Yes, this event was a disaster. Yes, it was spot-on with our short call across durations. And yes, the 20 mentions of [“we feel really good about…”] by the management team shows just how sub-par and complacent this team is. I’ve said this before and I’ll say it again…I don’t think this management team is lying when it hosts its bullish calls and analyst meetings. I simply think that it believes what is perhaps the weakest strategic plan I have seen out of any real company in my career. Our Black Book on Monday was titled “It’s Time to Start Shorting HBI Again; Champion is as Big a Liability as it is an Asset.” CLICK HERE I’m tempted to victory lap here, but I won’t. My job is to research business models and determine how an investment story will evolve from here. Based on everything I heard today, we’re still looking for a 15% 2H EPS miss – even on what are likely lower consensus numbers – and ~50% loss in equity value before this TGT C9 deal terms out.

This print was so much worse than a penny miss suggests. With just about every retailer/brand beating top line this quarter, HBI put up a slowdown in Innerwear to -3.4%, and a 100bps slowdown in global Champion on an easier compare. Bulls are believing Champion growth will accelerate to 30%+, and let's not forget the company highlighted the brand heat in its Investor Day, one would expect to see a sequential acceleration. Guess not. Oh, and by the way, Target just cancelled C9 (Champion sub-brand). If this is one of the hottest brands out there, why would Target cancel its exclusive? This is a $380mm top line hit, or 6% of the total business. If you wonder why Gildan is reorganizing and investing for a new world at mass, here’s why. There is a clear shift away from old undifferentiated brands to private label, and newer higher quality offerings.

This event was a wide open door for HBI to take down 2H guidance to give itself an easy bar to clear – the stock was going down today regardless (I’ll given ‘em the benefit of the doubt in that they had to know that). But it kept guidance high – setting up for additional downside later this year. We’re looking for a 10% miss in the upcoming quarter alone, and 60% by 2020 (ie we’re at $0.86 vs the Street at $2.10). I said it on several occasions and I’ll say it again…when all is said and done, this will prove to be the best short of my career. There’s terminal value here, but it all accrues to debt holders. Management is in denial as is anyone who will buy the equity today near $20.

Callouts:

McLean’s Modeling Callouts from the Print

Organic Growth

- Organic up 0.09%. Ok….I’ll give em a golf clap. Sales actually grew. But this is the best selling environment for sub-par retailers and brands that we’ve seen in nearly five years at a time when it has one of the hottest 90s retro brands in its portfolio – and yet it couldn’t muster more than 9 bps of growth?

- C’mon. This technically does mark the 3rd quarter of organic growth in a row (3Q of last year did not grow by our math). Now, however, the organic set-up is EXTREMELY difficult -- and yet not represented in management’s guidance.

Champion slowdown = BAD

- Champion is growing great, right? It’s going to accelerate to +30%, right? So why then did it slow 100bps in a great retail environment with the brand selling out everywhere, and against an easy compare. Now compares get harder, and we think there is real risk of this slowing further in the coming quarters. Perhaps management top ticked Champion growth by having an investor day to tell everyone how great it was doing.

- Our HBI deck on Monday (link above) has more on why we think Champion is a borderline liability and not the reason to buy the stock. The fashion heat will reverse at some point, we are two years into the brand ramp – and these retro growth bursts usually last 2-3 years before reversing course. I’m willing to bet big that management is modeling Champion as a perpetual grower. In fact, even after losing the $380mm in C9 at TGT, it still thinks its $2bn goal is attainable. I’m not there…

