Keith moved to neutral (from bearish) on the SP500 on the week of February 22. On Friday at 1139, for the immediate term TRADE, he moved back to bearish and shorted the S&P 500. This market is finally overbought!

The S&P 500 finished out last week on a strong note, with the S&P500 closing up 1.4% on Friday and up for six straight days. On the MACRO front, the calendar offered a fairly strong tailwind Friday as February nonfarm payrolls fell less than expected. In addition sovereign concerns continued to wane with the New Greek austerity package and the success of its 10-year bond sale.

In addition, there were no surprises out of China, as Premier Wen reiterated his aim of supportive fiscal policy and appropriately accommodative monetary policy. As a result, the VIX continues to confirm the RISK AVERSION trade. VIX declined 10.67% last week and today’s setup of the Hedgeye Risk Management models have levels for the volatility Index (VIX) at: buy Trade (17.29) and sell Trade (21.54). The VIX continues to be broken on all three durations – TRADE, TREND, and TAIL.

As we highlighted in our morning meeting, the Financials sector continues to provide leadership to the upside; the Financials were the best performing sector on Friday, rising 1.9%. The banking group led the way with the BKX +2.5%; regional and money-center names both out performed.

The employment data seemed to be a big catalyst for the Financials given the implications for the credit cycle. On Friday, nonfarm payrolls fell 36,000 in February vs. consensus expectations for a 68,000 decline. The unemployment rate held steady at 9.7%, while a Bloomberg survey was looking for 9.8%. Also note that the household survey showed a 308,000 increase in employment following the 541,000 gain in January. Average weekly hours fell a less-than-expected 0.1 to 33.8 in February, though average hourly earnings rose just 0.1% month-to-month and 1.9% year-over-year.

On Friday, Technology (XLK) moved to positive on TRADE and TREND. That leaves Utilities the only sector broken on TREND. Within the Technology, AAPL was up +3.9%, a bell weather for the group, broke out to new all-time highs after announcing that the iPad will be available in early April. We continue to be long the XLK.

Commodity-related equities largely outperformed on Friday. The RECOVERY theme got a boost on Friday from the February jobs number as the Energy (XLE) and Industrials (XLI) outperformed the S&P 500. Although, it should be noted that the dollar was down slightly on Friday and only up slightly for the week. Today’s set up of the Hedgeye Risk Management models have levels for the Dollar Index (DXY) at: buy Trade (80.08) and sell Trade (81.07).

As we wake up today, equity futures are trading modestly below fair value in what appears to be a slow start to the trading week on the heels of last week's move in the S&P. Today's MACRO calendar is void of any significant events. As we look at today’s set up the range for the S&P 500 is 37 points or 2.3% (1,113) downside and 1.0% (1,150) upside.

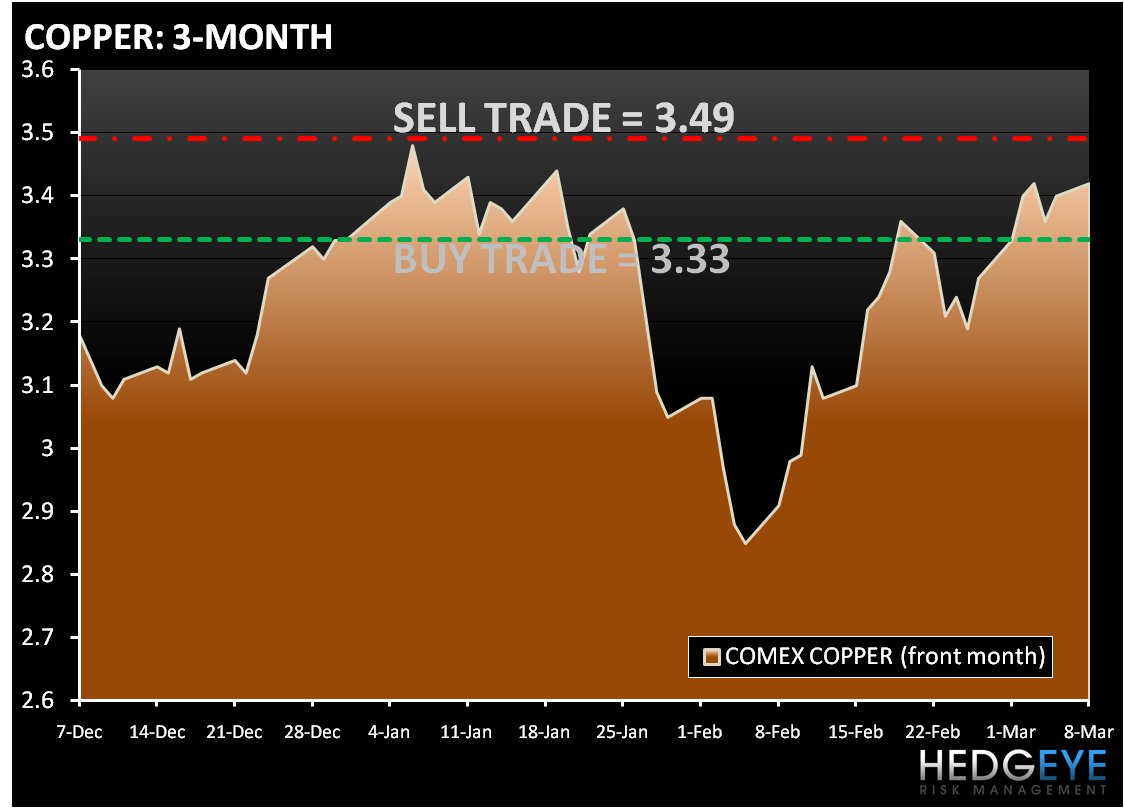

In early trading copper is trading higher for a second day as the weaker dollar and signs of improvement in the U.S. economy increased investor demand for copper. The Hedgeye Risk Management Quant models have the following levels for COPPER – Buy Trade (3.33) and Sell Trade (3.49).

Gold is slightly lower in early trading, despite the dollar trading slightly lower. The Hedgeye Risk Management models have the following levels for GOLD – Buy Trade (1,122) and Sell Trade (1,149).

In early trading, oil is trading at a two-month high above $82 a barrel in New York amid growing confidence that the economic recovery is proceeding and set to increase demand. The Hedgeye Risk Management models have the following levels for OIL – Buy Trade (79.74) and Sell Trade (82.13).

Howard Penney

Managing Director