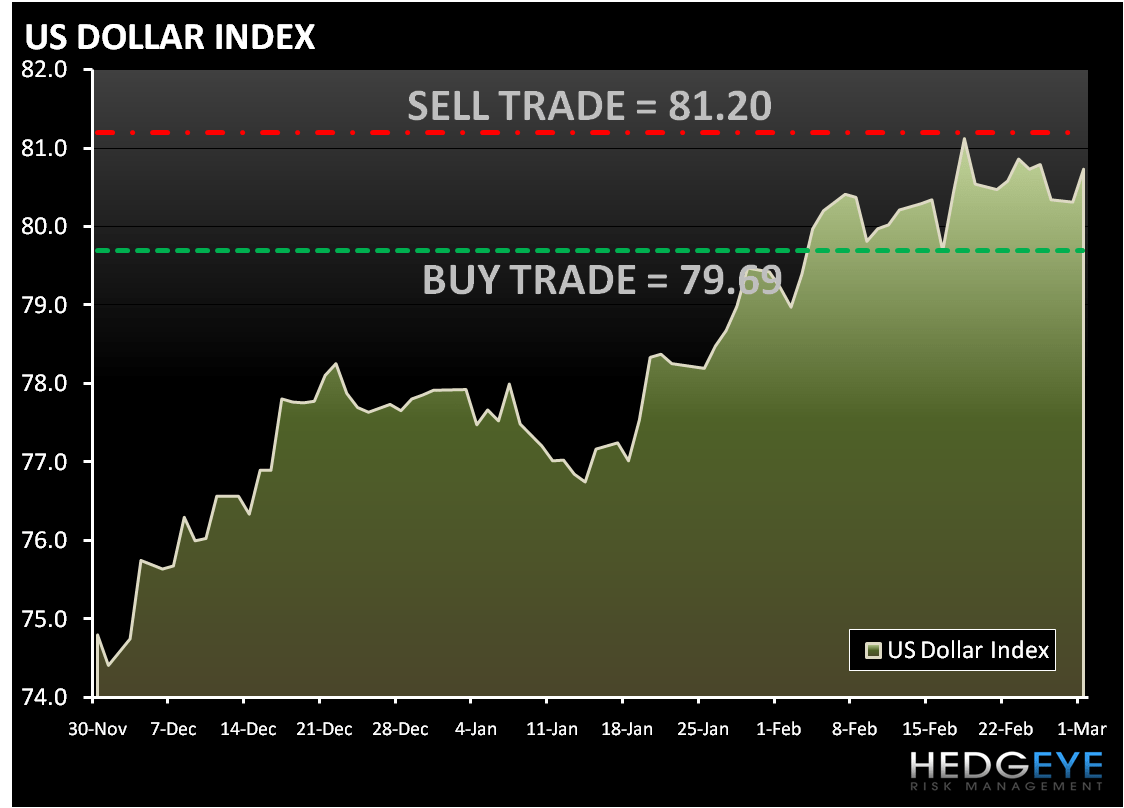

On Friday, the S&P 500 US equities finished slightly higher, capping off a down week for the Dow -0.7%, S&P -0.4%, NASDAQ -0.23% and Russell -0.5%. From a MACRO perspective, issues surrounding the momentum behind the global RECOVERY trade remain in place, with a continued focus on weaker-than-expected economic data out of both the US and the Eurozone. Despite this, the dollar index was slightly lower last week declining 0.35%. Today’s set up based on Hedgeye Risk Management models have levels for the Dollar Index (DXY): buy Trade (79.69) and sell Trade (81.20).

