As we highlight each week, initial unemployment insurance claims have for the last six weeks been moving higher. They've broken out of the three standard deviation channel we consider an important barometer. Given that claims are starting to go in the wrong direction, we've screened the Financials universe looking for the stocks with the highest R-Squared values to initial claims. The following chart shows the 45 stocks most correlated with initial claims. For reference, our screen looked at 170 Financial companies.

A quick caveat. Are all of these stocks actually being driven by claims to the extent suggested above? The answer is clearly no. Some of these high R-Squared values seem spurious. For instance, Aflac (AFL) appears to have 85% of the movement in its stock price explained by changes in claims, yet Aflac's principal business is disability insurance in Japan. So in this case, we think the correlation is more coincidental than causal. On the other hand, Capital One (COF), which shows a R-Squared value of 0.74, has a tight connection between earnings and general levels of employment, so in this case the high R-Squared value seems appropriate.

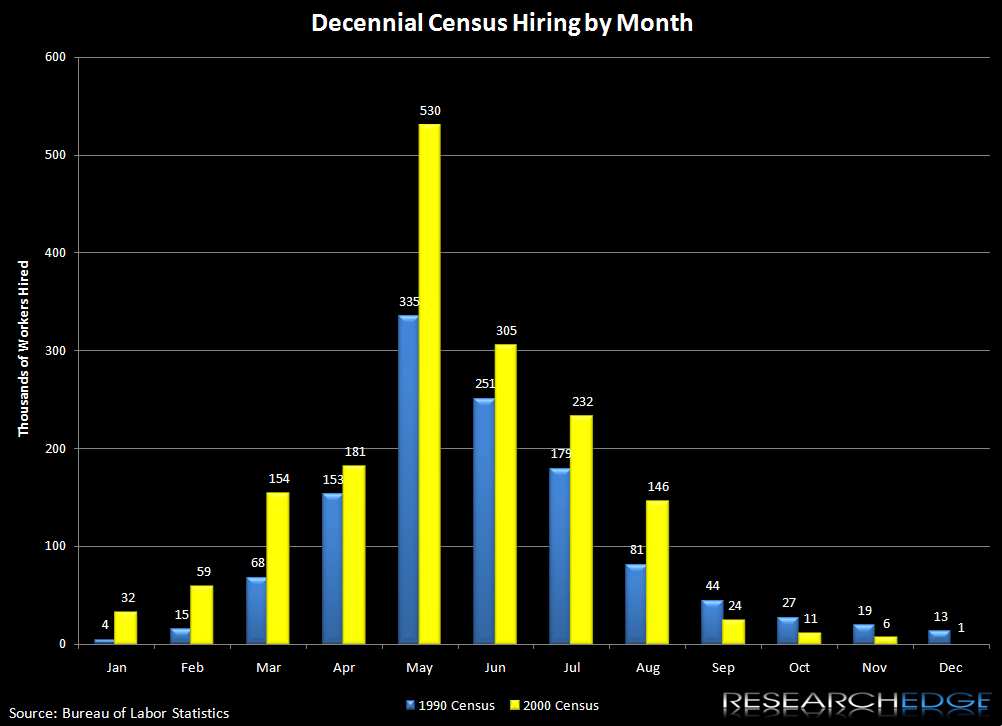

So what do we expect out of claims going forward? Our view is that claims are likely to resume their downward trend in the coming months for two reasons. First, there were numerous reports that the snowstorms throughout January/February adversely impacted the data. This wouldn't be the first time. For instance, in January 1996 a blizzard not unlike what we experienced this past month left most of the East Coast of the United States at a standstill. In the following weeks, initial claims rose 82k to 415k from 333k, only to then drop back down in the following weeks. Second, we think the census hiring will provide a tailwind for claims on the margin, as that hiring ramps up in earnest in March, April and May. The following chart shows census staffing levels by month over the last two censuses. This census is expected to require approximately two times the number of people needed in the last census.

If we're right about claims moving lower over the next few months, we would recommend long exposure to the high R-Squared names that have also seen their stock prices drop in the last six weeks - the duration over which claims have been on the rise. The following chart shows graphically which companies may be best positioned to benefit from a recovery in claims. On the x-axis is the R-Squared to claims. On the y-axis is the percentage change in stock price since January 15, 2010 - the date of the first of six negative prints on claims.

For those uncomfortable taking a view on claims, the following are some of the names with low, or no correlation to claims.

Finally, we republish our claims chart below for reference.

Joshua Steiner, CFA