“Every man takes the limits of his own field of vision for the limits of the world.”

-Arthur Schopenhauer

And… every “visionary” can lose all of his (or other people’s) money too! The aforementioned quote comes a book I cited at the peak of the Bitcoin Bubble, The Age of Cryptocurrency, where the authors (WSJ guys) were talking up the alleged “asset class.”

Whether it was another US Semiconductor company (NVIDIA) continuing to #crash last night on the “collapse of crypto mining” or Bitcoin’s epic eradication of market cap from its prior 2018 lows, you have to ask yourself why you haven’t pivoted to safety.

Safety – you know, as in a safer, lower-beta, lower-volatility portfolio of assets… instead of a tweet-centric book of alleged Chinese “trade deals” and speculative equities and/or credits who have bad balance sheets and Quad 4 Cycle @Hedgeye TAIL risks.

Back to the Global Macro Grind…

Not every man and woman “limits their field of vision” to the assets and liabilities that other men and women are paid to promote. Call us the Data Dependents. Call us The Cycle People. Call us whatever you want, but don’t call us crashing.

“Nice call on Quad 4 but we’re not really seeing it in credit yet…”

-Credit and Equity PMs in October

And, now that I’m back from Toronto and Boston, my team has me scheduled to do conference calls with 3 separate Credit Hedge Funds today. I guess we’re seeing it in credit now!

Is GE really a “Triple B Credit?” Is the approximately $2.5 TRILLION in “BBB” paper out there not some form of an “imbalance” and/or bubble? Like from the crypto crowd back in DEC of 2017, I don’t expect to receive positive mail on this topic today.

As long-time subscribers to our 4 Quadrant Risk Management #process know, when the US economy enters Quad 4, you short, sell, and/or de-risk the following 3 exposures in Fixed Income:

- High Yield Credit

- Junk Bonds

- Converts and TIPS

And you buy US Treasuries, across the curve. If you’ve already shorted any or all of those exposures in November against a portfolio of UST Bonds, you’re beating at least 80% of the Credit Hedge funds out there.

Yes fellow Data Dependents, the goal of the game is to beat the competition. Inasmuch as making these portfolio pivots in Fixed Income have mattered, so have the pivots you’ve made in your equity portfolio where the Top 3 Shorts remain:

- Momentum (MTUM)

- High Beta

- Tech (XLK) and Semiconductors (SMH)

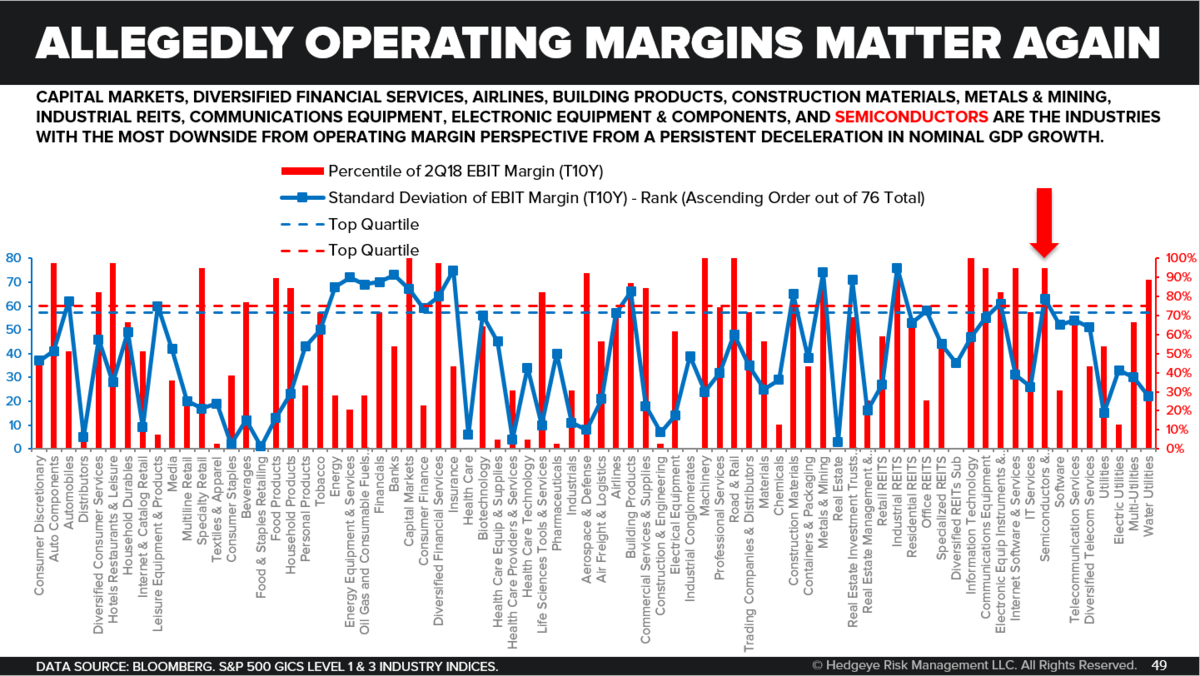

On that last point, how many hedge funds started shorting Semiconductors (SMH) as they were peaking alongside the “globally synchronized recovery” back in Q1 of 2018? Instead of trying to justify holding Semis on “valuation”, they must be killing it!

Semis (SMH) actually peaked on March 12th of 2018. If they open where NVDA and AMAT (both guided lower last night) are trading this morning, Semis will have already had a -18% draw-down from their Cycle Peak.

Since #CyclePeaks is the #2 Macro Theme for Q4 (next to #1 Quad4 in Q4), I’m pretty well versed in the bear case for a cyclical slow-down and/or collapse in cyclical Tech earnings.

“Oh, but I’m not long those – I’m long Secular Growers.”

-Equity PMs in October

While that sounds totally cool, I have to ask one basic question – what is a Secular Grower that has not yet seen a cycle?

We already know that Facebook (FB), Amazon (AMZN), and Apple (AAPL) are guiding to cyclical slow-downs in both revenues and earnings. And that’s AFTER a record 9 straight quarters of top-down US GDP Growth #accelerating!

How do you think these companies are going to do when the Tech Sector (66 companies in the SP500) has to cycle against the #CyclePeak EPS (year-over-year) growth rate of +32% of Q2 of 2018 in Q2 of 2019?

Whether you’re buying speculative Tech, Momentum, or Credit you absolutely have to have some respect for The Cycle and how it will impact equity multiples and credit spreads when The Cycle slows.

Or you don’t, and you can just get mad at me like limited-field-of-macro-rate-of-change-vision Bitcoin Bulls did.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND views in brackets) are now:

UST 10yr Yield 3.05-3.19% (neutral)

SPX 2 (bearish)

NASDAQ 7040-7419 (bearish)

Utilities (XLU) 53.50-55.56 (bullish)

Consumer Staples (XLP) 55.04-57.10 (bullish)

VIX 15.75-23.39 (bullish)

USD 95.65-97.76 (bullish)

GBP/USD 1.26-1.30 (bearish)

Oil (WTI) 54.40-60.60 (bearish)

Copper 2.65-2.79 (bearish)

AAPL 183.66-199.97 (bearish)

AMZN 1 (bearish)

FB 138-150 (bearish)

Bitcoin 5005-6046 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer