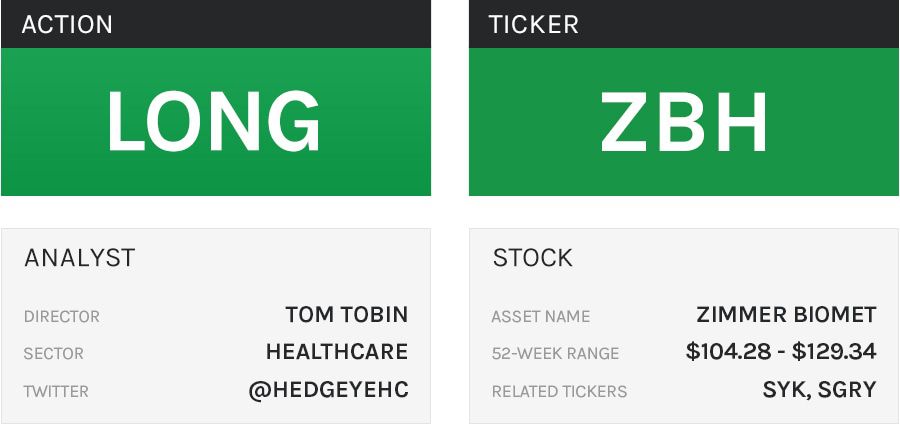

THE HEDGEYE EDGE

We see a pivot underway that will compress the spread in recent years between top ortho players Zimmer Biomet (ZBH) and Stryker Corporation (SYK). We believe the current valuation and consensus estimates for ZBH do not reflect the potential for a turnaround under new management from manufacturing issues, a salesforce disruption, and botched merger that cost the company significant market share.

BACKGROUND

In 2015, we introduced our "health care deflation" theme and challenged the consensus orthopedic volume and pricing assumptions of 5-7% and (2-3%), respectively. Our view called for implant volumes to decline in the U.S. due to high penetration, and the marginal impact of aging and obesity on growth.

Concerning device price, we expected manufacturers to cut prices at an accelerating rate in response to declining volume and provider pressure from the mix shift toward Medicare. Zimmer Biomet (ZBH) was our target on the short side due to the company's exposure to the U.S. reconstructive market relative to more diversified peers Stryker (SYK) and Johnson & Johnson (JNJ). The market itself proved more resilient, sustaining 5-7% volume growth with 2-3% declines in ASP, although we believe the acceleration of the insured population under the ACA and other tailwinds were key.

While ZBH experienced volume, price, and gross margins pressure over the last three years, it was mostly the result of market share losses from the mismanagement of the Biomet merger and supply problems at one of their manufacturing facilities. ZBH's share losses primarily benefited SYK, which experienced accelerating knee volume over this period.

MARKET OUTLOOK

Over the next 1-3 years, we expect volume growth will decelerate to 2-4%, which is in-line with growth in the osteoarthritis (OA) population in the United States. A significant and real downside risk to our estimates is over implanting, as penetration rates extend well beyond the population of patients with severe osteoarthritis, or those with the correct clinical profile for an implant. Incidence of total knee replacement, or total knee arthroplasty (TKA), will be pressured following significant increase over last 20-years which has resulted in 30% implant penetration into OA population.

Meanwhile, ASP declines will be limited to -2% to -3% over the next 12-18 months, but with significant risk for faster declines longer term and beyond the scope of this call. The key determinant for pricing trends will be facility level 3-year contracts, excluding the previously lucrative relationship between the rep and surgeon. Longer-term, we see significant downside risk to ASP as the number of large joint procedures being done in Ambulatory Service Centers (ASC) will accelerate, and hospital margin pressure intensifies.

BOTTOM LINE

We believe ZBH’s current valuation and consensus estimates do not reflect the potential for a turnaround under new management and resolution of self-inflicted manufacturing problems.

ZBH ceded ~300bps of market share in U.S. knee since 2015, and we expect ZBH to recapture a significant portion of this lost share rapidly. Currently, consensus estimates imply ZBH taking a modest 25bps of US knee market share in 2019 and 2020, assuming 2% market growth. We think this understates ZBH’s potential once they are back at full supply and strategic initiatives bear fruit.

We expect continued share gains in 2H18 with supply coming back online in 3Q18. We see 30%+ upside from current levels.

ONE-YEAR TRAILING CHART