The crux of our call on GIL revolves around the company winning new private label apparel contracts across retail channels – everywhere from Walmart and Target to Amazon – as it flexes its muscle as the low cost producer with its first new manufacturing facility in five years. Timing there is perfect and is not by accident. The company saw this sea-change coming, built an asset (that went live in June) and will profitably undercut anyone bidding for this business due to its structural cost advantage.

To that end, I’m looking for evidence that 1) the company is successfully selling the new capacity, and 2) its base business is healthy. There was some noise in the quarter – as we expected – around the hurricane impact on the business given that GIL’s US ops are based in the Carolinas, but overall the base business is solid in units, pricing and inventories. On top of that, it announced a new private label deal at Wal Mart -- the fourth such deal it secured over the past four months (others included a Price Club and Sporting Goods retailer).

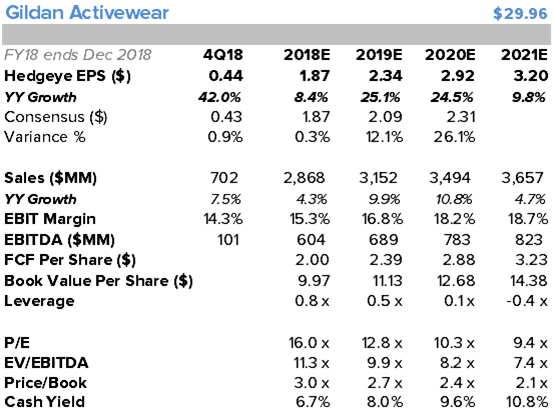

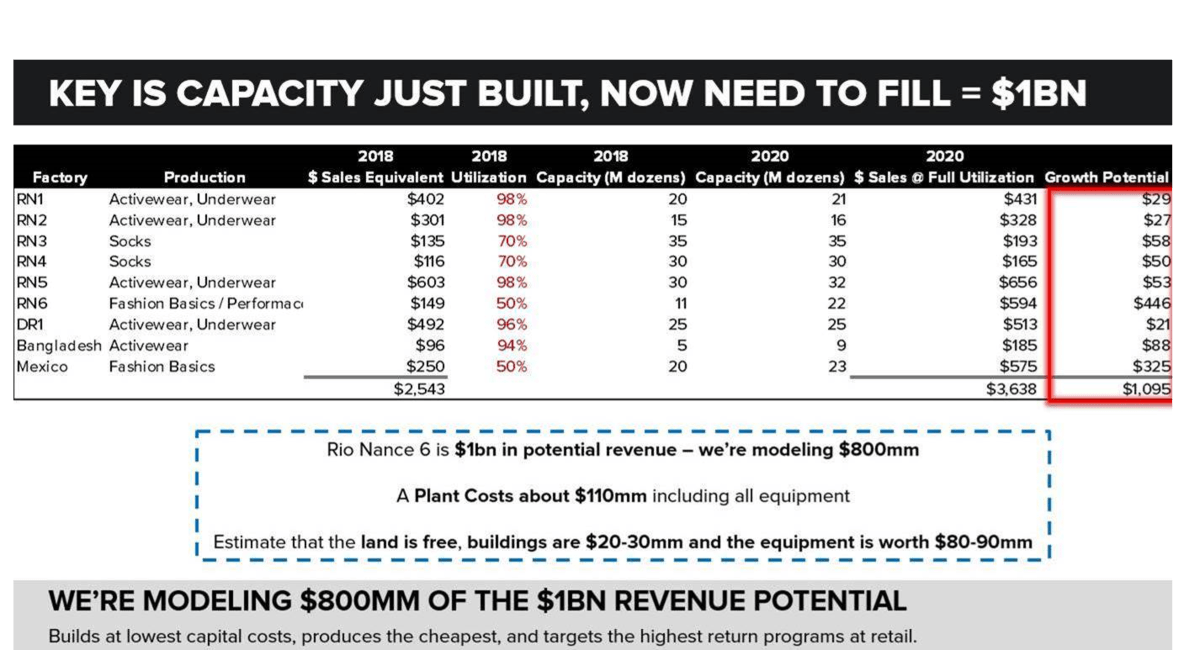

The company is guiding to just MSD% top line growth at a time when it will be clipping these contract wins at a consistent pace – and for some reason the consensus is falling for it. Simply put, this is the mother of all sandbags. We’re modeling $800mm in new business over 2-years for a company that has largely been land-locked in the $2.6-$2.7bn sales range since 2014. GIL should clock in at about $1.87 EPS this year, and then ramp to nearly $3 in two years. At which time we’re likely to see new capacity to perpetuate growth, as this sea-change toward private label (product that can’t be price-shopped on Amazon) is secular and here to stay. As $3 in EPS becomes apparent over the course of 12 months, I think that the growth and return characteristics will warrant a mid-teens multiple. There’s your $45 stock, or a 50% return on an otherwise stable and defendable name that won’t blow you up at $30.

--McGough

Biolsi’s Deep Dive on the Print

Print Quick Take

- Q3 EPS of $.57, representing 6.7% growth, was in line with consensus and $.02 below our estimate.