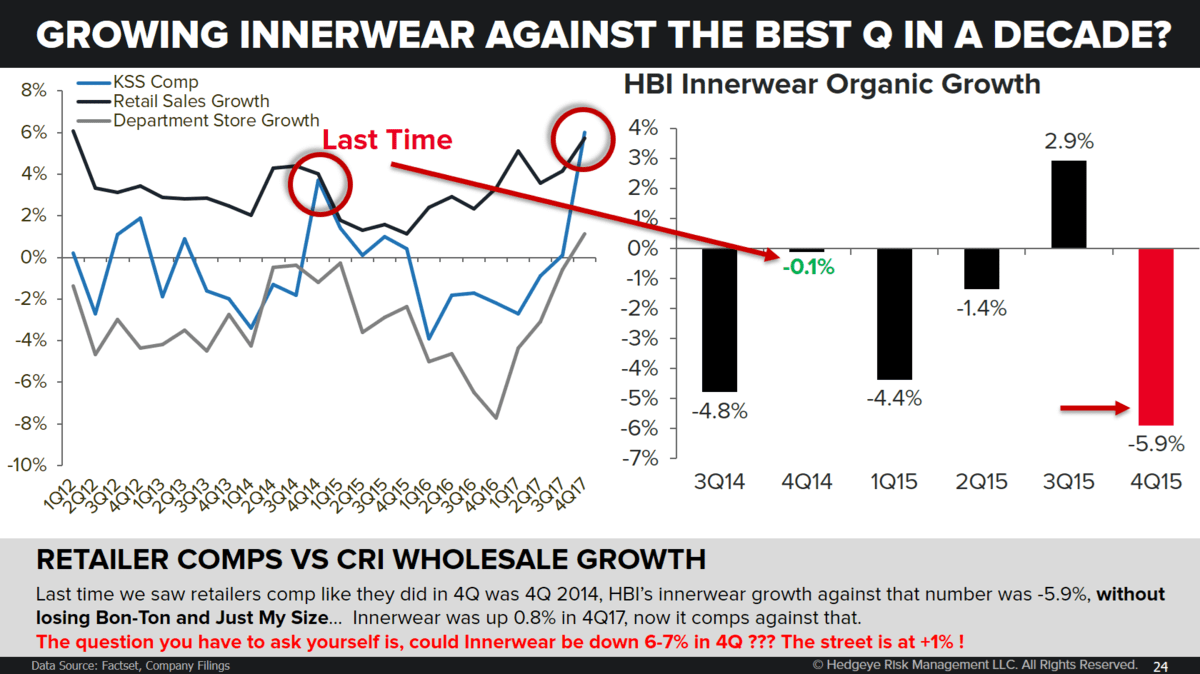

Innerwear weak with big 2H Risk

- Even in what has been a great retail sell through environment, HBI’s Innerwear slowed on a 1 and 2 year basis, down 3.4%.

- The 3Q compare is easy, but 4Q is very difficult at +1% aided by a great B&M US retail comp last holiday. But don’t forget that HBI just lost Just My Size in WMT and lost all Bon-Ton doors. That impact will likely be bigger in 2H. The question you have to ask yourself is, could Innerwear be down 6-8% in 4Q? The street is at +1%. Why? Bc that’s what the company says.

Activewear growth in trouble with C9 loss

- The C9 partnership with TGT is being cancelled as of Jan 2020. That’s a 6% hit to total sales and 22% hit to Activewear. Management stated that C9 was not in its Investor Day guidance, saying “frankly, at the time of the Investor Day, the renewal was still pending. So we specifically excluded it from our CAGR in the 1% scenario. Said differently, frankly, if the contract had been renewed, we would have significantly exceeded those goals.”

- Though, let’s not forget that the day of the Analyst meeting the head of Activewear stepped down deciding to take a professional three-year sabbatical (going on a mission trip). Perhaps the head of Activewear knew he was losing his biggest customer accounting for 25% of the business.

- Management is guiding that 2019 C9 sales should not see a difference vs the current 18 plan, however we expect it to comp down due to Target starting to allocate space to its planned replacement, likely private label options. If Champion was your growth driver, you are now befuddled since C9's lost sales will likely offset Champion growth upon contract expiration.

- At least when C9 comes out of the base, we can see the bigger impact of the Champion brand heat. Unfortunately, that’s 2 years down the road, and by then And1 and Juicy will be cool again instead.

- Management wouldn’t give detail on C9 margin profile, which signals to us that it’s more likely to be higher margin than the Activewear segment’s ~15%. HBI would probably be happy to share if it was margin dilutive, now that it’s going away.

What happens when International really slows?

- Organic international was +5.1% slowing from +6.6% last Q, though against a tougher comparison. We think International presents a looming risk. It’s doing well today with help from rapid growth in distribution for Champion in Europe and Japan.

- The rest of the business is not so hot, and we think sourcing integration of acquired brands means lower quality product and share risk. Europe is slowing, Australia will probably face a large housing driven recession (someday, not today), and FX is no longer helping. What happens if when we lap Bras N Things’ closing next year, the International segment is reported down MSD%?

Credibility

- We have to point out the fact that management held an investor day at the stock lows, 2 weeks after a quarter release, without changing strategy, or changing guidance, or doing anything other than buying some shares to change the story. And the following quarter’s print was a disaster.

- In fact one point management highlighted in that investor presentation was the fact that private label was not a risk. Yet today the company announced it will lose $380mm in business at TGT, and it is likely losing out to private label.

- We have to question why management’s confidence and good feelings about its business should have any credibility when it seems to have no command of its business.

- Also we struggle to acknowledge the validity of the company’s comment on cotton, which was:

- “But what I want to say first is we're no longer a cotton dependent company, as many people often think we are.”

- What are those Champion sweatshirts and Hanes tighty whities made of? Silk?

- We understand that the company’s dollar value of "raw" cotton buys are much lower than they used to be as the owned manufacturing % of COGS has gone down, and cotton prices have declined. But HBI still has exposure for every thread of cotton in its brands’ products. Raw materials inflation is guided to have a $35mm (50bps) negative impact this year, net of price increases. So as we see it, cotton goes up, margins go down.

Model changes:

- Taking up 3Q revenue slightly, was overly bearish on innerwear against an easy compare. Also taking up “other segment” given sequential improvement.

- Taking tax rate to 15% in perpetuity. I think HBI is over estimating its 16%.

- Taking 2019 and 2020 Activewear down given C9 pull back and cancellation.

- Also taking down 2019 and 2020 SG&A, assuming HBI reduces that which is associated with C9.