Each nation feels superior to other nations. That breeds patriotism - and wars.

- Dale Carnegie

On the MACRO front, continued concerns over sovereign credit in Europe seemed to be the driving theme behind Friday’s decline. The Greek PM suggested that Greece might have trouble accessing the market in order to refinance its debt later in the spring. According to street account, “In a speech mostly for domestic consumption in front of one of the Greece’s unions Papandreou raised the stakes in a competitive game of political posturing.”

The Germans aren’t buying it. According to Bloomberg, “German Chancellor Angela Merkel told investors they shouldn’t expect this week’s European Union summit to agree on assistance for Greece, resisting calls for the specifics of a rescue plan and helping send Greek bonds to their lowest in more than three weeks.”

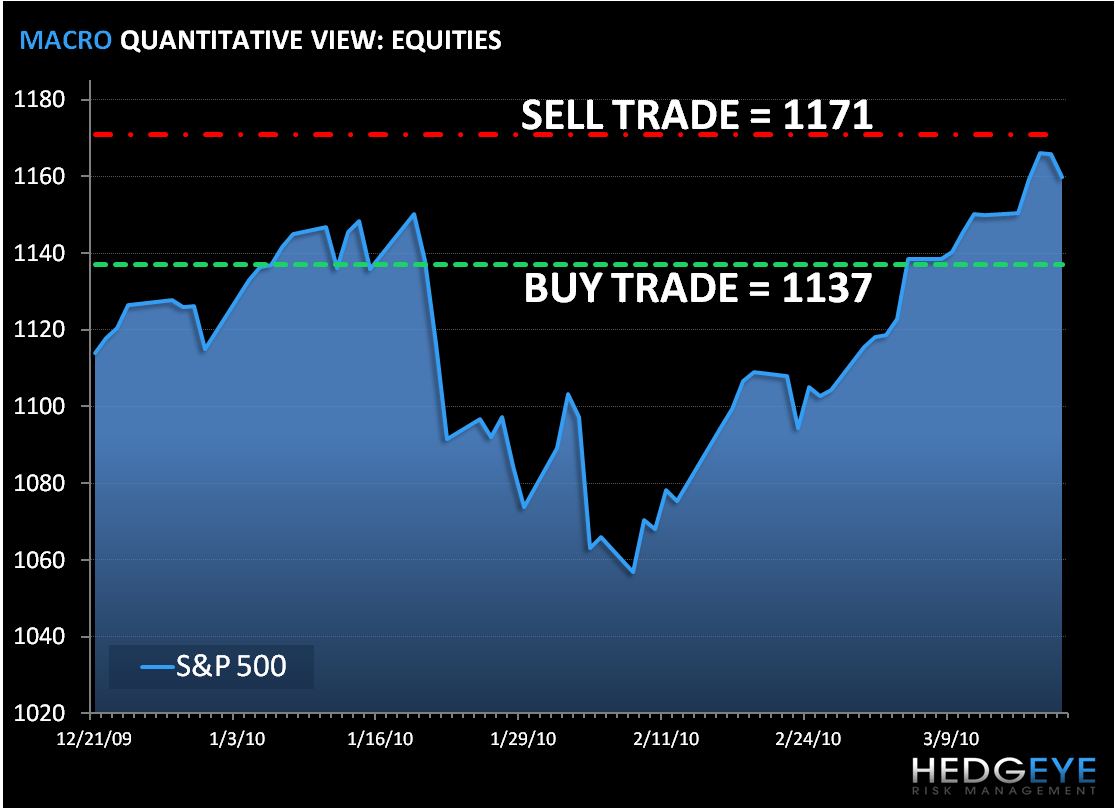

The S&P 500 declined by 0.5% on Friday, but was up 0.8% for the week. While the S&P traded within a relatively narrow range, the breadth continues to decline as small caps underperformed large caps on the day. Every sector declined on Friday and only two sectors outperformed the S&P 500.

Also on the MACRO front, India raised its repurchase rate on Friday, which was a surprise and a concern for US equities. Further, India central bank Governor Duvvuri Subbarao also alluded that he’ll likely raise rates again next month.