- Management guided Q4 to $0.42-0.44 bracketing consensus of $.43.

- Revenue growth of 5.3% was less than consensus estimates of 5.8%, but two thirds of the estimates did not reflect the hurricane disruption at the end of Q3. Revenue was slightly higher than our estimate.

- Gross margins contracted 200bps which the company attributed to raw material inflation and hurricane impact.

- SG&A dollars declined 7.1% and leveraged 150bps.

- Through share repurchases 2% net income growth drove 7% EPS growth.

- Inventory increased 3.8%.

Callouts:

Literal headwinds late in the Q were behind the top line deceleration

- Revenue growth was 5.3%, decelerating 150bps sequentially. Revenue was negatively impacted by the Hurricane Florence disruption of $30mm. Gildan has two of its main distribution centers in the Carolinas and outbound shipments were held for several days at the end of Q3. Revenue growth would have otherwise been 9.5%.

- Revenue growth continues to be driven by international, fashion basics, fleece, and global lifestyle brands. Activewear revenue grew 12.1%, decelerating from 17.3% in Q2. The hurricane negatively impacted the growth rate by 280bps. Socks and hosiery revenue declined 16.6%, but adjusting for $15mm of shipments pushed from Q3 revenue would have declined 7.8% compared to the 20%+ declines in Q1 and Q2 due to the Starter sock exit.

- Management said the licensed sock brands business was soft and looks to remain soft in Q4. I would note that one of Gildan’s largest licensed sock brands recently guided to weaker growth in its accessories segment. International grew 28% driven by fashion basics growth.

New Walmart private label underwear program

- Gildan announced a new private label men’s underwear program at its largest customer – in other words, Walmart. Gildan’s branded underwear shelf space will convert to a private label brand and expand by 50%.

- To our knowledge Walmart has never had a private label program in men’s underwear that extended beyond a test. Historically brands have mattered more in underwear than socks. Walmart knows this and in order for private label underwear to work it will have to be seen as a controlled brand rather than a cheap generic replacement.

- This supports our case that Walmart’s latest expansion of private label apparel is different than past initiatives. It is unlikely that Walmart is devoting shelf space to private label underwear to be a cheap, undifferentiated commodity option. Walmart will likely support the new product launch and look to expand it beyond the shelf presentation.

- Gildan said the private label underwear program will begin in Q2. The three previously announced new private label programs will start in Q4. The market has been concerned that the Starter sock exit precipitated a complete exit from Walmart which the new underwear win addresses.

Don’t expect private label margins to be spelled out, but expect them to be high

- Gildan simply can not speak to what the private label margins will be when its customers and competitors are listening. We are comfortable with management’s previous statements that over time private label activewear margins should approach screenprint margins.

- With the consolidation of its divisions into one reporting structure Gildan is not looking to add business that is dilutive to returns. That change in strategy was signaled by the exit from the Starter sock program. CEO Glenn Chamandy said he didn’t think the private label underwear program was bid out. Saying the program was not bid out may be the CEO’s way to answer what the margins of the private label business will be compared to the existing branded business.

- There are a number of factors a retailer uses to evaluate a manufacturer including distribution capabilities, shipment times, days of inventory, existing relationships, capacity, balance sheet, and price. Gildan checks all of the boxes for chain retailers as well as no China tariff exposure.

Capacity growth is not more of the same

- Rio Nance 6 will ultimately be able to support $600mm of additional revenue. Management projects the factory to be fully capable in a year, but equipment will be added as demand warrants over the next couple of years. Gildan is also adding capacity to the existing RN1 and RN5 plants in 2019. This will allow more specialization between the plants and ultimately greater production and efficiencies. It’s important to note that RN6 gives Gildan additional product capabilities that open new revenue opportunities. It also adds to Gildan’s manufacturing flexibility enabling it to pursue smaller volume orders that would have been previously unattractive from a margin perspective.

Gross margin inflection pushed out, and we’re OK with that

- Gross margin contraction of 200bps was the only material negative in the Q3 report compared to our estimates.

- Management attributed the contraction to higher cotton and polyester fiber costs as well the higher costs from production/transportation developments due to Hurricane Florence and disruptions in Nicaragua.

- Gildan has raised prices in the screenprint channel numerous times this year including in September which should have led to pricing catching up to raw material inflation. The $30mm in delayed shipments should not have had an outsized impact on gross margins.

- If RN6 coming online at an underutilized capacity combined with initial start-up costs and inefficiencies were responsible for the margin pressure it would highlight some of the future upside. I am comfortable projecting a timing delay in price increases offsetting higher raw materials which should be seen in Q4. I may be too conservative on future gross margin expansion from a fully utilized RN6.

SG&A leverage is just beginning

- SG&A dollars declined 7% as the savings from the consolidation of the two divisions earlier in the year was no longer offset by investment growth. SG&A leverage was 150bps in Q3. The majority of the savings came from the infrastructure to support the retail sock business.

- As Gildan’s revenues accelerate over the next two years the main driver of margin expansion will be from SG&A leverage. Gildan as a manufacturer does not have to add much SG&A in order to grow sales. Management is guiding to flattish expense dollar growth in 2019 which I project will drive leverage of 100bps.