“I’m not interested in what should be, could be, was. I’m interested in what is, what we control.” – Nick Saban

I’ve spent a lot of time studying and thinking about coaching this summer. While there are a lot of ideologies about what should be and could be out there, I’m most interested in coaching both who we have and what we can develop.

For those of you who coach anything in life and/or manage people at work, I’m sure you find it every bit as challenging as I do. It’s much tougher to lead and inspire people than it is to run a predictive tracking algorithm.

But can we inspire a broader population with principles and processes that go well beyond our in-house views? I’m not ashamed to say that I’m trying. There will be peaks and valleys in this journey. The best coaches coach through valleys.

Back to the Global Macro Grind…

As certain macro markets go through crashes and valleys, Wall Street has a central tendency to move towards calling all of the bottoms after rarely calling any of the tops.

That’s not coaching – that’s banking and brokering with a Bullish bias.

If you want to coach a Macro Team, start with some simple stuff like rate of change and the basic acknowledgement that making and/or saving money during major market tops and bottoms are processes, not “valuation” points.

But, but … “is Europe bottoming, because it’s cheap”… How about EM? “Too far too fast – everyone is long the Dollar now… and man it’s so cheap.” Oh and China, “why can’t they stimulate again or end the trade war?”

*Excerpts of many understandable client questions, those are.

And I empathize with the concerns. But don’t forget it’s my job to coach a team that gets to the answer on topping and bottoming processes before consensus Macro Tourists do. If there was a process driven “reversal” call to make, we’d make it.

Internally, here’s what a summary of a day in the life @Hedgeye Macro looks like on the research front:

Top Macro Callouts (from Darius Dale yesterday)

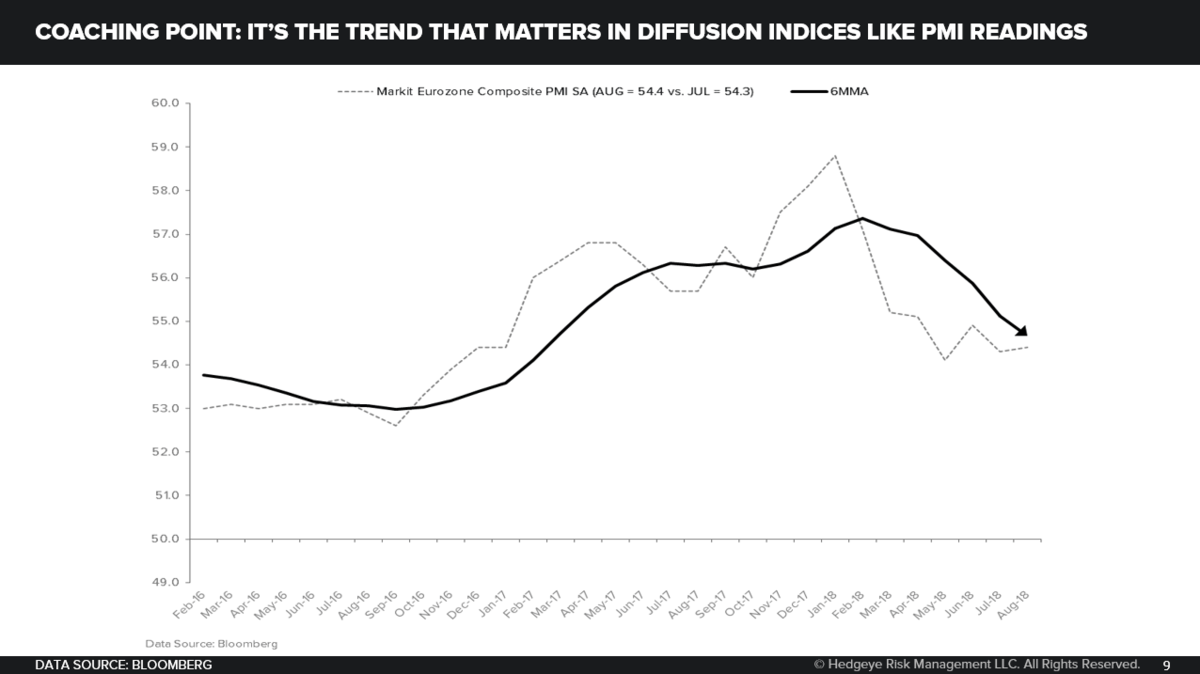

- Global Growth Is Likely to Continue to Slow Into Early-2019: There was something for everyone in the early batch of global PMI data for the month of August. Headlining the positive side of the ledger were the Eurozone’s preliminary Composite PMI reading (+0.1pts to 54.4) and Japan’s preliminary Manufacturing PMI reading (+0.2pts to 52.5), while Germany’s preliminary Manufacturing PMI reading (-0.8pts to 56.1) weighed on the preliminary Manufacturing PMI reading for the broader region (-0.5pts to 54.6). We are keen to highlight the fact that each of the aforementioned data series continues to slow from a trending perspective, underscoring our broader point that global growth is likely to continue to trend lower as the world economy traverses cycle-peak comparative base effects over the next few quarters. To that tune, I’ve attached our comparative base effect models for the world’s five largest economies, as well as Brazil; investors should note that comps for Real GDP growth steepen through 4Q18E for Europe and Japan, through 1Q19E for China, Brazil, and Emerging Markets in aggregate, and through 2Q19E for the U.S. As such, investors would be remiss to interpret one month of sequential strength – in a mean-reverting diffusion index nonetheless – as anything other than temporary reprieve from the broader trend of decelerating global growth – which itself should persist through at least year-end and perhaps into the early part of 2019.

