On the surface the S&P 500 looked like it had a good day, finishing mixed on Monday after spending the bulk of the day in negative territory. The internals of the market were decidedly negative with volume down 11.6% day-over-day and the advance-decline line turning negative at -506, down 788 on the day.

The news flow from global MACRO was a headwind yesterday, especially the news from China and Greece. There were also some concerns surrounding comments from Moody's that both the US and UK have moved "substantially" closer to losing their AAA credit ratings, though note that CDS on US and UK government bonds were little changed. As we have said many times, the ratings agencies are a lagging indicator.

On the MACRO calendar in the US, industrial production rose a better-than-expected 0.1% in February, with a positive take away from the ability of production to increase last month despite the weather. On the negative side, the only real disappointment seemed to be the NAHB Housing Market Index, which fell to 15 in March from 17 in February.

Yesterday, the SAFETY trade outperformed, while pockets of the market with outsized leverage to the RECOVERY trade underperformed today. Notable decliners included Energy (XLE), Consumer Discretionary (XLY), Materials (XLB) and Industrials (XLI) was flat on the day.

The bounce in the dollar was the big headwind too, with the move largely fueled by heightened tightening concerns surrounding China; the Dollar index was up 0.52%. The Hedgeye Risk Management models have levels for the Dollar Index (DXY) at: buy Trade (79.83) and sell Trade (80.79).

Yesterday, there was a lot of noise surrounding the regulatory uncertainty in the financial services and healthcare sectors. Facilities names and Pharma posted modest gains today; managed care was a laggard with the HMO +0.2%, though the group did finish in positive territory. There were several reports noting that Democrats currently lack the votes to pass the Senate's healthcare reform bill in the House.

Within Financials (XLF), the banking group was a slight outperformer yesterday with the BKX up 0.2%; however, investment banks along with money-center names were among the laggards yesterday. The underperformance was attributed to the inclusion of the Volcker Rule in Senator Dodd's financial market reform bill released today.

After lagging the broader market over the last few weeks, the consumer staples sector was the best performer yesterday. In the Hedgeye sector models yesterday, outperformance over the immediate term put the XLP in an overbought position, so we shorted it. Yesterday, WMT was one of the standouts on the back of an upgrade at Citi.

One of the bigger tailwinds for the market seemed to be the continued pickup in M&A activity, with some high-profile deals yesterday in the apparel and E&P spaces.

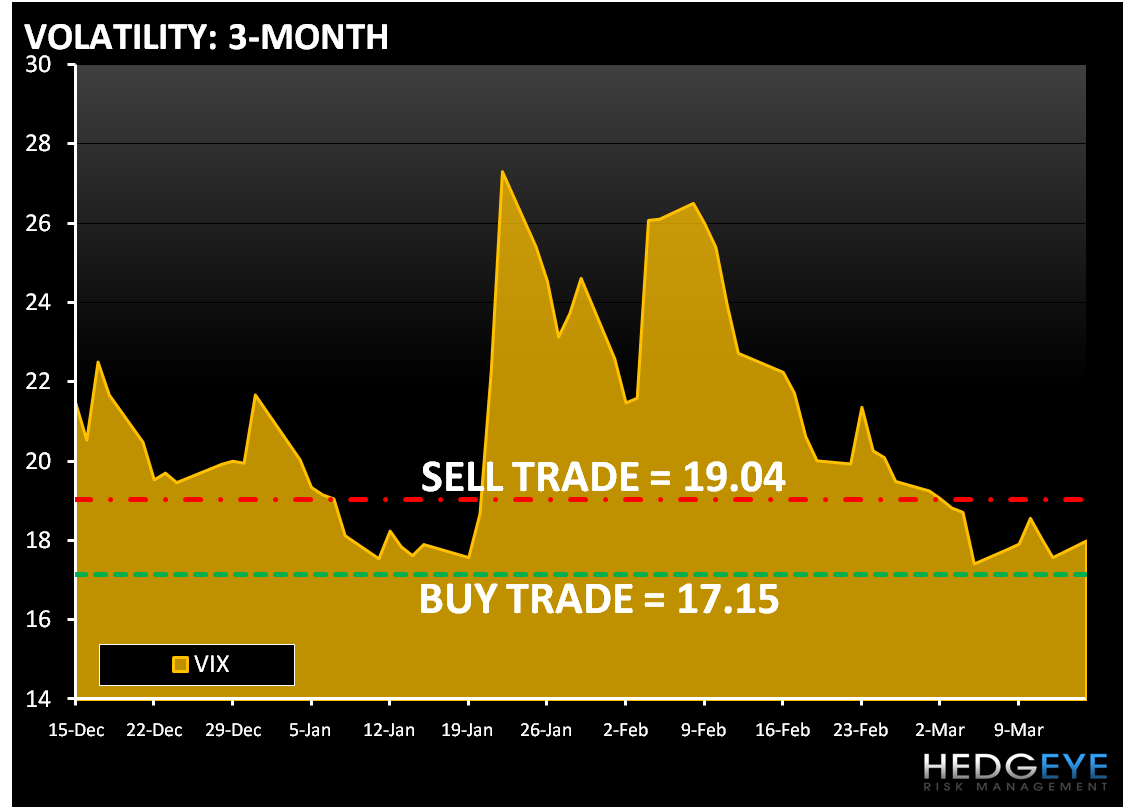

Volatility improved 2.39% on Friday, while the VIX continues to be broken on TRADE, TREND and TAIL. The Hedgeye Risk Management models have levels for the volatility Index (VIX) at: buy Trade (17.15) and sell Trade (19.04).

