The S&P 500 finished slightly higher by 0.17% yesterday, on a 25% improvement in volume. Notably, the advance-decline line deteriorated by 149 to 371. In our sector study it was surprising to see that 5 of the 9 sectors we track declined on the day.

For the second day this week, there were no big MACRO data points to help drive any one theme. The RISK AVERSION saw some signs of life with the dollar up by 0.2% and commodities flat to slightly higher. This dynamic seemed to weigh the most on commodity equities, particularly Energy (XLE) and Materials (XLB). The Hedgeye Risk Management models have levels for the Dollar Index (DXY) at: buy Trade (80.21) and sell Trade (80.87).

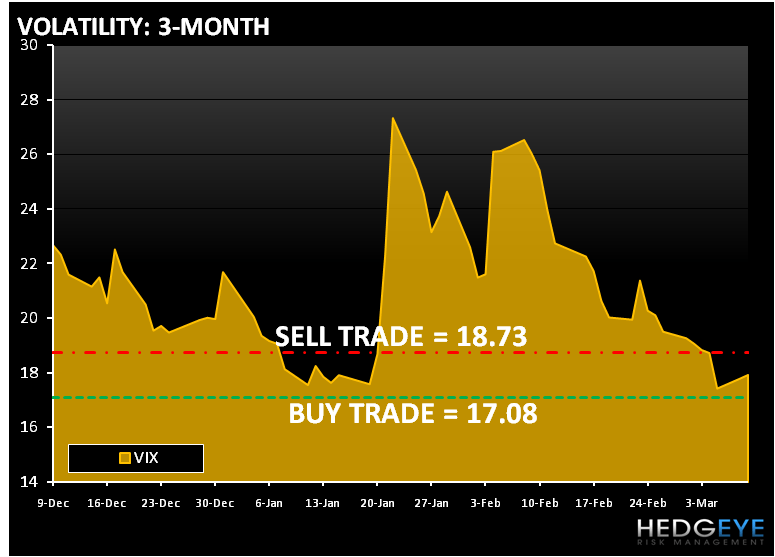

The VIX traded slightly higher over the past two day but continues be broken on all three durations - TRADE, TREND and TAIL. The Hedgeye Risk Management models have levels for the volatility Index (VIX) at: buy Trade (17.08) and sell Trade (18.72). Yesterday we sold our position in the VXX.

For the past three day the Financials (XLF) has been one of the best performing sectors and yesterday was no exception. Within the XLF, banking led the way, with the BKX +0.6%; the regionals were mixed with some renewed focus on capital needs. Credit-card and credit/risk-sensitive mortgage insurers were also stronger on the day.

Yesterday, we sold out position in Technology (XLK). The XLK has been leading the market higher this week, and now it’s finally immediate term overbought. Yesterday, both tech and telecom outperformed the broader market. The semis finished down slightly with the SOX down 0.2%; TXN was a drag following its mid-quarter update. Software was a bright spot with the S&P Software Index +0.7%.

Surprisingly, consumer stocks lagged the broader market yesterday. In the Consumer Discretionary (XLY) retail snapped a three-day winning streak with the S&P Retail Index 0.5%. On the positive side restaurants largely extended their outperformance despite weaker-than-expected Jan/Feb same-store sales out of BKC.

Yesterday the Materials (XLB) finished lower for a second straight day. The strong dollar can take most of the blame. CF, X and FCX were the three worst performing name in the sector.

As we wake up today, equity futures are trading above fair value ahead of another light day for corporate and MACRO data points. As we look at today’s set up the range for the S&P 500 is 27 points or 1.8% (1,122) downside and 0.4% (1,149) upside.

Copper gained for a second day after China’s imports of the metal rose 10% in February, adding to confidence that the economic recovery is gaining momentum. In early trading copper is trading lower after declining slightly yesterday. The Hedgeye Risk Management Quant models have the following levels for COPPER – Buy Trade (3.36) and Sell Trade (3.50).

Gold is slightly higher in early trading, after trading flat yesterday. The Hedgeye Risk Management models have the following levels for GOLD – Buy Trade (1,105) and Sell Trade (1,145).

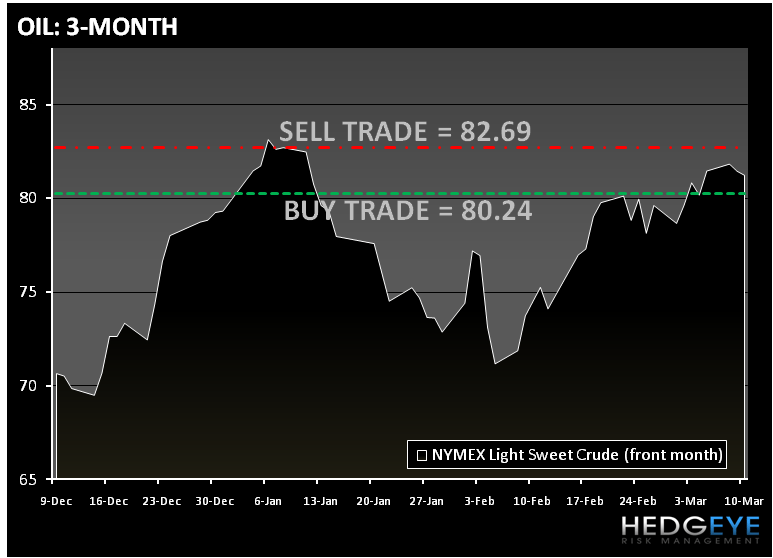

In early trading, oil is trading little changed as analysts forecast rising crude supplies in the U.S. The Hedgeye Risk Management models have the following levels for OIL – Buy Trade (80.24) and Sell Trade (82.69).

Howard Penney

Managing Director