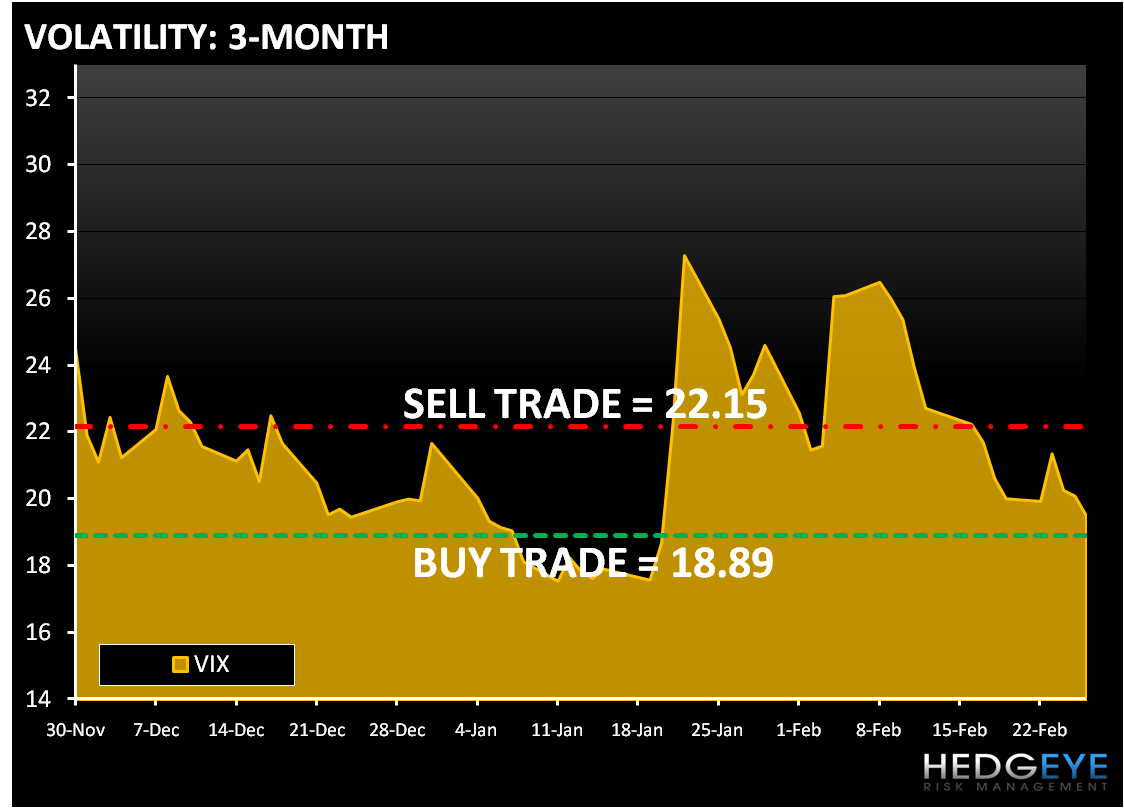

The RISK trade unwound last week with the VIX declining 2.6% and declined 20.8% for the month of February. Today’s setup for the volatility Index (VIX) is buy Trade (18.89) and sell Trade (22.50). As we posted on Friday, on March 9th, Greece’s Prime Minister will be visiting the USA. In addition to meeting with Merkel in Germany on March 5th this, on the margin, is another bullish catalyst for Greek stocks (bearish for Greek CDS and bond yields) which look poised to make a series of higher-lows in the coming weeks. “Fashionable Fears” are now locked in with Friday’s fears associated with a Moody’s downgrade (see our Early Look note from 2/26/10 for a more detailed analysis of the same).

As we wrote about last week there are some MACRO headwinds that can’t be ignored; a pickup in bank failures, continued excess inventories in the semi-conductor space, jobs, state budget pressures and reports of additional efforts to curb lending growth in China. The mitigating factors are the free money Fed policy, a continued pickup in M&A, well-received Q4 earnings, and 2010 guidance out of the retail space.

Last week, Europe dominated the MACRO headlines. The global recovery theme was called into question after Germany's Ifo business climate index unexpectedly fell in February for the first time in 11 months. In addition, Greek downgrade warnings from both S&P and Moody's made lots of headlines, but is a lagging indicator.

In the US, news on the consumer and housing were an addition headwind for the market. Our bearish stance on housing is expressed through our short in TOL which declined 1.72% last week and 5.2% over the past two weeks. Other builders such as LEN (5.2%), PHM (5.3%), RYL (4.7%) and DHI (4.6%) were also very weak. New home sales plunged 11.2% month-to-month in January to a record low 309,000 unit annualized pace, while existing home sales fell 7.2% last month following a 16.2% decline in December. It also should be noted that, mortgage applications fell 8.9% for the week ended February 19th, the third straight decline. Purchase applications fell 7.3% following declines of 7% and 4% in the prior two weeks, pushing the purchase applications index down to levels not seen since 1997.