Although down slightly on Friday, Healthcare (XLV) was the best performing sector, along with Consumer Discretionary (XLY) and Consumer Staples (XLP) on Friday. Many cited reduced uncertainty regarding healthcare reform as providing support for the sector. Managed health preformed well; the HMO index was up 2.7% on the day.

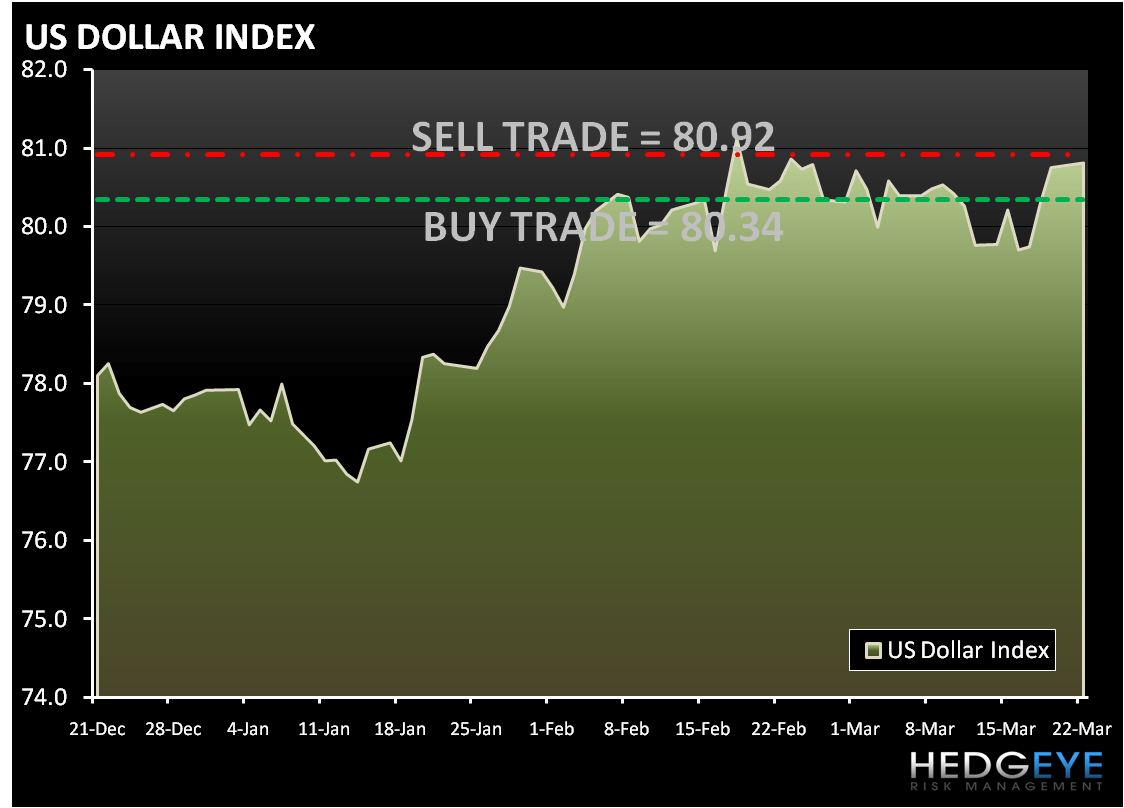

The Dollar index was up 0.62% on the day and 1.1% on the week. The Hedgeye Risk Management models have levels for the Dollar Index (DXY) at: buy Trade (80.34) and sell Trade (80.92). The strength in the dollar knocked down the REFLATION trade and related sectors. On Friday the three worst performing sectors were Energy (XLE), Materials (XLB) and Utilities (XLU).

