Financial markets are selling off—just like our Macro analyst team predicted.

Why is this happening? More importantly, what comes next?

Hedgeye CEO Keith McCullough has answers. He delivered a detailed market and economic outlook as part of our Hedgeye Investing Summit. We don’t want you to miss any of the key investing takeaways.

Below is an important excerpt from McCullough’s presentation explaining why investors should “Beware This Late Cycle U.S. Economy." (CLICK HERE to watch the entire webcast, in which McCullough explains where investors should hide out ahead of the “Quad 4 Hurricane.”)

* * * *

Keith McCullough: What I care about most is growth and inflation. The rates of change in growth and inflation are the two biggest and most important questions to solve for in Macro.

This isn’t subject to debate. [Bridgewater founder] Ray Dalio has built a wonderful firm with a lot of smart people who have back-tested this.

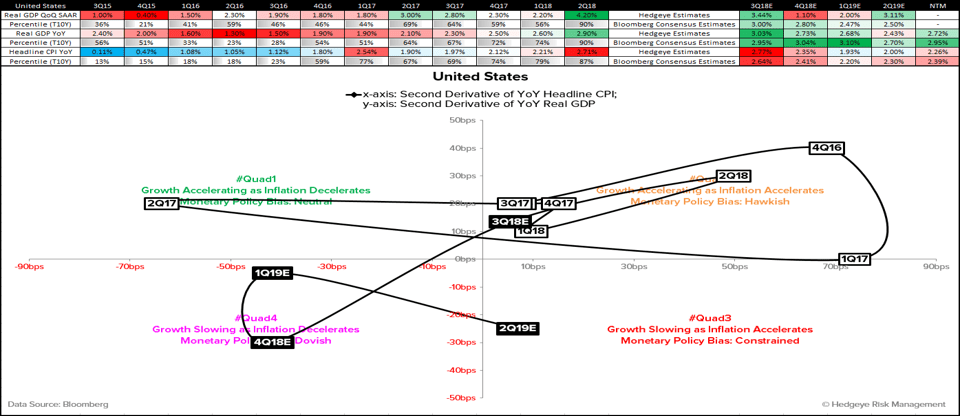

Here’s our model. When you have growth and inflation accelerating at the same time, as it has been for the U.S. economy over the last 5 quarters, we call that Quad 2. That’s not subject to debate either. That is a fact.

We think the U.S. economy is heading into Quad 4, in which growth and inflation slows, in Q4. That is indeed a forecast, based on our model.

Once you have growth and inflation slowing, central banks realize it and have to turn dovish. They devalue the currency and what you get is price inflation, specifically asset inflation in markets, but you don’t get economic expansion. In other words, you get stagflation. That’s Quad 3.

McCullough: So again, we’ve had 9 consecutive quarters of growth accelerating, meaning the U.S. economy has been in either Quad 1 or Quad 2. That’s a historic run.

But what I’m trying to do as a risk manager is get you prepared for what the most amount of people aren’t positioned for tomorrow. We also want to get the timing right on that.

The reality is that what the data says is a lot more important than what any human says. We look at the quarterly returns for asset classes, factor exposures, sector returns across all four quadrants in our model.

My process is pretty simple with a lot of complexity around it. We’re trying to figure out what Quadrant we’re going to, so you have a playbook at the sector level, asset class level and at the style factor level.

It’s very consistent. It’s apolitical. And it’s data dependent.

You’ll note in our four quadrant playbook, Quad 4 is the opposite, mirror reflection of Quad 2. If you follow us, you know that our call over the past few quarters has been Quad 2. That’s why I’ve been bullish on U.S. growth and bearish on long-term Treasury bonds because that’s what Quad 2 tells you to do.

We were bullish on High Beta, Momentum, Technology stocks and Consumer Discretionary.

Now, I want to short all that. Because that’s what you do in Quad 4. You get long dollars. You get long duration, i.e. long-term bonds. You get long Utilities and Consumer Staples. You can see the factor exposures. You’re looking for minimum volatility and high-quality.

In the last three weeks, if you put that playbook on you absolutely crushed it.

To get the forward-looking Quad outlook for growth and inflation right, what we do is we run predictive tracking algorithms for both that are highly accurate. More accurate than what’s published on the Old Wall that’s for sure. We really compete with people on the buyside. We meet with fund managers who have their own forecasts. [DoubleLine Capital CEO] Jeff Gundlach has his own forecast for inflation that is contra to mine, and I’ll explain why in a second. I have my own model.

Getting back to where I think we’re going.

We have GDP slowing, after growth for nine straight quarters, from year-over-year growth of 1.3% in the middle of the year back in 2016, to 3% at the peak of the cycle here in 3Q 2018. From there, we see the U.S. economy slowing after 3Q 2019, starting with 30 basis points off the peak to 2.7% as we head into 4Q 2018.

Now, you might say 30 basis points isn’t a lot. I don’t particularly care what you say on that. It matters. And if you look at how Wall Street will read it, which is the quarter-over-quarter sequential reading, in Q4 of 2018, our 30 basis point deceleration on a year-over-year basis equates to a GDP reading of 1.1%.

We were the firm that prior to this said the U.S. economy would go north of 3%. In other words, we go both ways on the data. And when the data on the U.S. economy is going to rollover into steepening base effects, we make that call too.

Here’s the key takeaway: GDP of 4.1%? That’s yesterday’s news. The fourth quarter will have a 1 in front of it if we’re right on growth.

McCullough: Okay, that’s growth. Let’s turn to inflation.

This is where I deviate from Mr. Gundlach. I have a view that inflation has peaked. Look at the recent PPI data. That was a third consecutive month of slowdown already. That’s not an opinion. That’s a fact, inasmuch as the most recent CPI data slowed again to 2.3%. The peak was 2.9% in July.

What you can see in this chart (see below) is that by the time we get to July of next year, inflation could be really slow. I’m just calling for the first 100 basis points of a slowdown in inflation to 1.82%.

That’s what our predictive tracking algorithm says relative to Wall Street, which is basically sticking with its current outlook. What Wall Street does it take what happened yesterday and pin that out into the future.

If you’ve ever used Wall Street research on growth and inflation, I apologize. Hedgeye was started a decade ago. We’re a relatively new firm. We started it by calling the 2008 financial crisis and the bottom in 2009. There have been plenty of other calls that we’ve made. Why? The process has stayed the same.

CLICK HERE to watch the entire video replay.