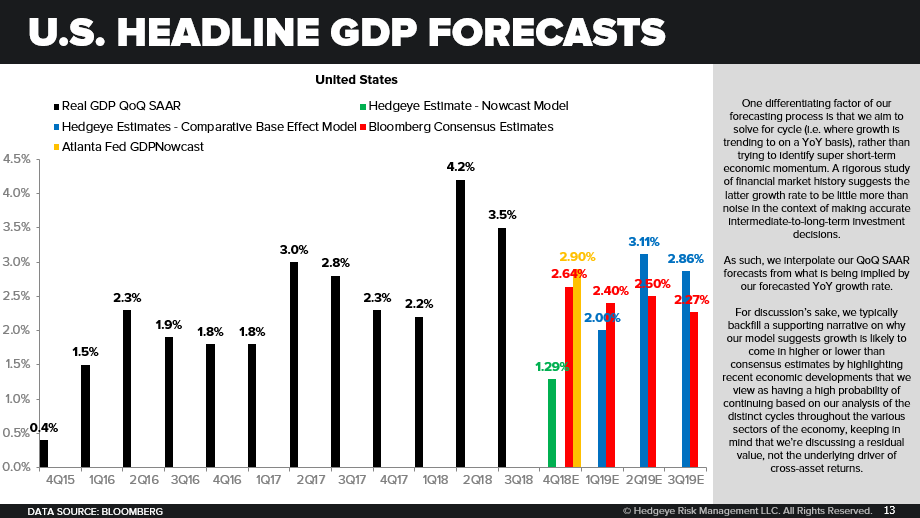

Erik Townsend: So let’s just put this in perspective. Because you’re talking, at least in your 1.29% figure, about a major, major miss on expectations if you’re right. Does that leave you outright short the market? And if you look at what’s happened – some people think that maybe we’re going to see a bounce into year end and if you wanted to get short it’s not time yet. Is it time to be short? And where do you see this going? Because I would think if you’re proven right and the 1.29% comes true, we’re going lower after that data comes out.

Keith McCullough: Oh, yes. And we’re going lower into this because of that number coming out. I don’t mean the news reconciles why we were going down. And the answer is absolutely yes. I mean, I’ve written multiple notes in the last six weeks saying, yes, I still believe what I believe. God forbid I believe what my model tells me, and it told me the same thing on the way up that it’s telling me on the way down. At the same time you should have conviction in a process and a model.

So the key here Erik is, of course, selling the stuff that goes down most. And, whether it be tech, really – on Slide 8 we show you what it is at the equity sector level, it calls to short on bounces, tech, industrials, and energy. Those are the three big short calls. And then the other side of it, what this model tells you to do, is buy things that look like low beta or bonds or bond proxies. So it’s buy utilities, buy REITs, buy consumer staples. So you don’t have to be out of the market. You have to be out of the things that everybody else is long in the market. And you have to go buy the things that everybody else is underweight.

So that’s an easy thing for me to understand because, of course, I’m basically shorting the things that I liked and I’m buying the things I didn’t like. The next big part of this, I think, is on Slide 14. Especially on those bond proxies and long-term bonds. I know a lot of people are bearish on long-term bonds. There are a lot of famous people that don’t like bonds. I’m not famous, but I didn’t like bonds either. Now I do. The main reason is because bonds over the course of the long term, intermediate to long term, tend to go where inflation is going.

So our forecast on inflation, I’d say it’s a layup, you know, by Q1 of ‘19 falling below 2%. We’re at 1.76%. And that of course is the layup now, because oil has just crashed. So oil is the heaviest weight in that model. So I want to be acutely positioned for that. And you can obviously be long long-term bonds if you’re bearish on inflation. I think that Wall Street can come to us on that metric as well.

Erik: I really, really want to encourage our listeners, particularly newer listeners, to study the entire chart deck. And if you’re not familiar with some of the Hedgeye process, listen to Keith’s interview from a year ago when we went into a lot of detail on this. I’m going to skip ahead again to Slide 23 where we get into what you’re actually looking for in terms of Q3 2018 Macro Themes. Walk us through these three themes and why they’re important.

Keith: A theme is important when it’s new and then it starts to trend. So our call on the US dollar when we called the dollar breakout in April – and then we reiterated in Q3 that the dollar should strengthen at this point. So we’re going to stay with that. And as much as shorting in emerging markets on all bounces to lower highs. So, again, if you’re a Hedgeye power user you know what to do at the top end of the risk range, which we publish daily. That’s where you make your sales. You don’t sell them just because they’re up. You sell them when they’re up and at the top end of the range.

A good example of that, obviously, is the four-day US equity bounce that we had coming out of the mid-term election. We wrote a note that said huge selling opportunity. So, again, that’s what it is. Have interest rates peaked? I think that’s the biggest call left that has not yet worked in a meaningful way, but I do think that the 10-year bond yield is about to break. I just need it to break 3.05% on the 10-year yield. I think there is a trap door underneath that towards 2.5% on the 10-year yield. And I don’t think everybody else thinks it can go there. At least they haven’t published that forecast. Maybe there is somebody. If they want to be in my lonely corridor with me on that, then that’s great. Quad four is the bigger theme, which is on Slide 24 – we’re just rolling through –

Erik: Hang on one second, Keith, before you go on. Let’s come back to rates because there is such a chorus of people that are just so convinced – look you saw the breakout past 3.10– 3.12%, whatever you want to call the magic number on the 10-year. It got all the way up to 3.20-something, came back and retested that 3.12 level as support. It held, moved higher. There are so many people that just say, that’s it. The secular bond bear market is upon us. Give us the rationale. Why do you disagree on a fundamental level those views?

Keith: Well, one, the easiest way that I always disagree is that most people are just looking at a chart. I mean, there’s a lot more to this than just looking at a chart. And anybody can look at what I affectionately call the 200-day moving monkey or the 50-day moving monkey. And they are one-factor models. We get it. If you pull the chart back far enough on 10-year yields, you can get – almost every traditional technician is going to tell you it was a breakout inasmuch as every technician, Erik, as you know, has told you that the Russell looked fine at the end of August and so did the Nasdaq. Subsequently they’ve both gone down on the order of 12–15%. Now the charts look bad.

So that’s the whole point of having a research process that front runs the turns in the technicals. And that’s, really, when I look at it – I don’t look at other people’s technical, I look at my own quantitative signals. As I pointed out, as inflation data points come out lower, I think the Fed is going to go from hawkish to dovish. So I think they’re going to raise rates for the last time in December. And if they continue raising rates during the Quad Four slowdown, the stock market is going to continue to go down faster and they’re going to have to eventually cut rates faster anyway.

So I really think that in the next three to six months all my catalysts are really in the forward-looking outlook. And today it would be very hard for people that don’t agree with me to see those things, because people that see those things are just looking at a chart – you know, once they start to hear the Fed turning from hawkish to dovish. And then eventually the Fed is going to have to start cutting interest rates again. It will be way too late to be buying long-term bonds. And that’s effectively the point when I look at that.

Another big thing that people call out is, of course, the gargantuan amount of Treasury issuance. All the reasons why we could have given you to be bearish on bonds and bullish on bond yields for two and a half years are clear. Bonds have been going down for three years – long-term bonds have – for a reason. And so has the short end of the bond market as well. I just think the cycle has peaked – again, on inflation but also on growth and also on earnings. So the three-legged stool of peaks called the triple peak is the main reason why we have that outlook on bond yields going lower, taking lower highs effectively from that 3.25–3.23% level for a year now, for that matter.