This week we will be getting some incremental data points on the health of the casual dining space from DRI earnings on Tuesday and Brinker’s annual analyst meeting on Friday. In both cases I expect the news flow to be positive.

Over the past 90 days, casual dining stocks are up an average of 34.9% while quick service stocks are up 21.8% on average. The outperformance is attributable to the data; consumer confidence trends are showing that consumers in higher income brackets have higher levels of confidence. Additionally, a relative improvement in higher-end retail sales (Tiffany’s today and Nordstrom in February), as highlighted by our Retail team, has been observed recently. Household income is also picking up disproportionately at the “high end of the income spectrum”, according to J.P. Morgan’s investor day (highlighted by financials sector head, Josh Steiner, on 2/25). Management commentary from chains like PFCB also suggests that business expense expenditures may be picking up.

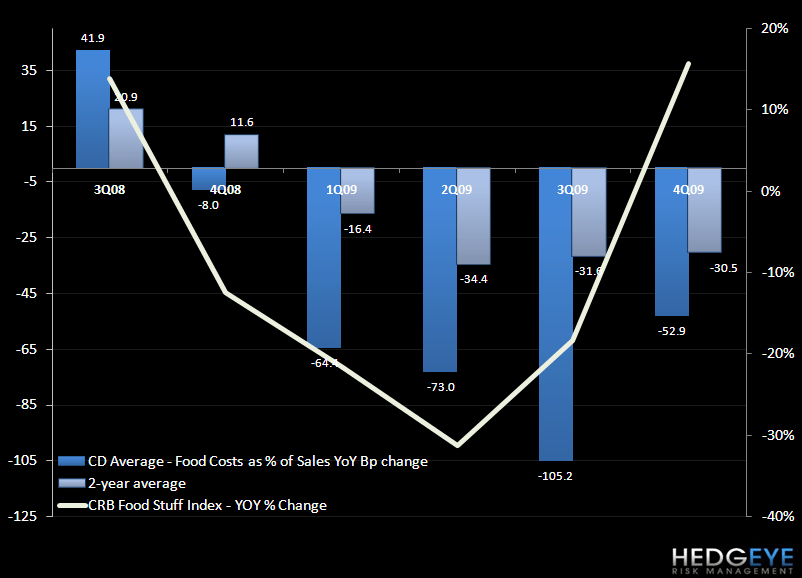

Coming into the summer months, the trends in top line sales will take on increased importance for overall stock price performance. Casual dining, like quick-service, is facing some notable operating cost increases, on a year-over-year basis, particularly in the third quarter. As seen in the chart below, declining food costs have been a significant tailwind for the industry in 2009. The benefit from lower food costs began in earnest in 1Q10, but the favorability accelerated throughout the year peaking in 3Q09. It’s impossible to make a blanket statement about every restaurant company and the impact of foods costs on the P&L, but it is helpful to look at a broader measure of food cost trends.

Given that most companies contract out a year or more (in some cases) for 75% or more food costs, the timing of higher foods costs impact on the P&L is delayed by six months or more. The broadest measure of overall food inflation, The CRB Foodstuffs Index, is trending upwards and is likely to remain at elevated levels for the next few quarters (currently at +15.7% YoY) given that 2Q09 saw a decline of -30% YoY for the Index.

Given the current trends, 3Q09 will be a very difficult quarter for the industry from a cost stand point, putting incremental pressure on the sales trends to continue to improve.

Additionally, it’s not likely that labor costs will provide any tailwind for Casual Dining operators. Unionization is not currently in the media’s crosshairs but it is probably going to be a focus of the current administration at some point in the next three years. It is also worth considering the chart below; labor costs are growing at a steady rate on a two-year average basis.

EBIT margin trends, shown in the chart below, vividly illustrate the benefit of cost cutting and lower food costs that occurred through 2009. As it stands now, it’s is not very clear where any margin tailwind will come from unless there is positive traffic trends and incremental pricing. Labor cost trends are not promising and food costs look set to increase as a percentage of sales in the middle and second-half of next year. As a point of reference, EBIT margins rose 110 bps in 3Q09 and 120bps in 4Q09; it will be difficult for the casual dining chains to match these levels of margin expansion.

Sales trends in casual dining are showing considerably more stabilization that in quick service restaurants. We are hearing that February and March same-store sales results continue to improve on a sequential basis. On a two-year average basis, sales trends in January improved by 380bps from December, to -3.2%. The improvement is impressive despite the fact that unemployment, the increase in the savings rate, and inflationary consumer prices are all a potential drag on spending patterns.

It seems that, as PFCB management alluded to, an improvement in “expense account” spending could be helping trends at casual diners. While consumer confidence among higher income brackets is currently providing a boost to casual dining, a reversal in the overall stock market could quickly change this. Darden restaurants is reporting after the close Tuesday and I will be eager to hear what commentary, if any, they offer on current trends in early fiscal 4Q10.

Howard Penney

Managing Director