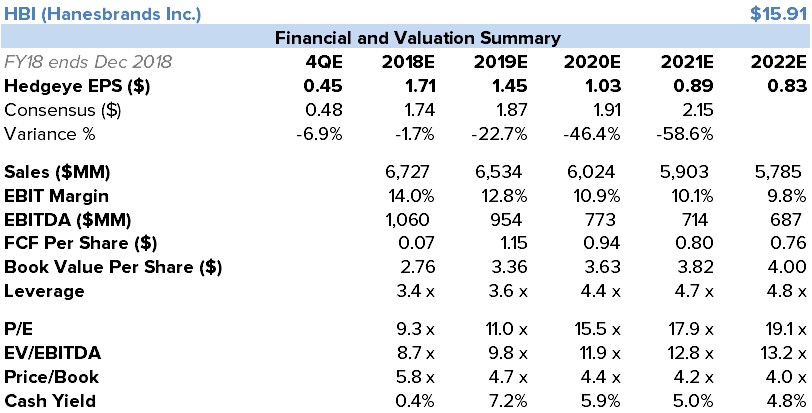

HBI management get less believable with nearly each successive call. It missed top line, covered up an operating miss with special charges and tax, took down full year Cash Flow, and was in denial about the risk of a private label taking share – AT THE SAME TIME Gildan management was on its call talking about business it just won at Wal-Mart. The irony here is that I seriously don’t think that HBI management is lying to us. I think that this team has a weak business planning process, and even weaker internal controls as it relates to understanding, communicating, and subsequently addressing changes in the business environment as they happen. To buy this name today you have to believe that its core innerwear business has the best five quarters since the 2006 spin-off to hit management’s Cash Flow guidance. We’re looking for another series of misses in the US as doors close and the brand simply loses share at the low end to GIL/private label, and at the high end to upstart competition. The sentiment around this name is that the short has mostly played out. But it hasn’t. Even today’s sell-off is still just a taste of what is to come. Check out our model summary below. The Street is building up to $2.15 in EPS over a TAIL duration…we’re at $0.89. If our numbers are right, then this is a $5 stock. Unless 4Q consensus numbers come down well below the guide, HBI just set itself up for more pain over the next 13 weeks.

McLean’s Analysis On The Quarter

Print Quick Take

- Revenue miss (again), that’s 14 of the last 20 Qs.

- Innerwear was worse than we expected, down 7%, Activewear as expected at +7%, International slightly better at +11% (note FX is now a drag vs help).

- Headline in-line, but took a charge for Sears ch.11 (3 cents), tax rate lower than guided (1 cent), so actually more like a 4 cent miss.

- 4Q EPS guided inline, but CFFO for the year was guided down. So cash generation of adjusted earnings is headed lower.

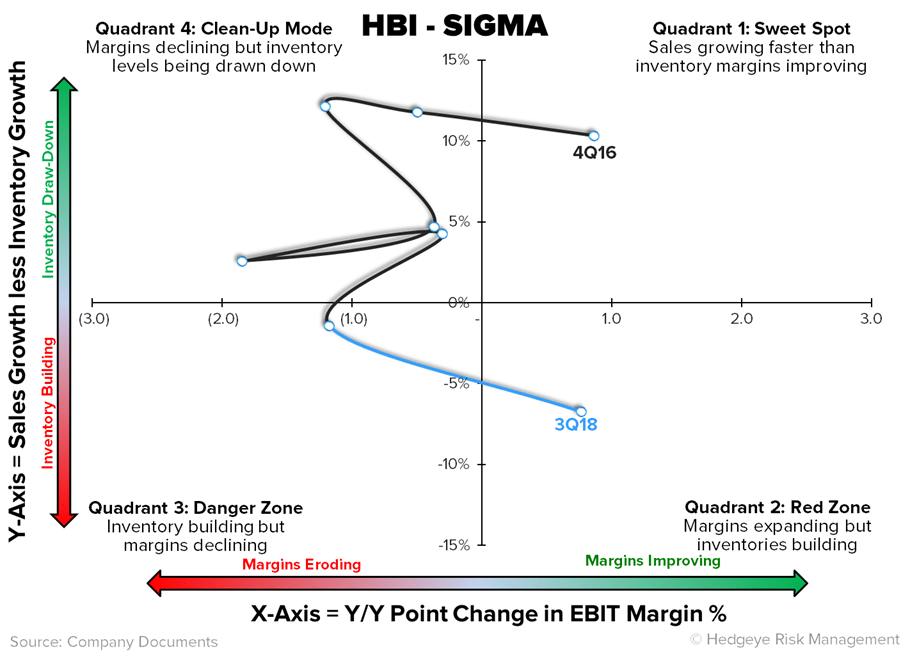

- 3Q margins look ok, at least after 2 different sets of adjustments (non-gaap and Sears) but Inventories are bloating up 9% on 3% sales growth, bearish for 4Q margin outlook.

- The Bullish data point is Champion growth, which management said was 30%, that’s an acceleration from 16% last Q.

- Overall the 4Q bar still looks high too us.

Callouts:

C9 isnt $380mm… its $455mm!

Let’s start with perhaps the most glaring incremental disclosure…

- Last Q, discussing the end of the C9 agreement with TGT, the HBI Press Release stated: “The company generated approximately $380 million in C9 by Champion activewear sales”

- Today in the FAQ filing, in relation to Champion at Mass (C9) HBI noted “The Activewear program is a seasonal commitment business with trailing 12‐month revenue of approximately $385 million at the end of the third‐quarter. The Basics program is a replenishment business with trailing 12‐month revenue of approximately $70 million.”

- So the company left out $70mm from its C9 revenue number last print.

- How do you think this went down?

