Have you ever sat back after two days and said something like ‘wow…I can’t believe we spent so much time on this and still have no answer?’ There’s my thought process right now around UAA inventory accounting. Retail is a simple game folks. An average-intelligence third-grader should be able to make sense of retail inventory adjustments. But for the life of me, I still cannot figure out what UnderArmour did this quarter, and both the auditor-blessed accounting as well as the reason for it are both perplexing me. I can hypothesize, but I don’t have the answer. That doesn’t happen too often on my team. That in itself is a callout.

Here are some of the facts...

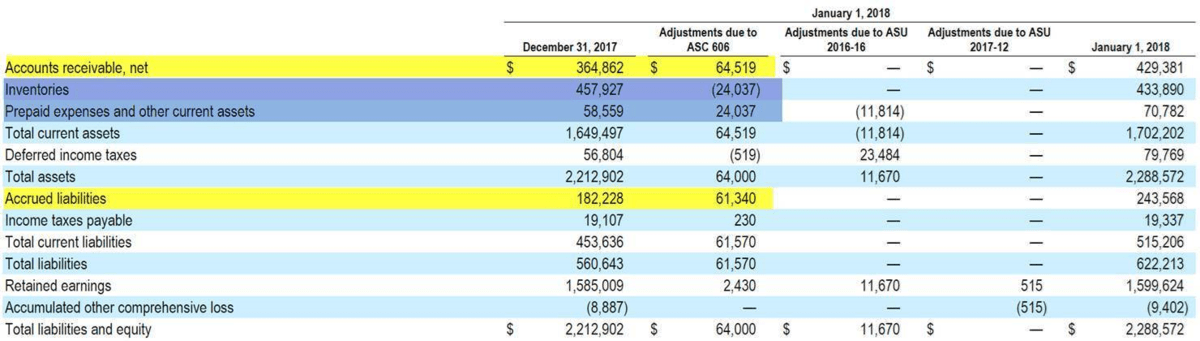

Adoption of ASC 606: Sale with a Right of Return

606-10-55-22 In some contracts, an entity transfers control of a product to a customer and also grants the customer the right to return the product.

606-10-55-23 To account for the transfer of products with a right of return (and for some services that are provided subject to a refund), an entity should recognize all of the following:

a. Revenue for the transferred products in the amount of consideration to which the entity expects to be entitled (therefore, revenue would not be recognized for the products expected to be returned)

b. A refund liability

c. An asset (and corresponding adjustment to cost of sales) for its right to recover products from customers on settling the refund liability.)

In the first quarter 10-Q, UAA announced plans for the adoption of ASC 606 into the firms reporting structure. The company had previously net reserves for returns, allowances, discounts and markdowns against accounts receivable. In line with the new accounting standards UAA will now recognize reserves for returns, allowances, discounts and markdowns within a customer refund liability, rather than a net against accounts receivable. The value of the inventory associated with reserves for sales returns will be included within prepaid expenses and other current assets. Yes…a prepaid expense.

From our research of the consumer discretionary space only COLM and UAA appear to have adopted this reporting structure so far this year. COLM’s adoption is squeaky clean – written for (but not by) a third grader. UAA is polar opposite.

UAA First Quarter 10-Q

In the 10-Q UAA has broken out a customer refund liability of $353mm, which based on ASC 606 accounting methods is essentially the value of the reserves for returns, allowances, discounts and markdowns. This was previously net against receivables. The reserve for returns has two components. First, the company must account for the loss of sale in the channel and second must account for the value of the inventory returning to UAA. Regulation wording implies that the value of the inventory that UAA expects to be returned is ~$97mm (prepaid expense line).

COLM First Quarter 10-Q

COLM has made the same adjustment in terms of removing its reserves from returns as a net against receivables, yet has opted to offset the increase in accounts receivable by increasing accrued liabilities by roughly the same amount. COLM also recognizes the value of inventory associated with expected returns as a prepaid expense. However the difference is that COLM is clearly offsetting the value of the prepaid expense by proportionately decreasing reported inventory values.

So COLM is booking a one for one adjustment between prepaids and inventories. On the other hand, UAA with a near 10x larger adjustment in aggregate is writing up prepaids by $97mm, which per 10-Q language are directly associated with inventories yet are disclosing a mere $3mm dollar impact to inventories. The opacity is stunning.

606-10-55-27 says that an asset recognized for an entity’s right to recover products from a customer on settling a refund liability initially should be measured by reference to the former carrying amount of the product (for example, inventory) less any expected costs to recover those products (including potential decreases in the value to the entity of returned products). At the end of each reporting period, an entity should update the measurement of the asset arising from changes in expectations about products to be returned. An entity should present the asset separately from the refund liability.

Based on this disclosure from the ASC 606 document it is possible to hypothesize that COLM is able to recognize the full value of the expected inventory returns whereas UAA feels there is very little value in the inventory being returned. So we are supposed to believe that UAA is over shipping ~$97mm of inventory with the expectation that the returns will be valued at ~$0.03 on the dollar? ($3.5mm on BS/ $97mm prepaid). If I was bullish on UA I’d hope to have a lot more confidence that the recapture would be $0.50-$-0.60 on the dollar – at the absolute worst. Something’s off here.

It can get very dangerous hypothesizing rationale for this accounting/behavior…but also consider the following.

In the 2017K, UAA disclosed that the company was increasing its allowance for returns by $100mm or 70% from $146.2mm to $246.6mm. Does not take a genius to surmise that management saw an inventory overhang and took the early hit to clear ’17 product to set up for full price sell through for ’18. Then on the 2Q call management said “So I would say full year is slightly higher than prior year relative to that channel but it's really helping us drive down the overhang of inventory that we spoke to relative to 2017 and setting ourselves up to be clean going into 2019.” Then sales at wholesale increased 9% in 2Q marking a steep acceleration from the down LSD 1Q report on a very similar yy comparison. Also noteworthy is the fact that the wholesale growth of 9% outpaced the 7% DTC growth in 2Q while NKE and ADS simultaneously continue to prioritize sales in their own direct channels.

I could go as far as to say that management increased the reserve only to jam the year with current season product and remove unsellable inventory off the books. There’s a few conspiracy theories I’d throw in as well. But in the end, the fundamental question is why UAA has to get so aggressive in managing excess inventory in the first place? The fundamental problem is that it is simply producing too much undifferentiated product and stuffing into poorly matched channels. Check out that Costco inventory and compare against what UAA is selling in KSS (finally anniversaried) and DKS. There’s not that big of a difference. This near term accounting patch might be an auditor-friendly way to ameliorate a near-term product problem. But the bigger deal for me is whether this company can put up a top line relative to consumer demand without a meaningful downshift in profitability.