The S&P 500 turned an exceptionally strong performance on Tuesday, finishing around its best level for the day. Volume was up 9% day-over-day and breadth expanded significantly. As the market is getting stronger there is seemingly a pickup in the appetite for increased risk. The dollar index has now fallen 4 of the last 5 days and was down 0.62% yesterday. The Hedgeye Risk Management models have levels for the Dollar Index (DXY) at: buy Trade (79.68) and sell Trade (80.86).

Yesterday’s FOMC meeting was anticlimactic. The central bank reiterated that economic conditions are likely to warrant exceptionally low levels of the federal funds rate for an extended period. See Keith’s post from yesterday “FOMC Pandering: Trader Vik like it” for our position on this subject.

Again the MACRO data points provide some headwind, but are being brushed under the rug. Yesterday, housing starts in the US fell 5.9% month-to-month in February, but the decline was due mostly to weather related issues. Although the news from the Euro zone is slightly more positive as the finance ministers said that they are ready to help Greece with an emergency support facility, if needed. There also seems to be very little concern about the potential for an “angry client” - see yesterday’s Early Look for more details.

Last night China rose for the second day in a row, rising 1.93% - the second biggest day of 2010! The Chinese crash callers are everywhere, as we believe that the widely expected additional tightening measures are already priced into the market. We are long China through the CAF.

On the back of a weaker dollar and a better performing Chinese market the two best performing sectors yesterday were Materials (XLB) and Industrials (XLI). The Fertilizer names were underpinned by upbeat inventory data, while NEM, WY and X all outperformed. CF industries was the only stock to decline in the XLB yesterday.

While consumer stocks lagged the broader market today, LBO speculation runs rampant and is reminiscent of 2007. Yesterday speculation was that HOG would go private; the stock traded up 7% on big volume.

Volatility declined 1.72% yesterday, while the VIX continues to be broken on TRADE, TREND and TAIL. The Hedgeye Risk Management models have levels for the volatility Index (VIX) at: buy Trade (17.16) and sell Trade (18.79).

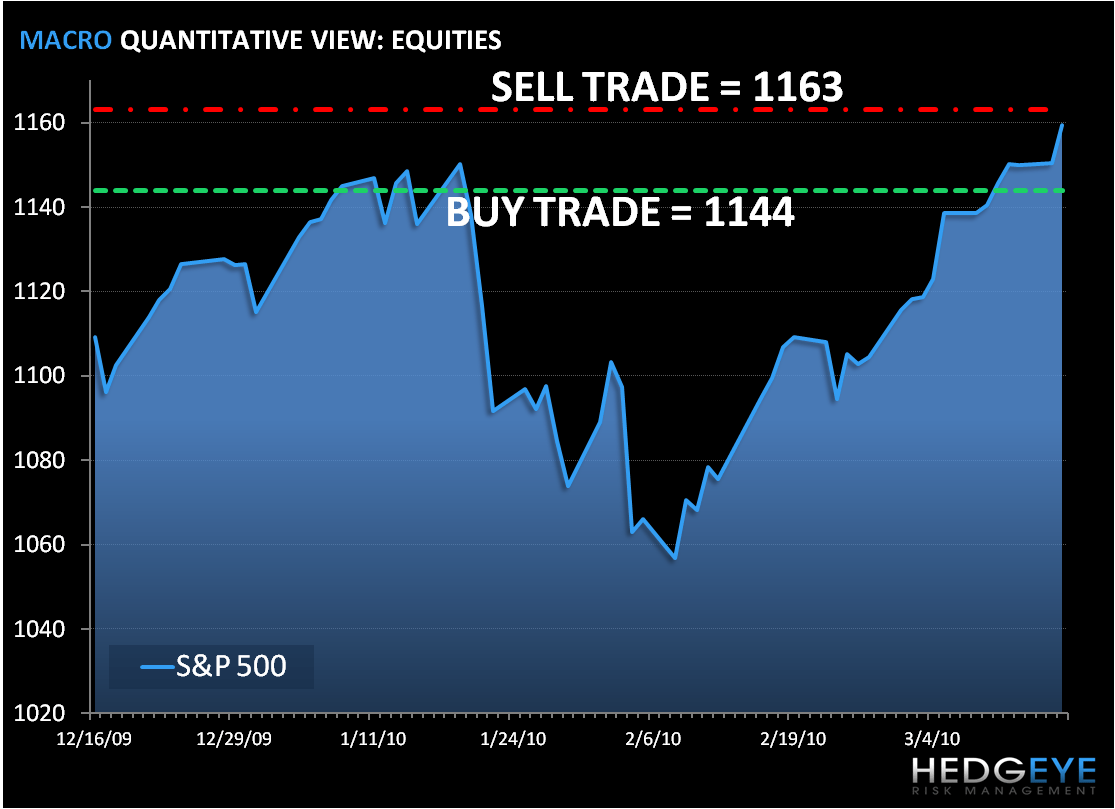

As we wake up today, Equity futures are trading above fair value in a continuation of yesterday's upward momentum and firmer global markets. As we look at today’s set up the range for the S&P 500 is 19 points or 0.6% (1,144) downside and 1.1% (1,163) upside.

