Into the market strength yesterday we bought the VXX and shorted the SPY. With the VIX down -38% since the S&P500 bottomed -10.2% lower on Feb 8th, yesterday was a good time to buy some volatility for the immediate term TRADE from its oversold level.

Volatility (VIX) declined 4.4% yesterday, while the VIX continues to be broken on TRADE, TREND and TAIL. The Hedgeye Risk Management models have levels for the volatility Index (VIX) at: buy Trade (16.90) and sell Trade (18.64).

There was no obvious catalyst behind yesterday’s 0.58% move in the S&P 500, though there is a clear pick up in the RISK appetite and the REFLATION trade is gaining momentum. The pullback in the dollar provided support for most commodities and commodity equities. The Hedgeye Risk Management models have levels for the Dollar Index (DXY) at: buy Trade (79.52) and sell Trade (80.31).

Riding the REFLATION trade were Materials (XLB) and Energy (XLE), and were two of the three best performing sectors yesterday. Financials (XLF) rounded out the top three spots, with the focus on diminishing regulatory headwinds and capital needs. Within the XLF, life insurance stocks were among the best performers.

Within the XLE, coal names led the index higher, with the focus on M&A after MEE announced that it would acquire Cumberland Resources Corp for $960M. The oil services group was another bright spot, with the OSX +0.8%.

Technology was a strong outperformer last week, but the XLK is unable to sustain the momentum this week. The semis put in a strong showing with the SOX +1.2% yesterday, underpinned by strong fundamentals. Industrials were also a relative underperformer, though the machinery space fared well after lagging earlier in the week.

Yesterday, the Consumer Staples (XLP) and Consumer Discretionary (XLY) sectors finished higher, but were relative underperformers. Retail also underperformed, although the S&P retail index finished higher for a sixth straight day. Restaurant stocks continue to outperform on the back of some positive commentary in the QSR space - JACK +5.1%. BKC +3.1% were two notable standouts in the space.

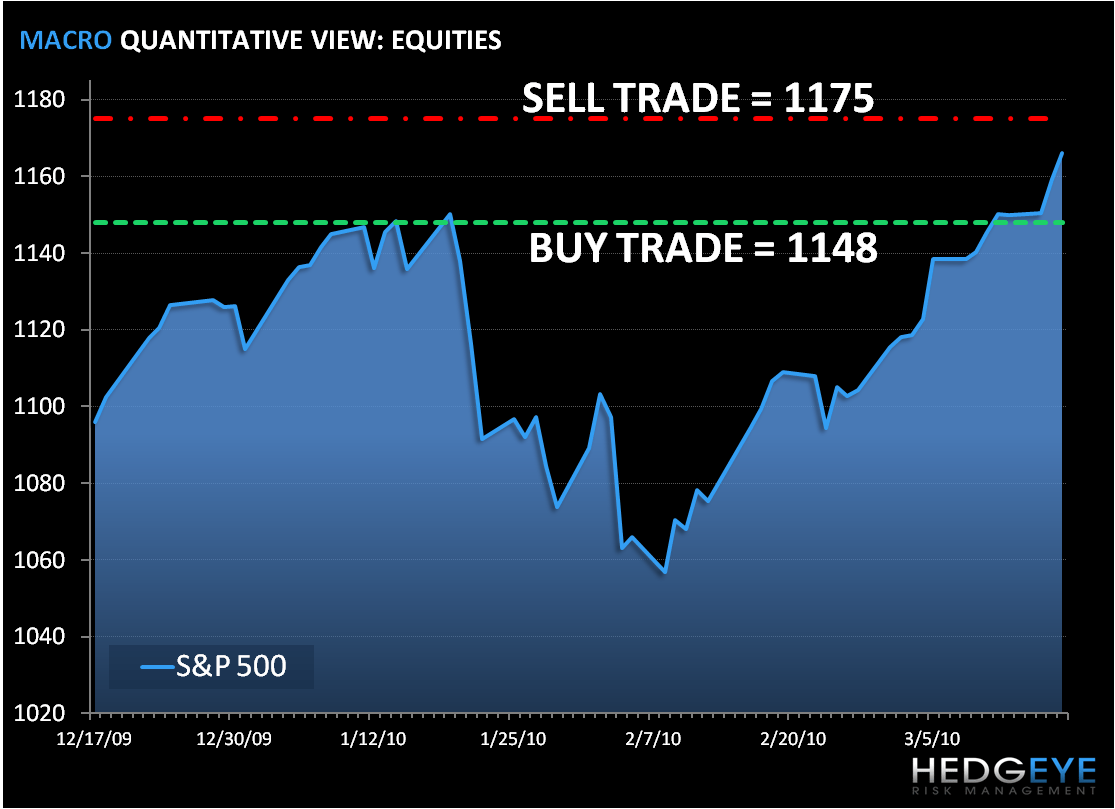

As we wake up today, equity futures are trading below fair value ahead of Feb CPI and as Greece pushes back into the spotlight as Germany is breaking ranks with the rest of the EU. As we look at today’s set up the range for the S&P 500 is 27 points or 1.6% (1,148) downside and 0.8% (1,175) upside.

