Editor's Note: Below is transcribed analysis from today's edition of The Macro Show hosted by Macro analyst Ben Ryan. Click here to learn more about The Macro Show.

|

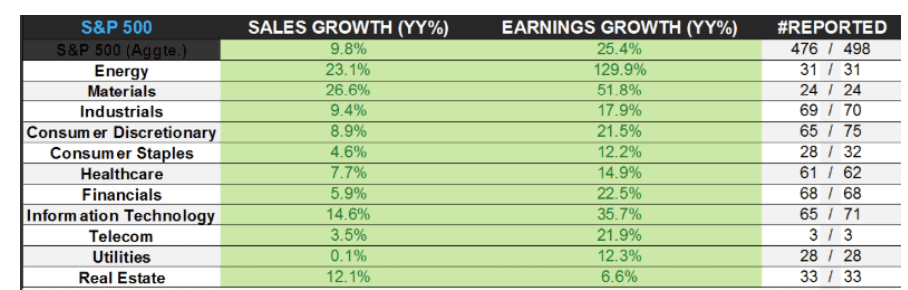

Ryan: So let’s go through an earnings update because we’re almost completely through 2Q 2018 earnings season. If you look at this chart (see below) it’s been a really positive quarter, especially from a second derivative perspective. What you’ve had is 476 of 498 companies reported. 9.8% is the sales growth number. That top line growth number is the hottest reported growth rate since Q3 2011. 25.4% is the bottom line, that’s the biggest delta since Q4 of 2010. Obviously those numbers back in 2010 were on the back of Great Recession compares. In other words, this looks like peak second derivative growth rates for both the top and bottom line. Every sector has reported sales growth. Every sector has reported earnings growth. The earnings picture looks a lot like what we see in year-over-year GDP growth. You’ve seen an acceleration but there are a lot of headwinds looking forward. Eventually these comps get steeper and steeper and growth flatlines. This is eventually going to be an issue, maybe next quarter but definitely in the fourth quarter. One of the key questions that we answered in our 3Q 2018 Macro Themes deck is after you’ve had such a positive environment for growth in margin expansion, what has to happen for companies to hit numbers and hit high estimates? What has to happen to make this second derivative growth in both the top and bottom line continue? In short, it’s hard to see. If you have a lot of inflation and commodity and heavy industry type companies can take price, that could drive the top line growth rate. But, if you look at the big platform companies, a lot of these companies are reliant on intangibles and branding, so the push and pull of inflation and deflation won’t impact their margins nearly as much. It's also worth noting, our outlook for the labor market and higher wage growth. This is another reason why we see margin degradation. |