Last week there were only two sectors with positive performance, Consumer Discretionary (XLY) and Financials (XLF). The XLY benefitted as Retail had a very strong relative outperformed last week, with the S&P Retail Index +1.9%. Better-than-expected Q4 earnings and increasingly upbeat outlook for 2010 helped to underpin the group last week. This outperformance came despite some continued headwinds facing the US consumer, as February consumer confidence plunged 10.5 points to 46, the lowest level since April. Expectations fell to a seven-month low, while the current conditions index hit its lowest level since early 1983.

As we wake up today, Asian and European markets rose this morning as worries about Greece subsided. Resources stocks went up as copper prices surged after the earthquake in Chile. Chile is the world’s largest country producing copper. US Equity futures are trading above fair value but well below the highs as European markets pare earlier gains.

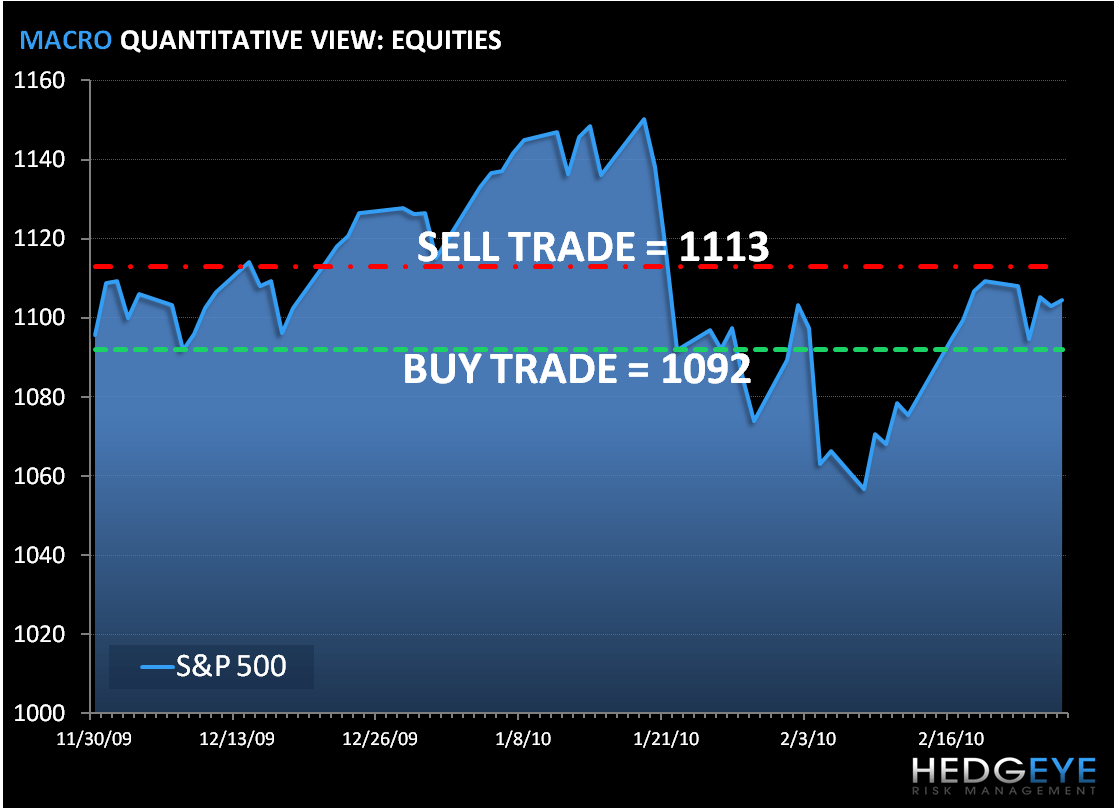

On the MACRO calendar today we will see January personal Income/Spending, PCE Deflator, February ISM and January Construction Spending. As we look at today’s set up the range for the S&P 500 is 21 points or 1% (1,092) downside and 0.8% (1,113) upside.

Copper jumped to the highest price in five weeks in London after a magnitude-8.8 earthquake disrupted supplies from Chile, the world’s largest producer. The Hedgeye Risk Management Quant models have the following levels for COPPER – Buy Trade (3.18) and Sell Trade (3.38).

Gold declined in London as the dollar extended gains against the euro. The Hedgeye Risk Management models have the following levels for GOLD – Buy Trade (1,097) and Sell Trade (1,124).

Crude oil rose for a second day on expectations that economic growth in the U.S. will boost fuel demand. The Hedgeye Risk Management models have the following levels for OIL – Buy Trade (77.10) and Sell Trade (81.09).

Howard Penney

Managing Director