Today's MACRO highlight will be:

- US CPI Core Index (February)

- US Continuing Claims (6-March)

- US CPI MoM (February) consensus 0.1%; ex-food/energy 0.1%

- US CPI YoY (February) consensus 2.3%; ex-food/energy 1.4%

- US Initial Jobless Claims (13-March) consensus 450K

- US Current Account Balance (Q4) consensus ($119.8B)

- Philadelphia Fed (Mar) consensus 17.6

- US Leading Indicators (Feb) consensus 0.1%

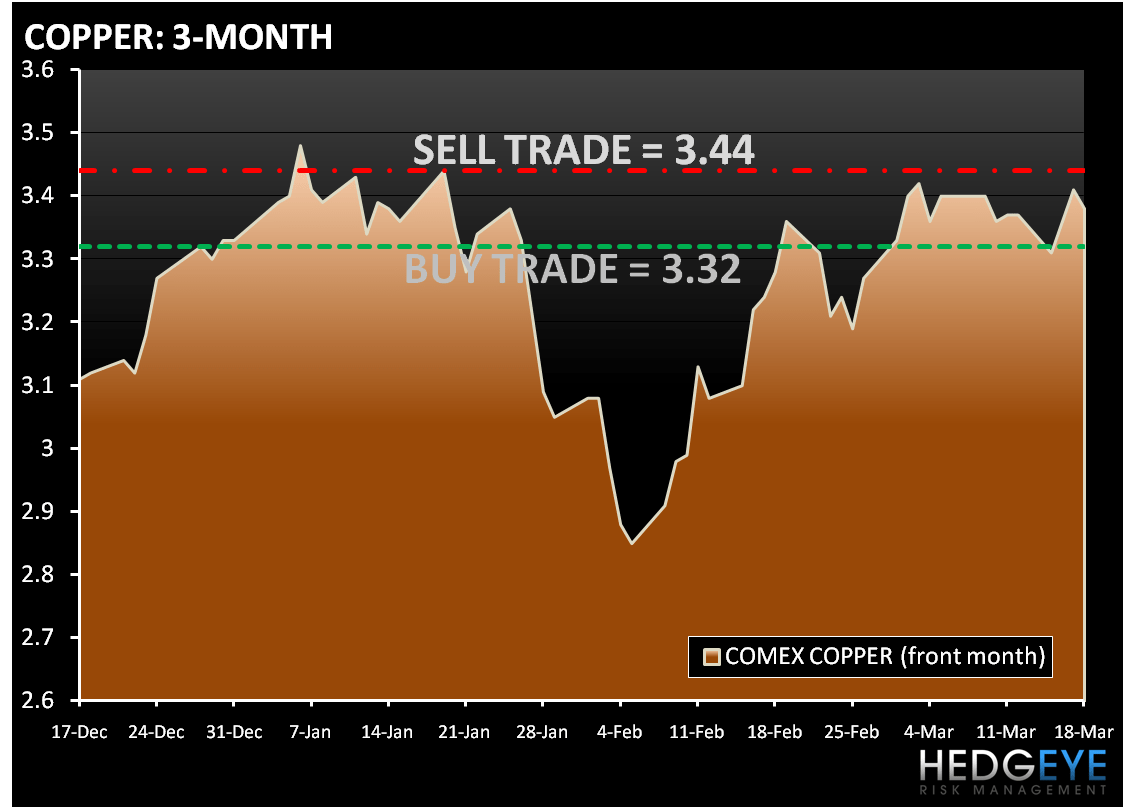

In early trading, copper is trading lower as the dollar strengthened on concern that Greece will fail to secure financial assistance from the European Union. The Hedgeye Risk Management Quant models have the following levels for COPPER – Buy Trade (3.32) and Sell Trade (3.44).

