The S&P 500 finished higher on another day of very light trading. While the index was up 0.4% on the day, volume declined 14% day-over-day and breadth of the market deteriorated significantly. The S&P 500 finished at its highest level since October 2008.

On the MACRO calendar the only meaningful statistic was initial jobless claims and the data was mixed. While claims dropped 6,000 week over week to 462,000 from 468,000, the 4-week rolling average figure actually rose by 5,000 to 475,000 from 470,000. Yesterday’s number was a clear disappointment, but there is real optimism that jobless numbers will have a tailwind, as census hiring begins to have a positive influence on the data - lasting through May/June.

Day-over-day, the positive divergence in sector performance yesterday was in Healthcare (XLV). Within the XLV, the managed care index was up 1.6% on speculation that reconciliation will be difficult to pass. Republicans declared a parliamentary victory as they challenge the Democrats’ efforts to pass Healthcare legislation. CVH and AET were the two best performing stocks in the XLV

The Financials continue to take center stage, as the XLF has been one of the top three performing sectors all week. The banks finished higher for a sixth straight day, with the large-cap regional’s providing the upside leadership for the group; C continues to be the standout in the group.

Rounding out the top three performing sectors was Consumer Discretionary (XLY). Yesterday, retail continued to outperform the broader market with the S&P Retail Index +0.8%. The notable weakness in the sector was centered in the homebuilders; LEN, TOL and DHI were among the laggards.

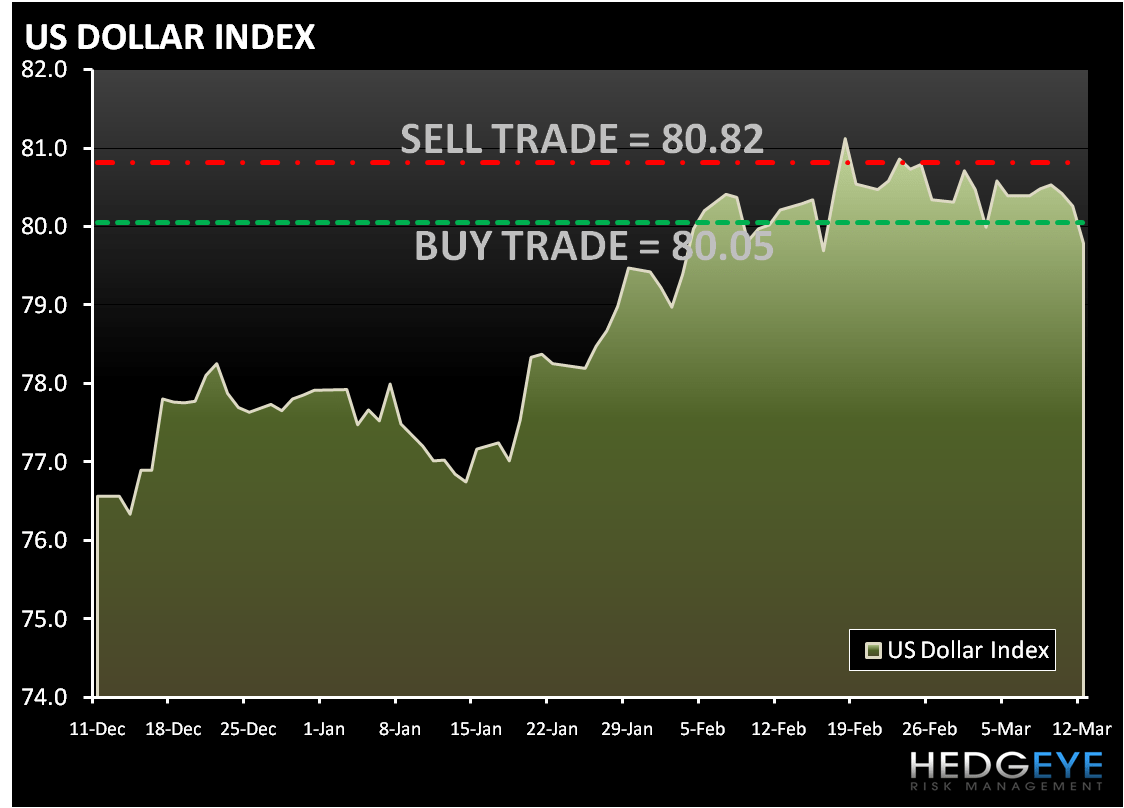

Volatility lost 2.7% yesterday and continues to be broken on TRADE, TREND and TAIL. The Hedgeye Risk Management models have levels for the volatility Index (VIX) at: buy Trade (17.29) and sell Trade (21.54).

As we wake up today, equity futures are trading modestly above fair value following yesterday’s outperformance. As we look at today’s set up the range for the S&P 500 is 24 points or 0.5% (1,132) downside and 1.6% (1,156) upside.