Today's MACRO highlights will be:

- MBA Mortgage Applications came in at -1.9% (it was the weather of course)

- Feb PPI (up 4.9% YoY)

- DOE Crude Oil, Natural Gas Inventories

In early trading, copper is trading higher as the dollar is trading lower. The Hedgeye Risk Management Quant models have the following levels for COPPER – Buy Trade (3.24) and Sell Trade (3.43).

In early trading Gold is also benefiting from a lower dollar. The Hedgeye Risk Management models have the following levels for GOLD – Buy Trade (1,108) and Sell Trade (1,140).

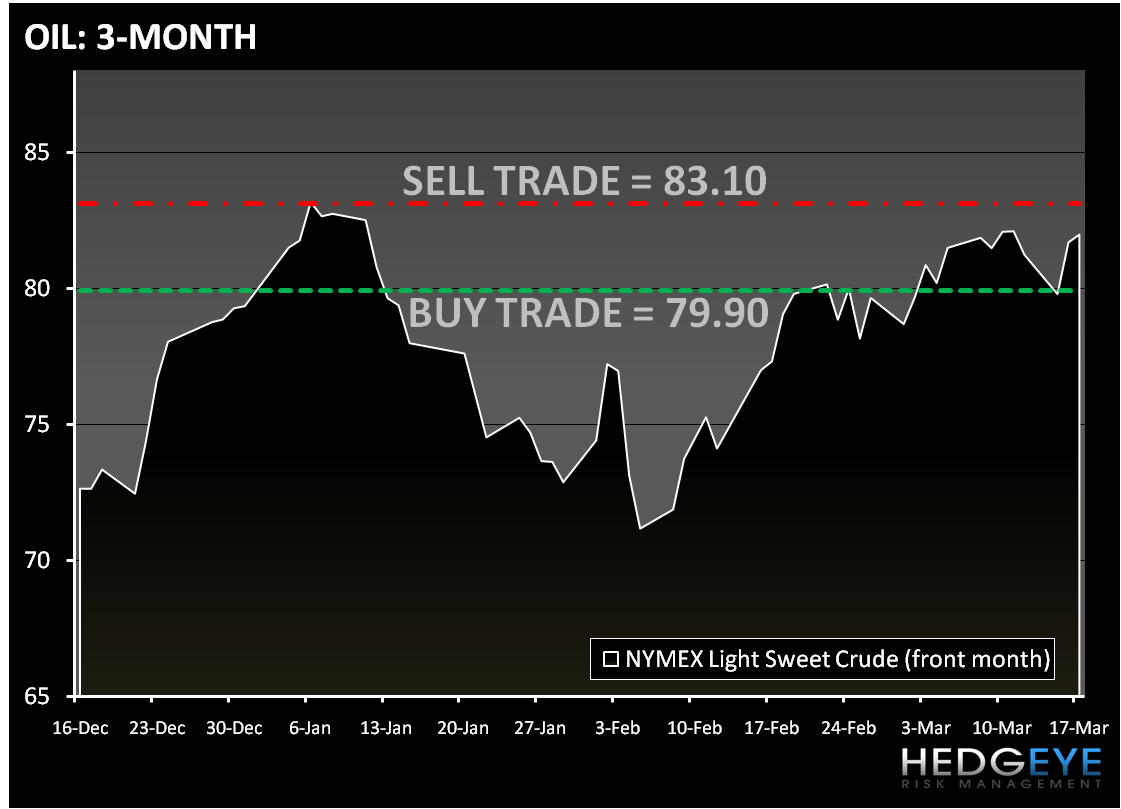

OPEC agreed for the fifth time since 2008 to keep its production limits unchanged, even as some members voiced concern that supply may be too high. The Hedgeye Risk Management models have the following levels for OIL – Buy Trade (79.90) and Sell Trade (83.10).

Howard Penney

Managing Director