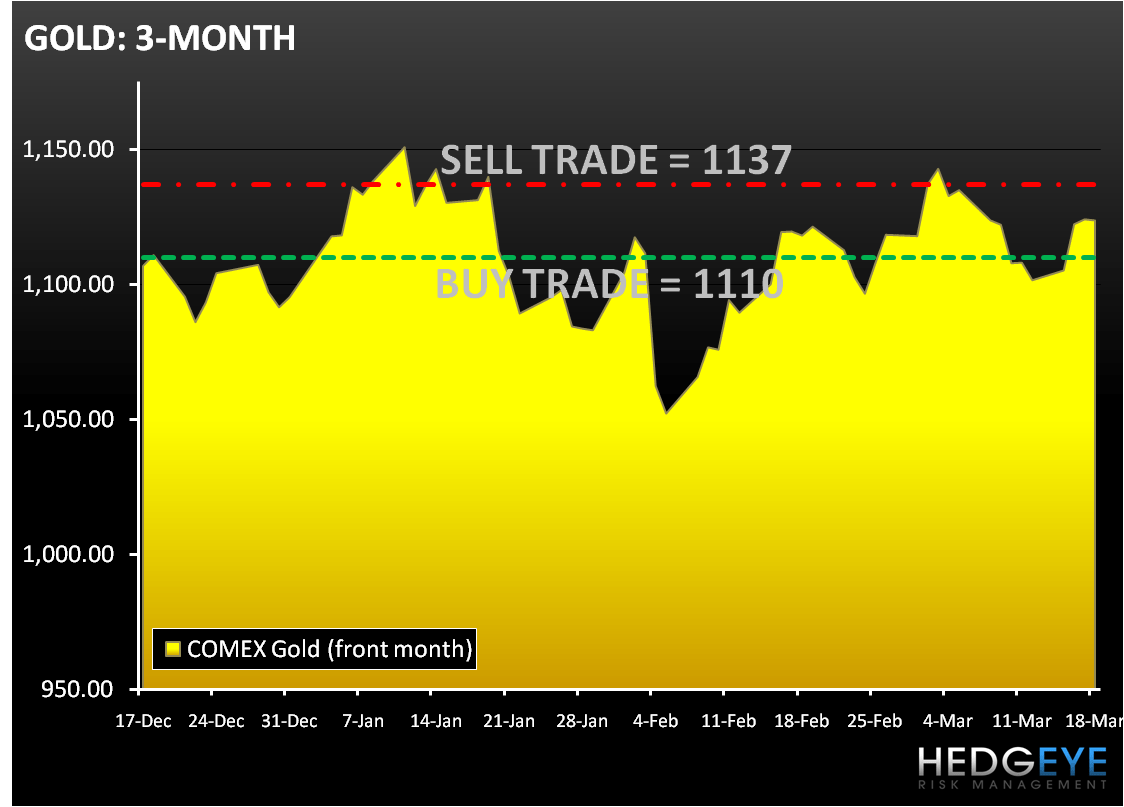

In early trading Gold is trading sideways. The Hedgeye Risk Management models have the following levels for GOLD – Buy Trade (1,110) and Sell Trade (1,137).

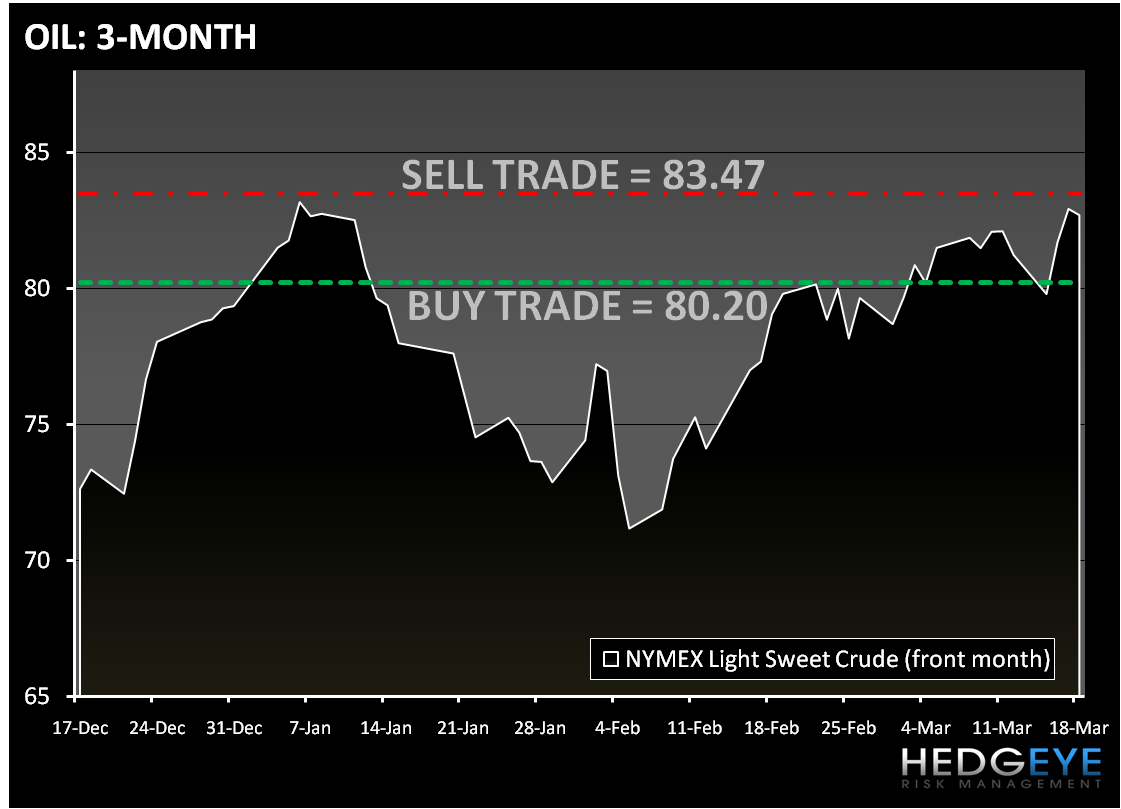

Oil is trading slightly lower on the back of a stronger dollar. The Hedgeye Risk Management models have the following levels for OIL – Buy Trade (80.20) and Sell Trade (83.47).

Howard Penney

Managing Director