- U.S. Junk Bonds Have Likely Bottomed, But Spread Risk Remains: Credit funds – FWIW a key upside driver of our own business in the YTD – should fear not our forecasted rotation from #Quad3 to #Quad4 in 4Q18E. In fact, they should welcome it given that junk bonds have likely already priced in what our GIP Model continues to suggest is the culmination of a record eight-consecutive quarters of accelerating YoY Real GDP growth domestically. Moreover, our proprietary analysis of the credit cycle itself continues to suggest that recession risk is unlikely to materialize at any point in the forecastable future (i.e. up to one year ahead). Looking to our GIP Model back-test data, we see that high-yield has historically performed well from an absolute return perspective in #Quad4; not so much in #Quad3 (think: margin compression). Credit spreads, however, do tend to widen in both of the aforementioned regimes and the performance of HY credit during #Quad4 typically lags that of IG credit – hence our call for credit investors to continually high-grade their respective portfolios.

- Are You Sure Beijing is Stimulating in a Meaningful Way? Because We’re Not: We’ve gotten a ton of questions of late regarding the likely economic response to the “wave of liquidity” Beijing has allegedly unleashed throughout the mainland over the past several weeks. Unfortunately for global growth bulls, that characterization is, at best, not true. To that tune, we’ve analyzed each of Beijing’s core policy drivers through our usual rate-of-change lens and, compared to the actual wave of liquidity they unleased from late-2015 throughout 2016, the current policy mix could best be described as “panicking to stay afloat”. Specifically, liquidity provision through PBoC Open Market Operations, Base Money growth, Bank Loan growth, the growth rate of Fiscal Expenditures, the General Gov’t Budget Balance, the growth rate of Infrastructure Investment, and the growth rate of Investment by State-owned Enterprises are all tracking considerably shy of their 2H15-16 averages. As guided to, however, the PBoC has indeed demonstrably boosted its Medium-term Lending scheme and has also followed through with comparable RRR cuts and the confluence of these factors are driving interbank lending rates lower on the mainland. We’ve seen that stimulate activity in the Chinese Property Market, which, in July, recorded its second consecutive month of sequential strength. This is important for investors to monitor because trends in the Chinese Property Market have historically led economic growth throughout the “Old China” economy broadly ~6 months. This implies the growth rate of China’s Secondary Industries is likely to bottom in/around the 4Q18E-1Q19E timeframe – which is precisely where the aforementioned comparative base effect model implies it should. Until then, Chinese economic growth is likely to continue to broadly trend lower across the preponderance of key high-frequency indicators – a trend highlighted most recently by the JUL PMI and JUL Freight Traffic data. All told, we are keen to reiterate our #ChinaSlowing theme after appropriately digesting Beijing’s latest policy tweaks.

In other words, we’re on it. We measure and map economic and market data all day, every day. On the economic data front, I coached Darius to do that. Almost 10 years into this, he now coaches all of his teammates to do that. He coaches me now too!

If you know of teams whose coaches completely missed China, Europe, and EM #GrowthSlowing in 2018, this is a great opportunity for them to be the coaches who learned something managing through a performance valley.

Sure, some of those macro exposures have and will continue to signal immediate-term TRADE #oversold within Bearish @Hedgeye intermediate-term TREND research views. We have a daily and dynamic timing process for that.

But, instead of trying to make calls on things our process doesn’t support, I humbly submit the bigger opportunity is to not miss the NEW macro calls our #process is making (like the topping process of #PeakCycle US inflation, for example).

If I sound like I’m trying to coach you this morning, I’m ok with that.

Like my teammates, many of our clients coach me with their data-driven perspectives too. I personally love being coached. Over time, dynamically evolving and data-driven teams will crush the individual who thinks they can know it all on their own.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND views in brackets) are now:

UST 10yr Yield 2.79-2.91% (bearish)

SPX 2 (bullish)

RUT 1 (bullish)

NASDAQ 7 (bullish)

Utilities (XLU) 52.71-54.85 (bullish)

REITS (VNQ) 81.28-84.77 (bullish)

Industrials (XLI) 74.09-77.73 (bearish)

VIX 11.23-15.08 (neutral)

USD 94.85-97.11 (bullish)

Oil (WTI) 64.04-68.70 (bearish)

Gold 1175-1210 (bearish)

Copper 2.55-2.76 (bearish)

Corn 3.57-3.76 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer