Takeaway: There wasn't anything in the print or on the call to suggest that mgmt wasn't just clearing the decks for 2019; especially considering the nonsensical assumptions embedded in its guidance.

UPDATE

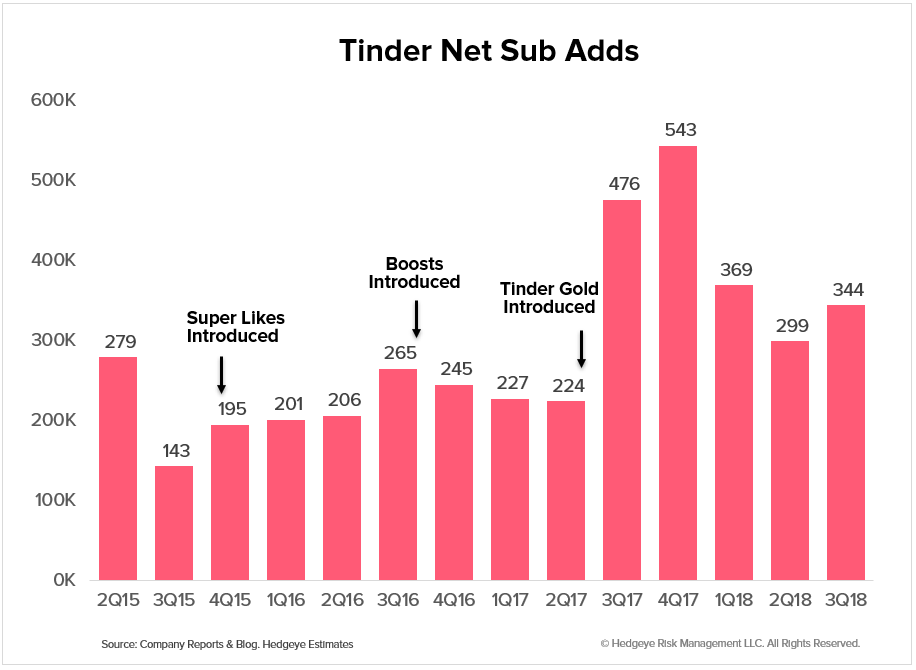

- 4Q18 Sub Guide = Also Sandbagged: Mgmt suggested that 4Q18 Tinder sub adds will come in below its historical average of 200K-250K given elevated contract terminations from Gold signups in the prior year period. A couple things to consider here. There were only 67K incremental net sub additions in 4Q17 vs. 3Q17, so if this was really an issue, we should have seen this manifest in the 3Q18 print as well given that Gold was the source of the sub surge in both periods. But as we mentioned in our prior note, MTCH saw an acceleration in 3Q18 gross adds, which also means it probably ended 3Q with the subs it guided to for 4Q18 (MTCH reports average not ending subs). Once again, our tracker suggested that MTCH was off to a relatively muted start to 4Q18 in terms of sub adds, so we suspect mgmt chose to guide to what it knew it could definitively beat (i.e. what it already has) rather than risk a miss on 4Q18 sub estimates that jumped the gun following the 2Q18 print.

INITIAL TAKEAWAYS

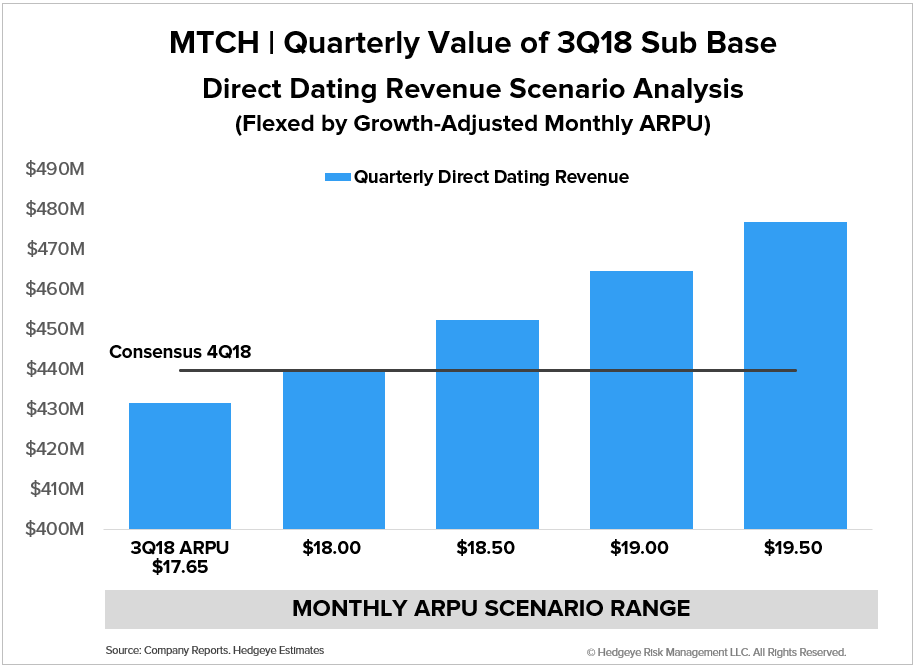

- 3Q18 = Clean Print: We're going to be brief here since the next two bullets warrant more attention. MTCH produced revenue and EBITDA upside, subscribers beat on accelerating total and Tinder net adds, including the non-Tinder brands that produced its largest net gain since 1Q16. We also estimate that MTCH ended 3Q18 with enough subscribers to exceed 4Q18 consensus revenue estimates leading into the print.

- 4Q18 Revenue Guide = Sandbag: MTCH's guide at the mid-point is basically calling for no sequential revenue growth, which would be all but impossible even if MTCH didn't pick up any new subs in 4Q18. Remember that MTCH hasn't received a full quarter's worth of revenue from its 3Q18 subs adds, which means that the quarterly revenue run-rate from its reported sub base is higher than what MTCH reported for 3Q18 revenues. That said, MTCH's guidance actually translates to declining 4Q18 subs, which seems beyond reason, even before considering that it ended 3Q18 on a particularly strong note given its strength in net adds (MTCH reports average subscribers not ending). Mgmt may point to Fx, but that is predominately a y/y headwind that can't explain the screeching sequential halt implied by its guide. In short, either the wheels are suddenly falling off the bus, or mgmt is making sure that consensus doesn't get too far ahead of its skies for 2019 (as they did following the last print) following another quarter of particularly strong net adds.

![]()

Let us know if you have any questions or would like to discuss further.