As we wake up today, equity futures are trading mixed to fair value ahead of today's FOMC rate decision and in the wake of yesterday's performance which saw markets eventually close flat having spent most of the day in the red. The focus of the FOMC meeting will be on any hints as to when the Fed might choose to lift rates. As we look at today’s set up, the range for the S&P 500 is 22 points or 0.9% (1,139) downside and 1% (1,161) upside.

Today's MACRO highlights will be:

- US Import Price Index

- US Housing Starts (February) consensus 570K

- US Building Permits (February) consensus 601K

- ABC Consumer Confidence

In early trading, copper is trading higher as the dollar is trading lower. The Hedgeye Risk Management Quant models have the following levels for COPPER – Buy Trade (3.24) and Sell Trade (3.45).

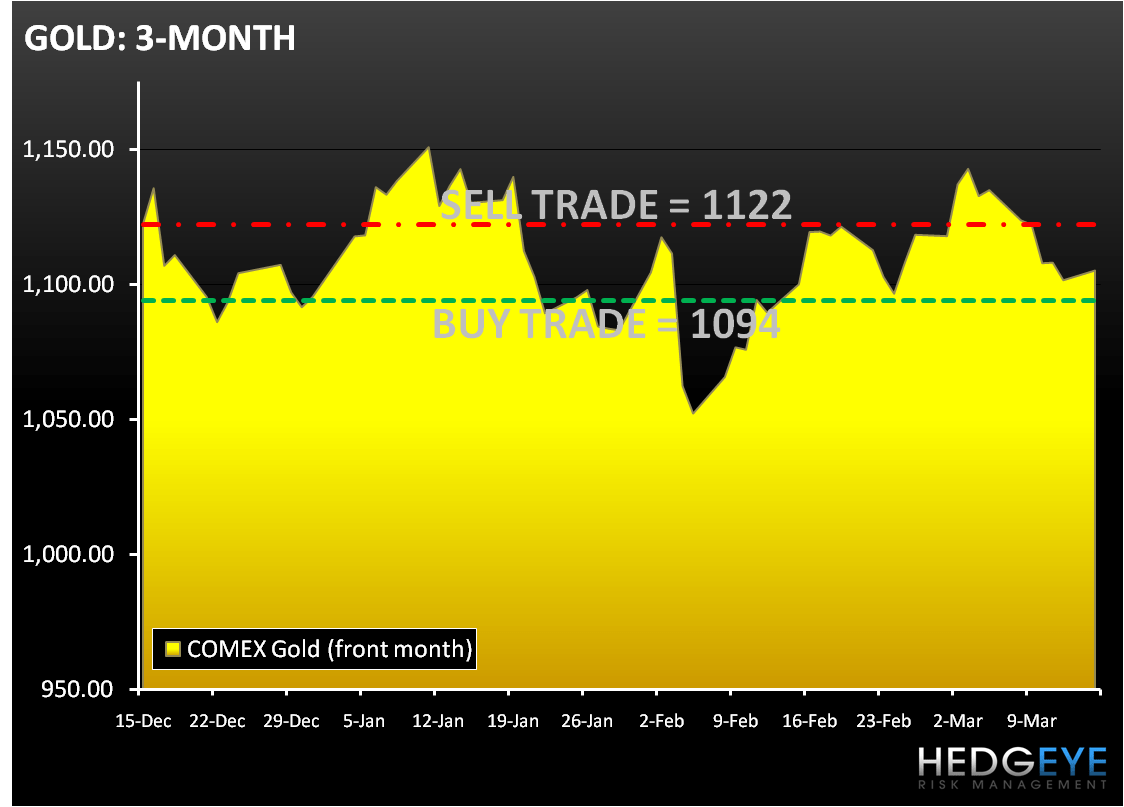

According to Bloomberg, gold rose for a second day in London as “investors sought a haven before the U.S. Federal Reserve’s interest rate decision and amid speculation about financial aid to Greece.” The Hedgeye Risk Management models have the following levels for GOLD – Buy Trade (1,094) and Sell Trade (1,122).

Also on Bloomberg today - “Saudi Arabia, the biggest and most influential member of the Organization of Petroleum Exporting Countries, said oil prices are in the right range and there’s no need to change production policy.” Crude oil is trading slightly higher in early trading. The Hedgeye Risk Management models have the following levels for OIL – Buy Trade (78.41) and Sell Trade (82.99).

Howard Penney

Managing Director