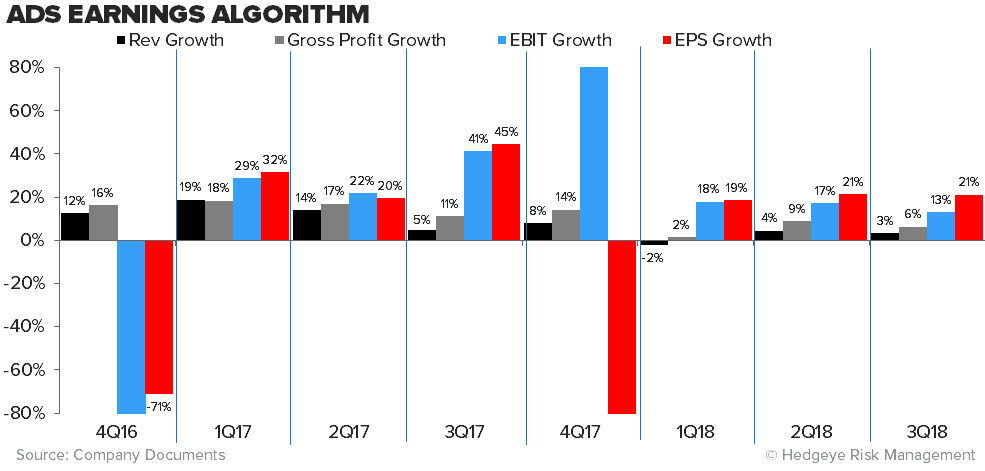

I like what I saw this quarter from Adidas. I know…revenue was weak. Never a good thing. But this company is weathering the European slowdown better than anyone out there. In the quarter it put up 8% constant currency top line, which translated to a ‘meh’ 3.5% growth on a reported basis. Growth was very balanced between apparel and footwear (+9% and 8% in the quarter, respectively). It absolutely killed the gross margin line, reporting a 140bp improvement and that INCLUDED a 130bp hit from FX. Ultimately we’re looking at 21% EPS growth for a company being hit by a global economic slowdown and currency headwind (which is set to inflect to a tailwind). This management team is pulling all the appropriate levers to deliver the goods – something I have not seen Adidas do in my career of following the business.

The thing I don’t get is that Nike is pitching it’s story as ‘full steam ahead’ in the US, Europe, and China – AND people are paying near 30x earnings for that (despite the fact that its partnership with Flextronics to reshape the manufacturing paradigm just evaporated). Adidas is being very pragmatic about the environment it’s in…not blaming weather or macro…but is simply holding itself accountable to every put and take in every geography. Management comes across to me as very believable and dare I say trustworthy (again, something I’ve never said about the C-suite at Adidas).

Why do people give Nike the benefit of the doubt? Because, to be fair, it’s earned it after a decade of pulling appropriate levers to drive a consistent financial model. Adi only has a year under its belt, and now you have to believe that management accelerates its top line in ’19 and/or ’20 to hit its stated goals. Let’s not forget that it has the same DTC optionality as Nike – and that FX inflects next quarter positively for Adidas. In fact, e-comm was up 76% in the quarter. Bear case is that it is overdistributing Yeezys. Fair point. But management has seen Nike’s Jordan gaffe over the past three years and I don’t think it will follow suit in cheapening up the brand by flooding the market.

This comes down to a management call, and I think this team will deliver mid-high teens EPS growth consistently as it optimizes a perennially mis-managed franchise while closing the profitability and return gap with Nike. The market might not like it today, but this story is simply more believable to me than Nike right now – and its trading at a 30% discount with less blow up risk.