The guest commentary below was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

Last week we posted a snippet from Rob Chrisman’s housing finance blog about former Fed Chair Janet’s Yellen being "puzzled" due to the lack of home ownership by Millennials. The ensuing reaction was an order of magnitude above our normal level of discourse, leading us to think that there is a raw nerve among Americans when it comes to home prices.

Here is the Chrisman excerpt:

|

I found this note sent to me a few years ago by John Hudson by Roy DeLoach of the DC Strategies Group titled, "Hang-in there, Millennials - The New Sub-Prime Mortgage Wave Is Coming." Roy is a former CEO of the National Association of Mortgage Brokers. "Hang in there, Millennials and all you other wanna-be first-time buyers still residing in Mom's basement. The Federal Reserve, Fannie Mae and Freddie Mac could soon be riding to your rescue. Well, not just your rescue, but perhaps more importantly, to save the economy, too. Which is the real reason they want you to take your 'rightful' place in the chain of life known far and wide as the 'Housing Ladder.' "Actually, Fed Chairwoman Janet Yellen is perplexed 'why so many Millennials choose to rent' rather than purchase a home. There was a collective chuckle in the room when I heard her make that statement at a recent House Financial Services Committee hearing. I only pray there are some in Washington who are not only not as confused as the Fed Chair, but also are seeing the very same statistics I am looking at and coming up with the same answer. The way I read the tea leaves, housing is in deep trouble and will likely fall apart sometime in late spring 2016 -- just in time to become an election year issue." |

In terms of housing market operating dynamics, De Loach was accurately describing the internals in the world of lending and servicing residential loans. But like many of us in the industry, he could not know just how high the Fed’s bond market manipulation via QE would take home prices.

In the new edition of The IRA Bank Book, we describe the continued distortion of credit loss metrics in both residential and multifamily asset classes. Eventually, these metrics will revert to the mean and beyond.

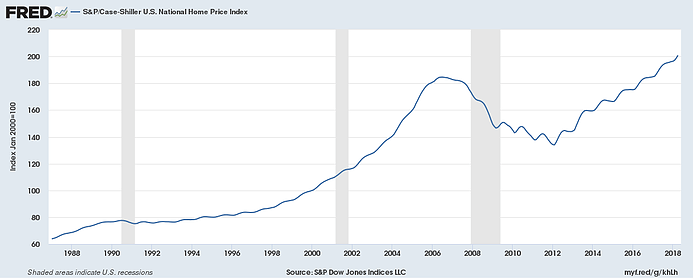

The importance of the fact that US bank credit metrics are showing essentially zero cost in residential lending from portfolio loans is that it begs the question as to home price valuations and thus loan-to-value (LTV) ratios. A number of analysts have predicted an imminent reset in terms of home prices, but this has not happened for several reasons. The chart below shows the Case-Shiller average for US home price appreciation.

First, real estate is a local market, so generalizations such as Case-Shiller are dangerous. New York City has been slumping for the past two years, but other markets around the country such as Denver remain hot. The work of Weiss Residential Research clearly shows a turn in some major urban markets that have been moving higher since 2012 and before. But these moves seem more a function of buyer exhaustion than a permanent move to a buyers market. They key factor is cheap money chasing a limited supply of homes.

Second, the US home market is in a classic supply squeeze. Referring to the work of Laurie Goodman at Urban Institute, the US is adding less than 1 million new units per year net of attrition of obsolete homes. Basically, new household formation is 50% higher than the growth in new housing units. More, the Fed’s manipulation of interest rates and credit spreads encouraged Wall Street to allocate capital to buying residential homes as rental properties, further limiting supply of homes available for sale.

Net, net, Millennials have been priced out of the housing market because the omniscient souls on the Federal Open Market Committee think that boosting asset prices will lead to more spending and job creation. Instead, low interest rates and help from the GSES (Fannie, Freddie and Ginnie) have driven up home prices beyond the reach of many home owners in major metro areas. Ed Pinto and Paul Kupiec wrote in The Wall Street Journal in March 2018:

|

“Since mid-2012, real home prices have increased 28%, according to data from the American Enterprise Institute. Entry-level home prices are up about double that rate. In contrast, over the same period household income has barely kept pace with inflation. The current pace of home-price inflation is increasing the risk of another housing bubble.” |

Lenders will be happy to hear that home owners are not even tapping the increased equity in their homes as in the 2000s, one reason why home equity loans (HELOCs) continue to shrink by double digits as a bank asset class. CNBC’s Diana Olick had a good segment “More homeowners leaving home equity untapped” on Monday.

Given the Yellen Inflation in home prices, the question for lenders, of course, is how much to discount home prices over a 15 or 30 year time horizon? This week we got to sit with one of the leaders of the mortgage finance world. The conversation eventually turned to credit. The consensus was that a recession in 2020 was not necessarily going to bring significantly elevated credit loss rates, but that by the mid-20s credit costs would be rising appreciably.

We continue to point to 2015 as the trough for credit costs at US banks generally and note that more normal portfolios like commercial and industrial loans (C&I) are showing rising defaults and loss rates, what you would expect at the end of a Fed-induced boom. But meanwhile in the world of mortgage finance, things are anything but normal. Just look at the intense competition among JPMorgan (JPM) and the other megabanks for non-bank fiduciary balances in the commercial deposit market.

The FOMC has indicated that short-term interest rates are rising, but long-term benchmark rates such as the 10-year Treasury bond are falling. Because of this move in long-term yields, modeled valuations for mortgage servicing rights (MSRs) will likely fall this quarter, requiring “fair value” adjustments to capital and income.

Meanwhile, MSRs are trading in the secondary market at record cash flow spreads, in excess of 5.5x annual cash flow for conventional servicing. And the cost to originate and service loans has never been higher. If this environment of extraordinary high prices and low operating spreads is intended to be helpful to the housing finance sector, then we respectfully suggest that our friends on the FOMC ought to think again.

Sadly, even as home prices have surged, none of the FOMC’s promised benefits have materialized when it comes to jobs, income or overall GDP growth. Indeed, the increase in home prices has locked-in many empty nesters in states like CA and NY. The big question: Is the Yellen Inflation in home prices permanent?

EDITOR'S NOTE

Christopher Whalen is Chairman of Whalen Global Advisors LLC. He has worked in politics, at the Federal Reserve Bank of New York and as an investment banker for more than 30 years. He is the author of three books Inflated (2010), Financial Stability (2014) and Ford Men (2017).

In 2017, he resumed publication of The Institutional Risk Analyst and contributes to many other publications and media outlets. He recently launched the first volume of The IRA Bank Book, a review of the operating and credit performance of the US banking industry written for institutional investors.