The guest commentary below was written by Benn Steil and Benjamin Della Rocca from the Council on Foreign Relations.

In the Wall Street Journal earlier this month, we examined the change over time in the market reaction to Fed “forward guidance” on future interest rates.

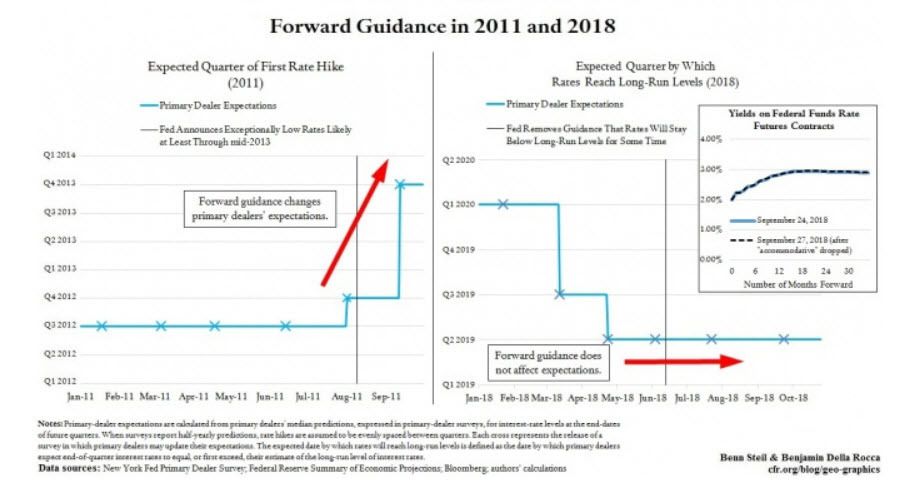

During the crisis, with the Fed’s policy rate at zero, the markets reacted strongly to it. When back in 2011 the Fed pledged not to raise rates at least through mid-2013, primary dealers of Treasury bonds immediately pushed back their expectations for rate hikes—as shown in the left-hand figure above. Today, however, with the Fed’s policy rate well above zero, at 2-2.25 percent, only the press seems to care about the Fed’s message changes.

In June of this year, the Fed’s post-meeting statement dropped language pledging continued low rates. Yet primary dealers, having concluded that the pledge was no longer meaningful, didn’t change expectations a jot—as shown in the right-hand figure. Similarly, when the Fed dropped its description of current interest-rate levels as “accommodative” in September, federal funds rate futures prices (a surrogate for dealer expectations, which haven’t since been surveyed) didn’t budge—as shown in the small inset figure.

Fed Chairman Jay Powell is therefore right in wishing to scale back forward guidance, which has outlived the usefulness it had when short rates were stuck at zero and the Fed needed words to keep down long rates. Today, with the Fed back in control of short rates it has no reason to tie its hands in the future.

We would like to see the Fed go further, however.

To the extent that forward guidance can still move markets, it’s counterproductive. FOMC members publicizing their views on when and by how much rates should move encourages them to ignore data inconsistent with their views, as humans naturally wish to validate their omniscience. As Minneapolis Fed president Neel Kashkari said back in March, he would have raised rates if he “had been sitting in the chairman’s seat” not because it was appropriate but because “we told the markets we were going to raise rates.”

That’s a mighty bad reason to raise rates, and a mighty good one to stop predicting them.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor piece written by Benn Steil and reposted from the Council on Foreign Relations’ Geo-Graphics blog. Mr Steil is director of international economics at the Council on Foreign Relations and author of The Battle of Bretton Woods and The Marshall Plan: Dawn of the Cold War. It does not necessarily reflect the opinion of Hedgeye.