Today's MACRO highlights will be:

- Feb Retail Sales

- March prelim U. of Michigan

- Jan Business Inventories

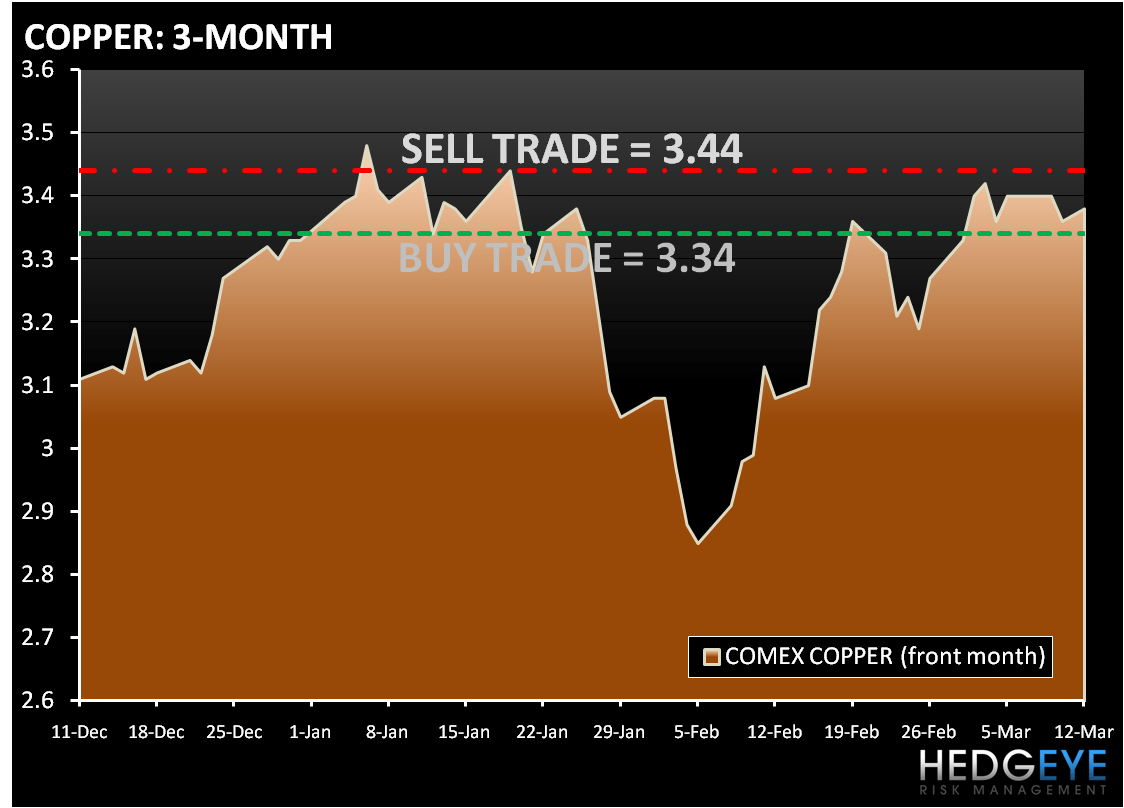

Copper is heading for a weekly loss on concerns that China may raise interest rates, slowing demand. The Hedgeye Risk Management Quant models have the following levels for COPPER – Buy Trade (3.34) and Sell Trade (3.44).

