Finally, a year after issuing an executive order calling for increased use of Health Reimbursement Accounts, the Trump Administration issued rules governing their expanded use by employers and re-ignited the long-fought debate on exactly what role employers should have in providing health insurance.

Under the Obama administration, use of HRAs for the purchase of health insurance was prohibited for fear that employers would dump their sickest employees on the health insurance exchanges. There were philosophical reasons as well. Many authors of the ACA, like Henry Waxman, felt employers (or their unions) had an almost moral duty to provide health insurance to workers, hence the decision to include in the law an employer mandate on top of an individual mandate.

The Obama policy direction was somewhat at odds with the basic structure of the ACA which was designed to encourage purchase of individual health insurance policies in a free market. It is also at odds with the widely held view by virtually every American health economist that employer-based insurance depresses cash wages and drives up costs.

The Trump administration has proposed reversing Obama policy and greatly expanding the circumstances under which an employer can use HRAs. The proposal:

- Removed prohibition against integrating HRAs with individual health insurance coverage

- Expands the definition of “limited excepted benefits” like long-term care to include $1,800 to provide certain supplemental benefits or pay other medical costs

In what would amount to a shift from offering defined benefit arrangement to a defined contribution plan, employers will be permitted to fund an HRA to cover medical expenses for employees enrolled in the individual market, on or off exchange. Depending on which type of HRA/health plan integration the employer uses, medical expenses covered by the HRA can include copayments, deductibles, co-insurance, premiums as well as medical care not covered by the health plan.

The Trump Administration has the same concern as the Obama administration regarding adverse selection but found a solution to the problem. Employers who offer HRAs integrated with the individual health plan market will be prohibited from also offering traditional health plans to the same class of employees (i.e., all part-time or all full-time)

Employees that opt for the HRA integrated with an individual plan would not be eligible for a Premium Tax Credits. If the employee would otherwise qualify for Premium Tax Credits by purchasing insurance on a Federal or State-based exchange, they can opt out of the HRA integrated plan.

The really big news is that an employer offering an HRA integrated with an individual plan would meet the requirements of the employer mandate.

Impacts. The Treasury Department estimates that there will be about 1 million people enrolled in HRA integrated health plans in 2020, the first year the arrangement will be available, and growing to 11 million people by 2029. They further estimate that the number of individuals in traditional group health insurance will fall by 600,000 in 2020 and 6.8 million in 2029.

The proposal gives employers, squeezed by increased health care cost under ASO contracts and a tight labor market, another option. How much uptake will occur will depend on plan costs. Exchange premiums have moderated this year but are still high relative to non-QHP plans. Private exchanges like that used by SBUX has not seen the uptake that many benefits experts expected.

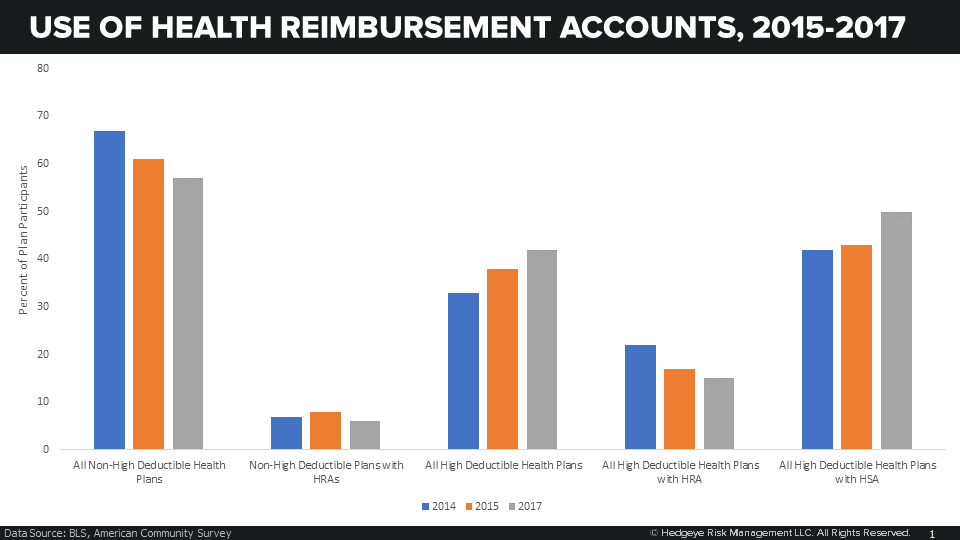

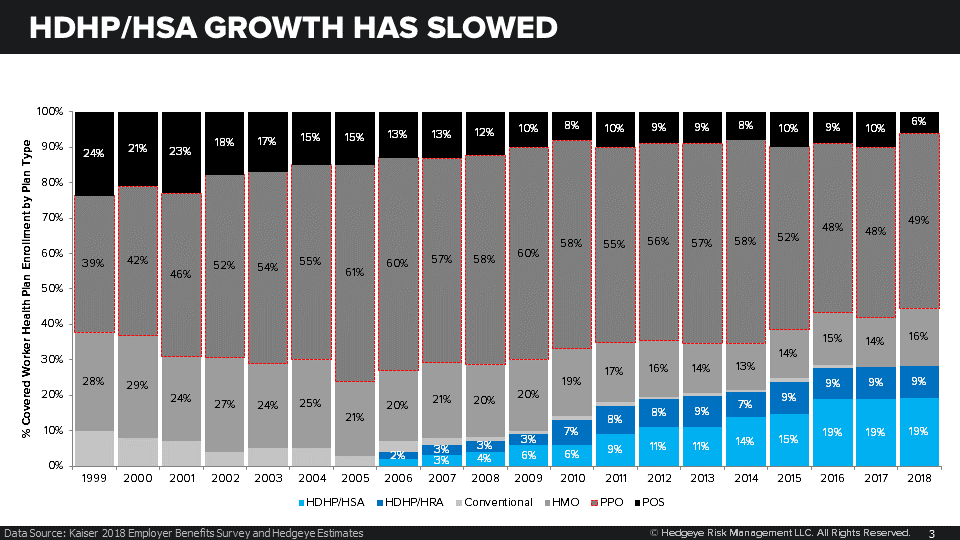

The implications for HQY are marginally negative. Growth in high deductible health plans has slowed as employers resist offering it as the only option to their employees. The HRA integrated option, like the administrations other insurance alternatives of Short-term Limited Duration plans and Association Health Plans, is designed to create more affordable options beyond the usual formula of increasing deductibles.

In the absence of price moderation in health care, high deductible plans are not an affordable option and, as such, are not politically attractive to Trump and even some Congressional Republicans. While there remains some possibility that Congress will expand HSAs in a lame duck session, that prospect diminishes dramatically if Democrats take control of the House in January. HSAs are generally bipartisan but not when Democrats need to keep their restless left flank happy. A more radicalized Democratic Party will view HSAs (and HRAs, STLDI, AHPs) as undermining employer's obligations to provide health insurance.

Emily Evans

Managing Director – Health Policy

Health Policy

Twitter

LinkedIn