Below are analyst updates on our fourteen current high-conviction long and short ideas. Please note we removed W.W. Grainger (GWW) from the short side of Investing Ideas this week. We also added Chipotle Mexican Grill (CMG) and Mednax (MD) to the long side. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

IDEAS UPDATES

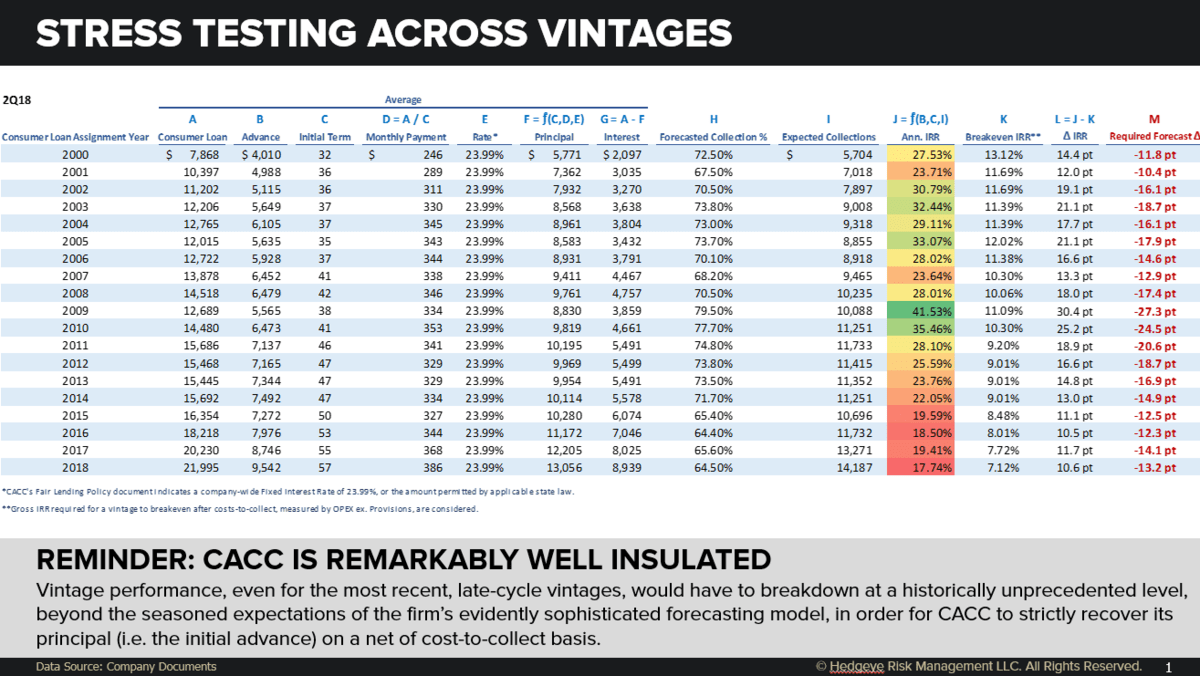

CACC

Click here to read our analyst's original report.

Credit Acceptance Corp (CACC) is remarkably well insulated. Vintage performance, even for the most recent, late-cycle vintages, would have to breakdown at a historically unprecedented level, beyond the seasonal expectations of the firm's evidently sophisticated forecasting model, in order for CACC to strictly recover its principal (i.e. the initial advance) on a net of cost-to-collect basis.

STAY

Click here to read our analyst's original report.

Most of the REITs beat the quarters, but only a few were willing to materially raise guidance for the year. In our opinion, which is backed by our forward looking data, we see an opportunity to take advantage of management’s overly conservative 2H guidance – we continue to like Extended Stay America (STAY).

Our model is projecting RevPAR growth in the +3% to +5% range, a range we believe is not discounted in hotel stock valuations, particularly the REITs. That 3-5% predicted range is more probable for full service urban hotels, while conversely we’d expect select service hotels to be a drag on headline Total RevPAR growth figures (due to the lapping of hurricane related demand in late 3Q and 4Q last year). Our positive RevPAR thesis should also benefit the C-Corps, but the real upside remains with the REITs like STAY.