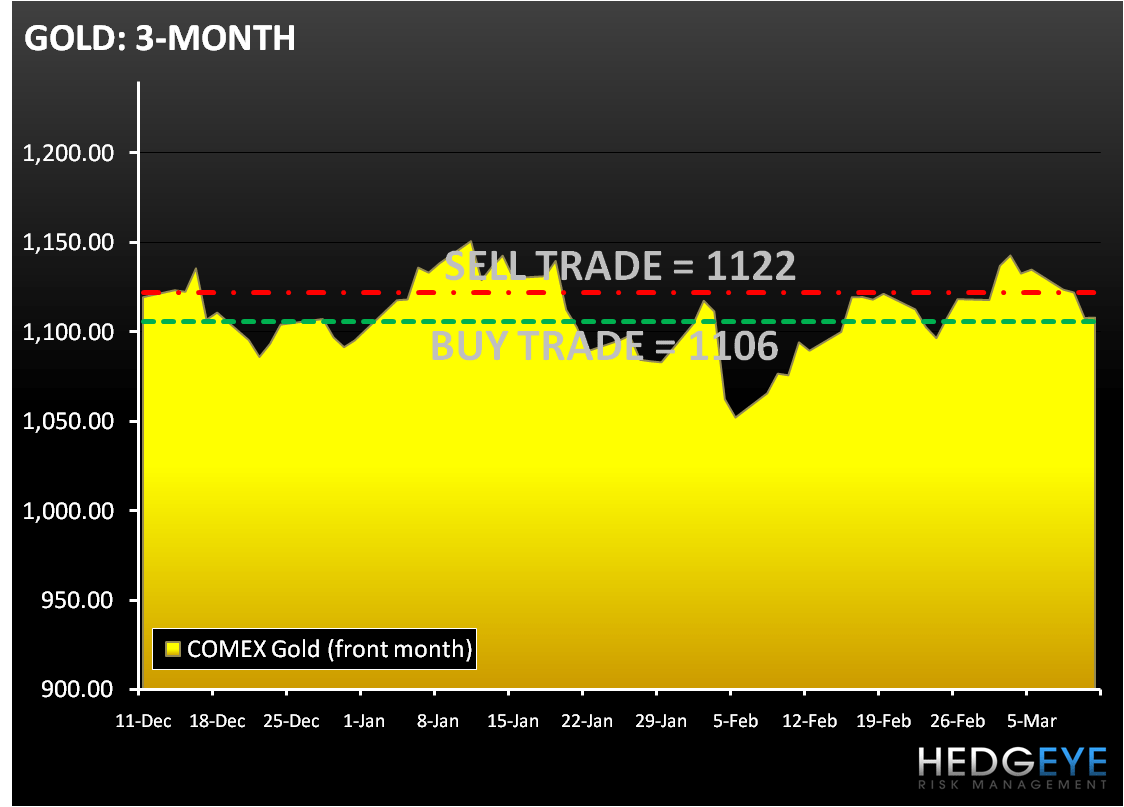

Gold is lower on speculation that governments around the world could pare economic stimulus measures, therefore dampening demand. The Hedgeye Risk Management models have the following levels for GOLD – Buy Trade (1,106) and Sell Trade (1,122).

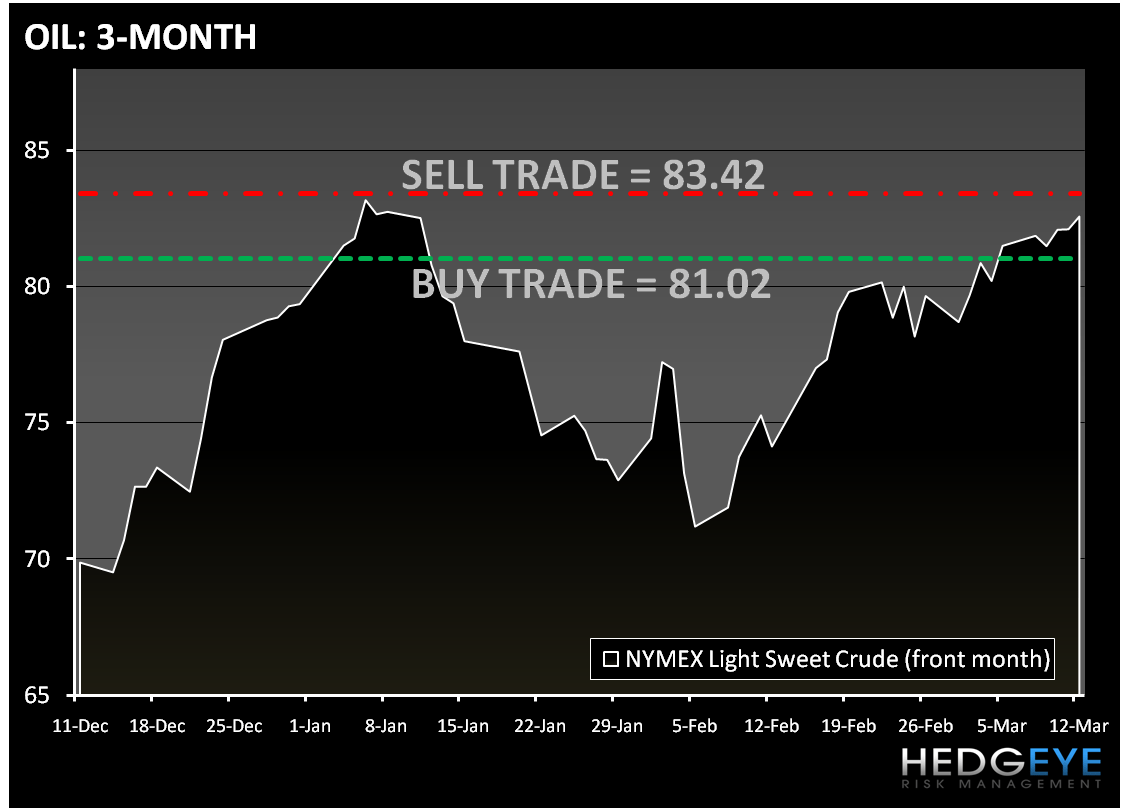

According to Street Account, the IEA increased its estimate for world demand in 2010 by 70,000 barrels a day to 86.6M barrels a day. That would mean a gain of 1.6M barrels a day, or 1.8%, from 2009 levels. The International Energy Agency raised its forecast for global oil demand this year for a second month as fuel consumption in Asia rises more than expected. The Hedgeye Risk Management models have the following levels for OIL – Buy Trade (81.02) and Sell Trade (83.42).

Howard Penney

Managing Director