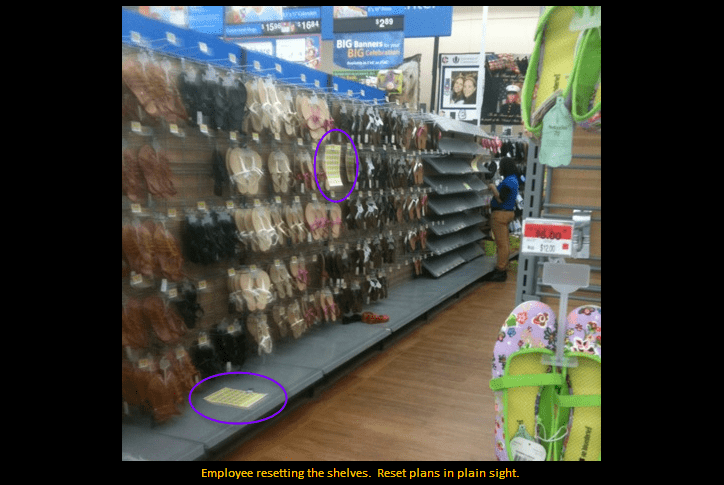

We’re starting to see broader evidence of Wal-Mart shift its focus away from footwear, which is positive for PSS on the margin. Back in July ’09 we highlighted the emergence of this theme, though evidence has been slow to come. In our ongoing analysis of Wal-Mart and its impact on everything else retail, we’ve been noticing enough tweaks to the assortment recently such that we thought it was time to break out the digital camera. Yes, the pictures below are from only one store, and there can be an endless number of variables impacting that specific store at that specific time on that specific day. But the step up we’ve seen in activity at Wal-Mart to change up its shoe department has been enough such that we think the pictures below tell a directionally accurate story.

When we look at quantifying the impact… Wal*Mart did $305bn in the US last year. About 11% of that was apparel, footwear, and accessories. Only about 100bps-200bps was driven by footwear, which suggests about $5bn annually.

The table below shows the store overlap between Wal-Mart and Payless. A quarter of Payless stores have a Wal*Mart within a mile radius. 43% have a WMT within 5 miles.

Let’s say Wal*Mart scales down footwear to 1% of sales over 3 years as it cycles through its remodel process. That suggests over $2bn is up for grabs. If I take it a step further and assume that 38% is within reach (within a 3-mile radius), then that’s $760mm. If PSS grabs only 10% of that, it would be a 2% comp alone. At a 30% incremental margin, we’re talking $0.23 per share. That’s off a base of $1.28 last year.