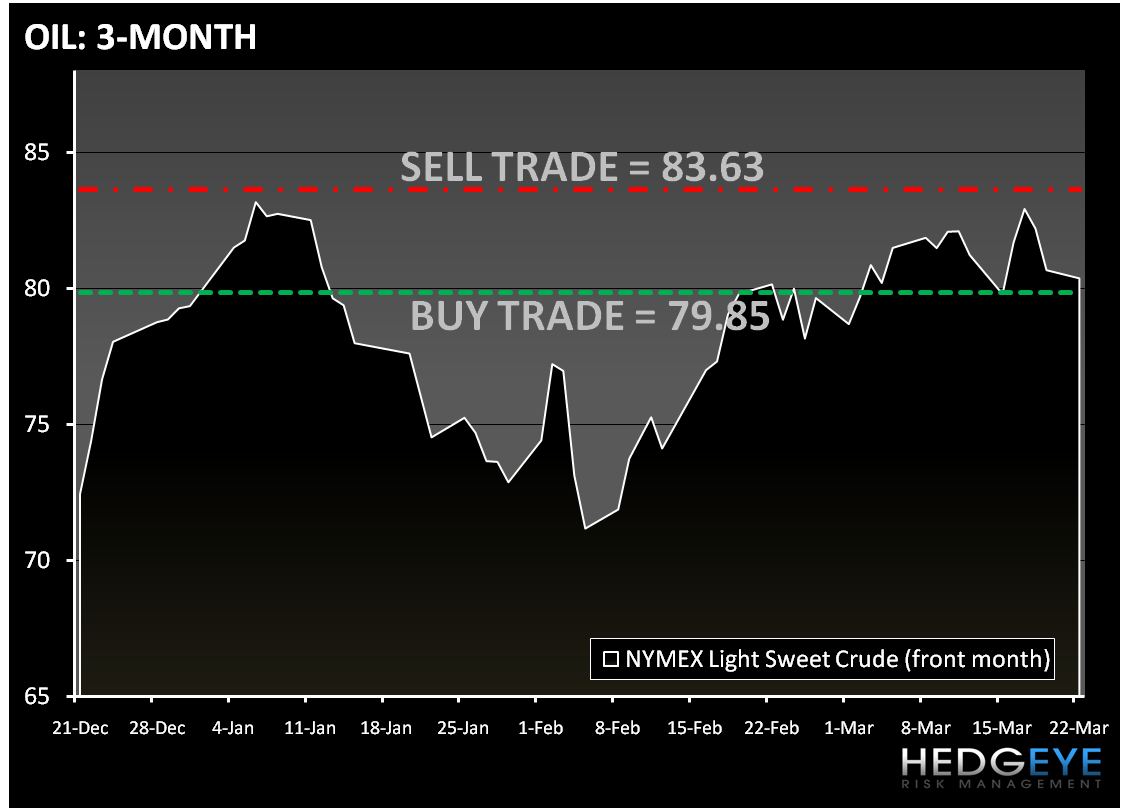

The strength of the dollar and Crude's big drop (1.8%) on Friday provided significant pressure on the XLE and the XLB. In early trading, Oil is trading down below $80 a barrel. The Hedgeye Risk Management models have the following levels for OIL – Buy Trade (79.85) and Sell Trade (83.63).

Last week Technology (XLK) was also a notable underperformer. Last week the XLK underperformed the S&P 500 by 70bps. On Friday, PALM reported disappointing earnings and provided guidance significantly below expectations; smart-phone sell-through was well below expectations. The SOX declined 1.7% on the day.

The VIX gained +2.1%, although off its highs at the close and closed down 3.5% for the week. The VIX continues to be broken on all three durations - TRADE, TREND and TAIL. The Hedgeye Risk Management models have levels for the volatility Index (VIX) at: buy Trade (16.39) and sell Trade (18.79).

In early trading, equity futures are trading below fair value after the House of Representatives approved a bill overhauling the health-care system in a 219-212 vote and India’s interest rate increase. The US MACRO calendar is void of any significant events.

In early trading, copper in Shanghai fell by the most in a week as supplies expanded significantly. The Hedgeye Risk Management Quant models have the following levels for COPPER – Buy Trade (3.31) and Sell Trade (3.43).

In early trading Gold is trading lower as the Dollar is trading near a three week high. The Hedgeye Risk Management models have the following levels for GOLD – Buy Trade (1,096) and Sell Trade (1,120).

Restless Howard Penney

Managing Director