THE HEDGEYE EDGE

Our extensive work on the extended stay yielded very bullish conclusions for the near and long term with Extended Stay America (STAY) uniquely positioned. The company still holds significant operating leverage (owns majority of hotels), making its near-term earnings positively leveraged to the accelerating RevPAR environment. Moreover, refranchising will contribute to significant free cash flow generation and more of an asset light growth model - a key driver of long term multiple expansion. Near term earnings upside, significant dividend growth, and long term multiple expansion make STAY one the most attractive investments in lodging, in our opinion.

Last year, much of the US macro economy was accelerating, but hotel RevPAR had yet to inflect. We’d owe this discrepancy to 1) the typical lagged impact the lodging industry typical commands, 2) political turbulence surrounding tax reform, trade deals, etc., and 3) supply growth that was still accelerating.

With much of this in the rear view, 1H 2018 has shown promise on the RevPAR front, and 2H 2018 should also deliver positive results. We remain bullish on the RevPAR cycle, but selective with our stock picks. STAY is among our go to stock picks, and we still see significant relative and absolute upside potential in its share price.

INTERMEDIATE TERM (TREND)

Ahead of 1Q 2018 earnings season, the REITs were trading at valuation levels that implied RevPAR deceleration, and even after the ~20% run, are not yet fully reflecting the top line opportunity.

Recently, we published our latest quarterly Macro RevPAR model output, which implies that the recent 4% RevPAR growth run rate could be sustained through the back half of the year – with room for upside.

M&A activity is also picking up in the REIT space. Wage and other cost pressures could crimp margins a little bit in the coming quarters, but faster top line growth and improving customer and ADR mix trends (business travel revival) will offer more upside to companies higher operating leverage. As such, we still favor hotel ownership as a lodging style factor into 2H 2018.

Even if GDP slows a bit, comps and moderate supply growth should equal higher RevPAR.

The fastest growing segment should warrant a little more attention, right? Extended Stay operates in a niche industry that’s somewhat under the radar, given the smaller base of rooms, but the demand growth trend is very impressive. Steady demand growth, decelerating supply, and easy RevPAR comps should create tailwinds for outsized RevPAR growth in the out quarters.

All told…

- STAY is in a small but growing sector within lodging. The segment was less than 2.5% of total lodging supply in the U.S. before 2014 but is now approaching 3.5%.

- Extended Stay represents close to 13% of the lower-end chain scale segment (midscale and economy scale).

- Demand growth is tracking up 3x the total U.S. industry – matched by above average supply growth, but concentrated at the high end (not STAY).

- ADR and RevPAR is growing at 5% and 6% CAGRs, respectively – 2 times the broader industry.

- All major hotel brand companies (C-Corps) are now involved in the Extended Stay segment, but at varying price points. HLT and MAR command the high end (big supply growth), and STAY, IHG, and CHH control the lower end.

- Lean staff contributes to hotel industry leading margins for the Extended Stay hotel owners (~45% vs. 38% for the industry), despite the high occupancy.

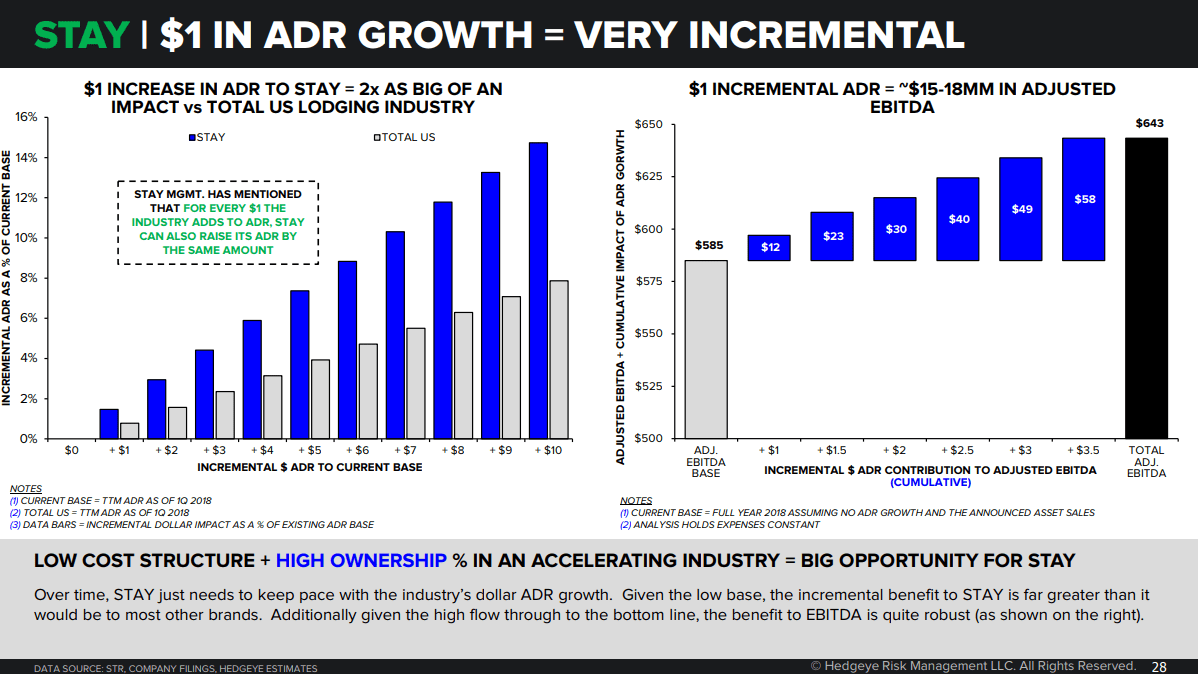

Furthermore, over time, STAY just needs to keep pace with the industry’s dollar ADR growth. Given the low base, the incremental benefit to STAY is far greater than it would be to most other brands.

Additionally given the high flow through to the bottom line, the benefit to EBITDA is quite robust (as shown on the right). given STAY’s high ownership %, if they are successful in the first round of refranchising efforts, they could accelerate another round of refranchising sales that would bring them towards considerably less asset exposure. In addition, various other drivers could them to a high growth profile in the coming years.

ONE-YEAR TRAILING CHART