The guest commentary below was written by Dr. Daniel Thornton.

I’ve argued that the Federal Open Market Committee’s (FOMC’s) low-interest-rate policy, large-scale-assetpurchase program (aka, QE), and forward guidance have not only been ineffective, but harmful. I’ve argued here that the FOMC’s low-interest-rate policies of the last 30 years have reduced the growth of output and employment. I made the case that the Fed is monetizing the debt here. I have shown that the FOMC’s QE policy has produce a dangerously large amount of liquidity, in the form of total checkable deposits, that could eventually have consequences for inflation here and here. I’ve explained why the FOMC’s policies have failed here, here, and here.

In this essay, I explain what monetary policy can do.

The thing the Fed can do that is effective during financial crises is increase or decrease the amount of credit it supplies to the credit market. It can do this in two ways. It can do it by making loans. It can do it by purchasing securities. The Federal Reserve Act severely limits who the Fed can lend to during normal times, but allows the Fed to purchase a wide range of securities. Both methods have the same effect on the supply of credit.

However, the Fed has historically done this by buying or selling securities in what’s called open market operations. The analysis that follows shows that the massive increase the supply of credit immediately following Lehman Bros. bankruptcy announcement on September 15, 2008, brought an end to the financial crisis and the recession.

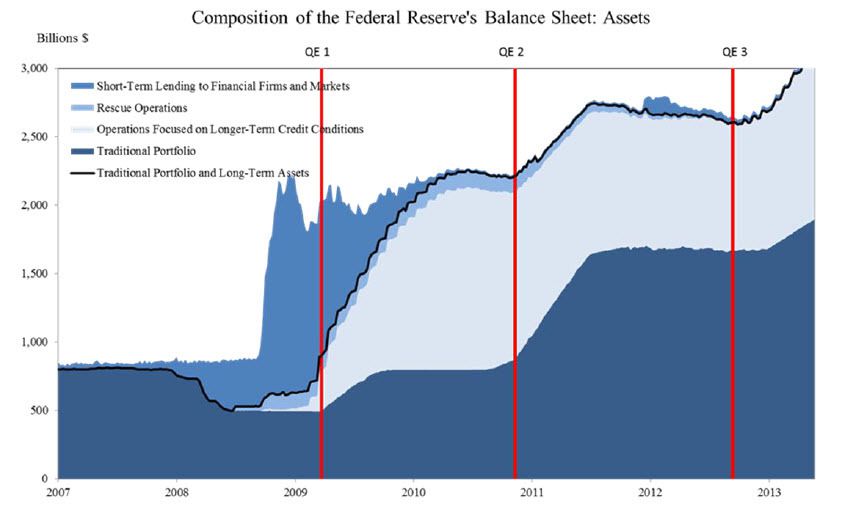

The figure above shows the amount of credit the Fed supplied to the credit market from January 2007 through June 2013. From January 2007 to Lehman Bros. bankruptcy announcement, the Fed kept the amount of credit it supplied constant at about $890 billion. The Fed made loans to financial institutions in the amount of about $300 billion during this period, but sterilized the effect of this lending on the supply of credit by selling an equivalent amount of Treasury securities. This is shown in the figure above: The lighter blue area, denoted as short-term lending to financial firms and markets, increased while the darker blue area, denoted as the traditional portfolio, declined by an equal amount.

Rather than increasing the supply of credit to mitigate the effects of the financial crisis and, thereby, stabilize the economy, the Bernanke Fed implemented monetary policy by reducing the target for the federal funds rate from 5.25 percent (its level on August 9, 2007) to 2 percent on April 30, 2008. That this policy was ineffective is witnessed by two facts. First, the recession, which began on December 2007, worsened significantly during this period. The unemployment rate increased from 4.6 percent in August 2007 to 6.1 percent in August 2008, and industrial production and real output dropped significantly. Second, the financial crisis intensified. The Fed took $29 billion of “toxic” assets on its balance sheet in mid-March 2008 in order to affect the bailout of Bear Stearns by JPMorgan Chase. Indeed, the financial crisis culminated in the bankruptcy of Lehman Bros. on September 15, 2008—the largest bankruptcy in U.S. history (see the Federal Reserve Bank of St. Louis financial crisis timeline, here).

Lehman’s bankruptcy was a financial disaster. Credit risk spreads, which had risen somewhat since August 9, 2007, exploded immediately on Lehman’s announcement. The Bernanke Fed responded by making massive loans to banks and other financial institutions. The amount of credit the Fed supplied increased rapidly from about $890 billion on September 11, to $2.2 trillion on December 29. The Fed’s lending was intentional, but the massive increase in the supply of credit was not. Bernanke took an unusual step to sterilize the effect of this lending on the supply of credit.

At his behest the Treasury announced the Supplementary Financing Program (SFP) on September 16, 2008, whereby the Treasury would issue marketable debt and deposit the proceeds in a new account at the Federal Reserve. This program was begun for the sole purposes of sterilizing the effect of the Fed’s lending on the supply of credit. The effect of this action was to sterilize the Fed’s lending by the amount of the securities issued. Indeed, the increase in the supply of credit would have been about $410 billion larger by the year’s end were it not for Bernanke’s effort to sterilize it (the Treasury’s balance with the Fed increased by $410 billion—$289 billion in the supplementary financing account, and $121 billion in the Treasury’s general account).

That the massive increase in the supply of credit was effective is evidenced by two facts. First, many risk spreads had returned to the pre-Lehman levels by late January 2009. Indeed, some spreads were back to their pre-August 9, 2007, level (see Should Have, Figures 1 & 2). Second, the recession, which deepened dramatically following Lehman’s announcement, ended in June 2009—just nine months after the largest bankruptcy in U.S. history!

Think about it. The financial crisis begins in August 2007; the recession in December 2007. The FOMC reduces the federal funds rate target by 325 basis points and lends about $300 billion to financial institutions but prevents this lending to increase the supply of credit. The result: the financial crisis and recession intensify. On September 15, 2008, the economy gets the largest jolt since the 1929 stock market crash. The Fed massively increases its lending to financial institutions. Bernanke attempts to sterilize the effect of this lending on the supply of credit, but can’t. The Fed did not have enough other securities in its portfolio that it could sell and the Treasury couldn’t do enough through SFP. Consequently, the supply of credit increased dramatically. The effect was spectacular! Just four months later the financial crisis shows dramatic signs of healing; nine months later the recession ends.

As far as I know, I’m the only economist to comment on this remarkable monetary policy success story. I’m at a loss to understand why. The verbatim transcripts of FOMC meetings show that neither Bernanke nor any other FOMC participant understood that increasing the supply of credit was the monetary-policy tonic that the financial crisis and recession needed (see Stumbled and Requiem for QE). Policymakers were so conditioned to believe that monetary policy only can work through interest rates that they couldn’t conceive of it working another way. This is likely the reason that other economists haven’t noticed this remarkable success story either.

Conclusion: During financial crises, the Fed should respond by massively and temporarily increasing the supply of credit to give financial market participants to take the actions they need to heal themselves and financial markets, and for economic resources to be reallocated. Ideally, this should be done by making loans to financial institutions because no action is required to return the balance sheet to normal—the loans will be repaid as financial markets normalize and the economy heals.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor piece written by Dr. Daniel Thornton. During his 33-year career at the St. Louis Fed, Thornton served as vice president and economic advisor. He currently runs D.L. Thornton Economics, an economic research consultancy. This piece does not necessarily reflect the opinion of Hedgeye.