- I actually doubt management meant to mislead investors. Rather when the last PR was being made, management probably asked the Activewear head what the size of the C9 business was. He said $380mm, since that was his exposure.

- Then shortly after the call in August the Innerwear President probably piped up and said, “Hey you guys know we have C9 underwear booked in Innerwear too, right?.

- HBI processes and information flow could actually be that bad.

Innerwear Decrementals at 33%

We’ve had a handful of people ask us about HBI decremental margin, today’s call perhaps shared some detail, in talking about 4Q guide the HBI CFO said:

- “We removed all sales to Sears Holdings from our forecast, which lowered fourth quarter revenue by $15 million and operating profit by about $5 million.”

- That’s notable and is in-line with our estimates. Lost innerwear sales flow out at ~30% decremental margin, and Champion sales flow in at ~mid teens incremental margin.

- That’s why innerwear margins are down 170bps (excluding deleverage of unallocated dollars since segment disclosure was changed at beginning of the year), Activewear margin flat, International is up 200bps due to Bras N Things mix shift.

Champion Acceleration is actually not bullish.

- Champion apparently actually grew 30%, up from 16% last Q, that had us nervous at first, but it’s not as bullish as you might think.

- The acceleration was actually driven by an inflection of Champion at Mass (C9), from down about HSD to up MSD this Q… but it’s irrelevant since all of this revenue goes to zero in 1.25 years. The acceleration in the rest of Champion was only 100bps to +40%. We think there is real risk that we are seeing the peak in that growth rate.

- The company is making it sound like Champion alone is hot, yet it’s a genre that’s hot, not a brand. Fila, and Russell Athletic are hot too. When the athletic retro trend rolls over, the bulls lose their biggest lever.

“Private label is small” it doesn’t matter…

When asked about the risk from private label, HBI CEO cited the Analyst Day from May. Let’s flashback, when Evans had to answer a question on private label risk online by saying:

- “First of all, the way you ask that question didn't indicate to me that you actually believe the data I just put out there. The brands are very strong online. They're actually stronger online than on bricks-and-mortar. I want you to take that away.”

- So again today management was asked, and it said : “As far as our channels in the Innerwear category, we're not seeing any change in the level of private labeling that business. As we've said for sometime, in Innerwear, the presence of private label is fairly small.”

- Management was probably not aware that this morning Gildan announced a private label program with a major mass customer (Wal-Mart) in underwear. So WMT is launching private label in a category it’s never had it before, which just happens to be Hanes core business. The GIL private label underwear shelf space will be 50% larger than existing GIL brand space and it ships in Q2.

- This is bad for HBI both due to the fact it’s a growing competitor at a low price and high value offering inside WMT, and the fact that it seems to be oblivious that the mass channel is changing right in front of its face.

Flat innerwear… assuming no Sears sales?!?!?!

- HBI is guiding innerwear flat in 4Q. The company noted that this implies 3% growth removing Sears from both years (my math says 2.5% with Sears at $15mm per CFO comments).

- Innerwear hasn’t grown 3% organically since 2Q 2013 (i.e. before HBI went to M&A growth mode with Maidenform). And its facing its toughest comparison of the year by far at +0.8%, with the first 3Qs of the year at -2.8%, -3.4%, and -6.9%. It seems outlandishly aggressive, but who knows, the company has visibility on orders, right?… more on 4Q later.

- Then the company is guiding Innerwear to be flat in 2019 as well. Given the trend over the last 5 years how can it possibly say this with any degree of confidence/integrity?

- It’s continually losing share, more major distribution doors will close (its NOT one time), all of mass is adding private label brands, and a couple dozen small, new, quality underwear brands continue to pick off younger consumers that were Hanes customers.

- I’m just going to say it…. Innerwear will not be flat in 2019, it will be down. Even if Sears has shrunk to only 1-2% of sales LTM.

How does it hit the CFFO numbers?

- The company is guiding to $625mm-$675mm in CFFO after the guide down. Its running $190mm behind the rate of last year at this time, yet needs to do last years number to hit the guide. That means we need to see $500mm in CFFO in 4Q, and about $300mm is probably going to have to come from working capital.

- Inventories are bloated, so perhaps there is a chance, but the 4Q number has to be over $100mm better than any 4Q the company has done.

Management teeing up a big 4Q guide with a lot of confidence…

- We’ve seen this before, and it wasn’t pretty. In 4Q 2016 management promised a big quarter. On the 3Q16 call management said the following re 2016 Cash Flow… "So, very confident, though, that we're going to get to the numbers that we've been talking about."

- It subsequently missed the annual cash flow number by 22%.

- If the company doesn’t hit its targets this time, how can you own this stock with the current leadership?

- In reality, flat innerwear and an implied 3.5% total organic growth rate would just about be a miracle for HBI.

- It’s not impossible though. How it could hit the Q? Jam Innerwear product into the channel clearing a ton of inventory, take a GM% hit, but then take a bigger charge than guided. Sell as much US Champion as millennials can stomach and keeping scaling its distribution in Europe and Japan.

- The 4Q print will be interesting, the last few fourth quarters have been very good for the bears.

- We’re coming in at $0.45, GAAP to be $0.39

Tariffs

Management noted the following on Tariffs in the FAQ:

- “Unlike the vast majority of the apparel industry, our exposure to China is minimal. We do not own any manufacturing operations in China. Of our third‐party sourced units, China represents a very small portion of the units shipped to the U.S. The impact to our costs is immaterial under the current tariffs in place and would likely be immaterial under any of the additional tariff scenarios currently being considered.“

- We’d prefer to see a specific number. About 50% of COGS is sourced from 3rd parties, we think China exposure could be as high as 20% of COGS.