THE HEDGEYE EDGE

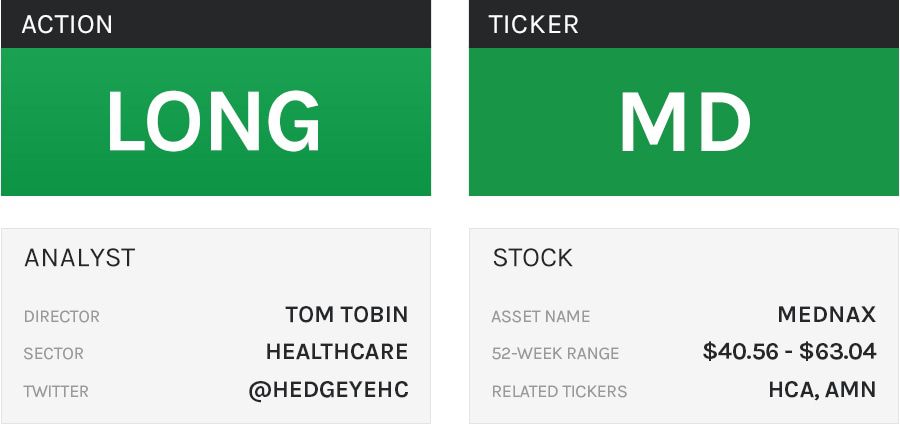

Birth rates appear likely to reverse a near multi-decade decline providing a tailwind to growth and margins for MD, which has suffered mightily from industry trends and self-inflicted missteps. The recent contract dispute with Atrium does not represent a return to the 1990s physician practice management bankruptcy cycle as some fear, but may actually validate MD's business model.

THOUGHTS ON THE PRINT

Mednax reported a positive quarter and stuffed several positive announcements into their 2Q18 earnings release. While maternity trends did not provide an extra same unit growth driver as we expected, same unit volume was inline.

Key callouts:

- Mednax’s CFO is retiring - Vivian Lopez will be replaced which is a significant positive in terms of communication and investor confidence.

- Incremental G&A cost cutting of $40M, or $0.30 per share.

- Incremental operational improvement of $80M, or $0.62 per share

- Buyback - added $500M buyback, or accretive by $0.30 per share assuming the company takes on debt to fund the program

- Practice salaries and benefits better than expected at 67.8% versus consensus of 70%.

Following the earnings release, the initially tepid move in the stock on the earnings release suggested there is lingering doubt management can deliver. Skepticism is warranted based on the margin destruction over the last 2 years, but executing a plan that drives EBITDA well north of $720M from the current run rate of $600M, our visibility into the mid $60s looks very attractive.

Flat births lead to NICU day growth of 0.1%, below our expectation of 2%. EBITDA guidance was on the surface disappointing, which calls for a decline of -3% to -8% year over year, however, adjusting the prior year for a +$5.5M EBITDA contribution from Southeast and the carrying cost of these physicians of $10M in 3Q18, the more accurate comparison shows EBITDA growth of +3% to +8% in 3Q18.

Data shows reported group practice member counts at Southeast have fallen from 116 as of March 2018 to 110 as of August 2018. As the company outlined, $10M in costs per quarter in the second half of 2018 are associated with these clinicians, although if the company helps these physicians move on more rapidly, there should be upside to results.

There were a number of questions focused on company guidance 3Q18 and beyond as it relates to carrying cost of Southeast and cost initiatives. The line of questioning took the position that while cutting G&A is concrete and believable, medical practice costs and margin improvement was less believable.

INTERMEDIATE TERM (TREND)

Maternity Stable to Improving: Birth trends appear likely to stabilize and inflect higher throughout 2018 due to Zika compare, demographics of marriage and maternity deferral turning positive as 30-39 age cohort accelerates, and a recovery in maternity, which is a positive tailwind for 50% of MD revenue and margins.

Activist Pressure/Take-Out: Activist investor Elliott Management has taken a 7% stake near $43/share which is driving take-out speculation. The activist is addressing productivity in anesthesiology helping to recover 100s of basis points of lost margin. In addition, the company has hired BofA to explore private equity interest. Lastly, consolidation among physician groups is accelerating, likely allowing MD to reaccelerate acquisition growth.

Physician Consolidation and Atrium Lawsuit: Consolidation among physician groups is accelerating, likely allowing MD to reaccelerate acquisition growth Irrational competition for deals appears to be abating; EVHC is under stress and appears to not be competing for deals as aggressively. Atrium, while a negative outcome for MD revenue, validates the model and is margin positive.

LONG TERM (TAIL)

With activist pressure and help from birth trends, the stage appears set for a good run of margin improvement, organic growth acceleration, acceleration in deal flow, and a recovery in the share price to the mid $60s and beyond suggesting 50%+ upside from current levels.

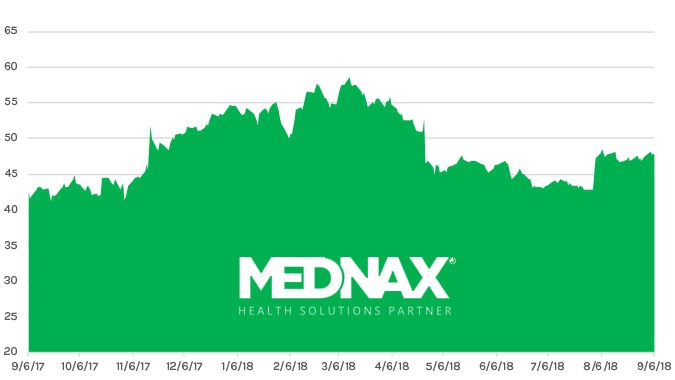

ONE-YEAR TRAILING CHART