THE HEDGEYE EDGE

Below are our top 10 reasons why Shake Shack (SHAK) is a short:

- Traffic has been declining for eight consecutive quarters, that’s not what we would call a growth concept! Traffic in 2Q18 was -2.6% vs. Consensus Metrix -2.1%. And yet the company talks about the health of the brand! The ultimate arbiter that determines brand health is customer traffic and they get a failing grade on addressing the declining traffic issue.

- SHAK has managed to have negative traffic in one of the best economic times for restaurants in over a decade! What will happen if GDP rolls over in the back-half of 2018 and into 2019 when the tax-reform bump becomes a difficult lap?

- SHAK continues to build an excessive number of new restaurants (system-wide restaurant count increased 33.6% in 2Q18, a 130bps sequential acceleration in the growth rate from 1Q18) sporadically around the country and world. This is a concept called ‘planned flags’ and greatly reduces supply chain efficiency and brand strength.

- Delivery will not be meaningfully incremental to sales, they have had the vast majority of their units available on three different aggregator sites and traffic is still down -2.6%. And they experienced 130bps of deleverage on the Other Operating Expenses line due to commission payments to third-party delivery providers. The incrementality and profitability of a delivery order needs to be called into question.

- Technology such as the app and self-order kiosks (which is late to the game) will not drive incremental sales. Looking at recent history for MCD and SBUX technology merely shifted the pinch points from before ordering to after. Without new capacity, actual sales can’t increase.

- Labor pressure is an outsized issue for a brand that strives to be far above minimum wage. They plan to pay a starting wage in Nashville (a new market for them) of $13 per hour, where the actual minimum wage is $7.25 per hour. How much can they possibly charge for a burger to cover the cost? Clearly with negative traffic consumers don’t like something…

- On the pricing front, with SHAK moving into “chain territories” (think Florida, North Carolina, Texas and Ohio) they will face increased competition they don’t experience as much in NYC, resulting in lower AUV’s and margin profile.

- They don’t disclose international same-store sales for a reason, they can’t be good.

- Permitting and construction costs delaying and increasing costs of new unit development – a process that is even tougher to manage in the planting flags approach.

- The stock trades at 24x forward EBITDA and 95x P/E – why would you pay that much for a brand that hasn’t grown traffic in eight quarters?

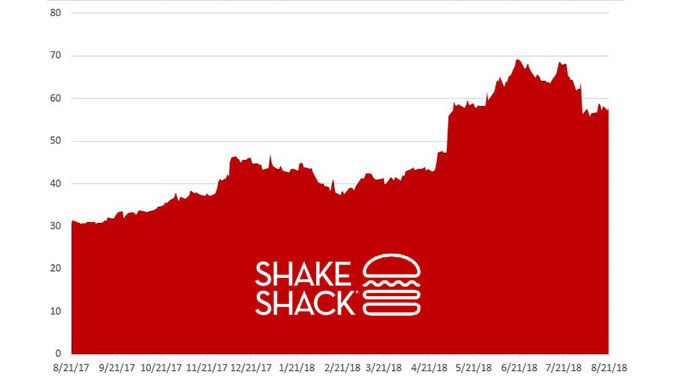

ONE-YEAR TRAILING CHART