GIL

Click here to read our analyst's original report.

Gildan is opening a new factory for the first time since 2012. The company sees demand growth from customers in basic Ts, fashion basics, and branded programs. Management also sees a structural change in the mass retail channel developing where retailers are replacing brands with their own private label programs in order to mitigate price comparisons with Amazon. Gildan believes it can win several private label contracts as it is the low cost producer with existing relationships with most of the retailers. With the opening of a new factory and the expansion of several existing plants Gildan can produce $800mm in revenues over the next two and a half years. From here the expansions will require minimal additional capex and SG&A. The $800mm in revenue would drive EPS of $3.00, 50% above the current year’s expectations.

MD

Below is a brief note from CEO Keith McCullough on why we added Mednax (MD) to the long side of Investing Ideas earlier this week:

|

Mednax (MD) is down -1.3% here today on #decelerating volume after ripping higher in early August back to Bullish @Hedgeye TREND. Here's an excerpt from my Healthcare Team's Institutional Research note post that quarterly report: MD | CAN THEY LAND THE DISMOUNT? Mednax reported a positive quarter and stuffed several positive announcements into their 2Q18 earnings release. While maternity trends did not provide an extra same unit growth driver as we expected, same unit volume was inline. What appears to be an initially tepid move in the stock on the earnings release suggests there is lingering doubt management can deliver. Skepticism is warranted based on the margin destruction over the last 2 years, but executing a plan that drives EBITDA well north of $720M from the current run rate of $600M, our visibility into the mid $60s looks very attractive. Sounds good to me. Buy the dip, KM |

SBUX | MCD | SHAK | CMG

Click here to read our analyst's original Starbucks report. Click here to read our analyst's original McDonald's report. Click here to read our analyst's original Shake Shack report.

Two industry heavyweights are set to share their unique, investable insights on which stocks are poised to win and lose in the months and years ahead.

We hosted an exclusive webcast between Hedgeye Restaurants analyst Howard Penney and Restaurants journalist Jonathan Maze, Executive Editor with Restaurant Business Magazine earlier this week.

In this special, in-depth investing discussion (featuring live viewer Q&A), Howard and Jonathan will discuss numerous big Restaurant stock winners and losers along with the key sector trends that are rapidly changing the game in the Restaurant industry.

In this presentation we discussed:

- What is the health of the overall restaurant industry?

- How is the trend toward delivery impacting restaurant stocks?

- Chipotle is in the “early innings of one of the greatest turnarounds you will see in the restaurant space."

- McDonald’s and Starbucks remain top Hedgeye short calls because "complexity is the silent killer of growth."

- What’s next for beleaguered Papa John’s (PZZA)?

- Takeaways on the casual dining space (examples include DRI, TXRH, CAKE, BLMN, DIN)

Click here or the image below for free access to the webcast (plus key takeaways).

CCL

Click here to read our analyst's original report.

For the 1st time since 2013, there were no hurricanes formed in the Atlantic basin in August, contrary to the wild Pacific ocean. As a result, sentiment from agents is improving on forward Caribbean bookings and bodes well for 2019. But that could change in September, one of the busiest months for hurricanes, with some weather forecasters already predicting some active Caribbean hurricanes. As for Caribbean pricing, Carnival (CCL) continues to lag behind its peers for 2H 2018 and heading into 2019 while RCL gained strength the last few weeks lead by Symphony of the Seas which arrives in Miami in Nov 2018.

UNFI

Click here to read our analyst's original report.

United Natural Foods (UNFI) announced recently that they have entered into an agreement to acquire SUPERVALU (SVU).

Margin differential between the two entities is drastic, a lot of which (but not all) has to do with the retail business of SVU. For FY19, UNFI’s gross margin is estimated to be about 14.9% while their operating margin is estimated to be 2.4%. Contrasting that against SVU’s estimated gross margin of 9.6% and consolidated operating margin of 1.4% and the operating margin on their Independent business of 1.9%. The rationale of levering up by three-plus turns to acquire a lower margin business with pension liabilities doesn’t hold water. Unless they fear what could happen with the Whole Foods contract (exposure to Whole Foods will decline from 33% of sales to 14%)?

As part of the acquisition, UNFI will also be buying into the food retail business representing roughly 100 stores under the banners of Cub Foods, Shoppers Food & Pharmacy and Hornbacher’s (20% of sales mix at SVU). Although they plan to divest the assets over time in a “thoughtful and economically driven manner” – what does that even mean? Sounds like it will take a while. SVU’s food retail business has been performing horribly and is burdened by multi-employer pension plans.

Given the strength of larger competitors in food retail and the investments in e-commerce that have been made, we feel that the under-invested in brands that SVU has will be difficult to sell. Furthermore, the retail assets could become a cash drain for the broader UNFI organization over time as they require capex of 1.25% to 1.75% of retail sales, whereas UNFI has been run-rating around 0.6% to 0.7% of sales.

Overall, we view this as a very troubling acquisition, that could cause problems for the company going forward. We believe this could be the beginning of an even greater downfall in the stock as the potential for missing targets and complications with integration mount.

ALRM

Click here to read our analyst's original report.

Alarm.com (ALRM) sits in the eye of market disruption as its leading position in interactive home security systems faces a torrent of new digital systems with innovative business models, customer acquisition, and technology. Meanwhile, the market opportunity for ALRM has exploded in the last few years, but ALRM has not. The stock is expensive on FCF…and OCF/EBITDA improvements in 2017 were mainly inorganic and not repeatable.

SGRY

Click here to read our analyst's original report.

While Surgery Partners (SGRY) revenue came in $15.9M ahead of expectations, adjusted EBITDA of $55.4M (which is manufactured) only beat expectations by $1.4M. Meanwhile, free cash flow to common equity holders continues to run negative at -$3M in 2Q18. SGRY's adjusted EBITDA margin of 12.5% declined 40bps YoY, as management continues to invest to "drive organic growth" in 2019. With adjusted EBITDA margins declining 154bps in 1H18, we continue to have a hard time getting to the ~150bps of 2H18 margin expansion needed to hit the 2018 consensus EBITDA estimate of $243.8M. Note management's 2018 guidance of at least $240M was before the impact of acquisitions, and we are modeling $234M including acquisitions and assuming COGS only increase 2% 2H18/1H18.

TSLA

Click here to read our analyst's original stock report.

What investors see isn’t what Tesla (TSLA) customers see, although that may eventually change. Will customers not test drive a Model 3 when the Tesla store calls to set up an appointment just because Elon Musk tweeted something provocative and probably illegal? So far, it doesn’t look that way. Like politics, we suspect Tesla will feel the personal financial situation – when the tax credits, HOV access, and competing models change the buying economics, the consumer will finally pay attention. We also expect build quality of the Model 3 to play a part, but the Model 3 is still a small part of the test drive mix. Sales are also likely to be impacted by declining residual values, which decrease trade-in values and generally increase total cost of ownership.

BYD

Click here to read our analyst's original stock report.

For the 1st time in 21 months, Seattle is no longer the fastest growing housing price market - that honor belongs to Las Vegas. According to Case-Shiller, Vegas home prices soared 13% YoY in June to its highest home price index value since January 2008. Digging deeper, North Las Vegas home prices continued to lag that of Balance of County through May 2018, according to LVGEA, although the margin has shrank somewhat since the beginning of the year. North Las Vegas existing home median closing price (TTM) is trending ~3% below that of Balance of County’s. For new home prices, the discrepancy is close to 20%. Boyd Gaming (BYD) has an outsized exposure to the North Las Vegas market.