“Appreciate the art of thoughtful disagreement.”

-Ray Dalio

When the macro market disagrees with your positioning, what do you do? Do you have an accurate forward growth and inflation outlook that you can depend on? Can you engage in a thoughtful disagreement with yourself and/or your teammates?

As Dalio goes on to preach in Principles, “when two people believe opposite things, the chances are that one of them is wrong. It pays to find out if that someone is you.” (pg 190)

I’ve been wrong plenty of times over the course of the last decade building this team and customer facing risk management #process. But I get paid to not stay wrong. Clients pay us to augment their #process with a data driven and dispassionate one.

Back to the Global Macro Grind…

Fortunately, my immediate-term signaling #process had me sell my long position in the Nasdaq’s QQQ’s at 10:06 AM EST yesterday. That’s the #timestamp. The NASDAQ was green at that point. It proceeded to drop -2% from there into the close.

Oh you’re so sweet. Not really. The way I see it is that this is all about the transparency of the #process. If I don’t have a real-time and accountable track record of #timestamps, I have no business being in the market-timing business.

*we have 4,111 transparent, timestamped market signals since 2008

Since market-timing are two very dirty words for people who are bad at it, you can imagine what they might think about timing the economic cycle! I’d be more than happy to sit down with anyone who’d like to have a thoughtful disagreement about this.

Moving along, today is Macro Themes Day @Hedgeye!

In our Q3 Macro Themes presentation at 11AM ET, we’ll walk through the Top 3 Global Macro Themes that we are:

- Measuring and mapping as becoming more probable… that

- Consensus still isn’t fully positioned for (i.e. consensus considers them improbable)

Especially when consensus is leaning one way and our #process is signaling a Phase Transition in the other direction, timing growth and inflation cycles can really help money managers separate their performance outcomes from the crowd’s.

Per Darius Dale’s summary, our Q3 Macro Themes are as follows:

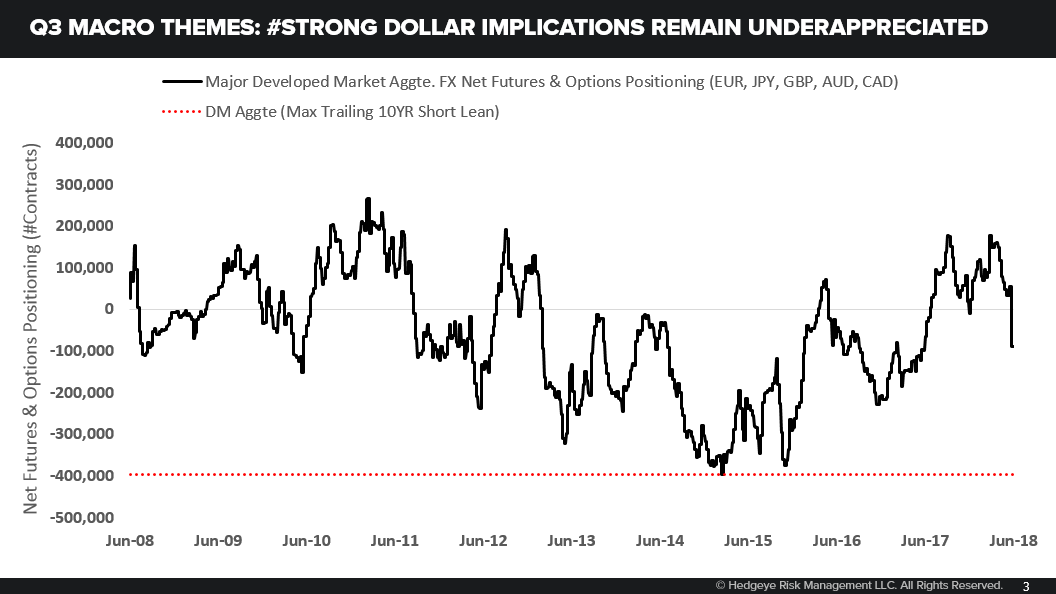

- #Strong Dollar: A U.S. Dollar Index +7% off its YTD lows has already inflicted some major pain in consensus macro views that were observably long of things like commodities and emerging market financial assets heading into Q2. Moreover, our proprietary GIP-modeling process for all of the world’s major economies signals that the global trend of decelerating growth is just getting started – an outcome that is likely to increasingly drive inflows into dollar-denominated assets. We will dig into the wide-reaching implications of further USD strength that investors can’t afford to miss, from emerging market USD-denominated credit risk to corporate profit deterioration.

- #HaveRatesPeaked?: With a peak in domestic headline inflation pending in Q3, 4 hikes out of the FOMC now priced in for 2018, DM sovereign yields retreating alongside the more discrete manifestation of #GlobalDivergences (i.e. broad slowing across Europe, China and EM) and 10yr Yield and Ag are signaling lower-highs, the consensus “bond bear market” thesis is likely to find itself under increasing scrutiny as we progress throughout 2H18. We’ll review prevailing conditions, detail emerging dynamics and discuss how we’ll be risk managing rates and rate-sensitive equity exposure in the upcoming months.

- #ShortEM: The first half of 2018 saw a tremendous pickup in cross-asset volatility – albeit from at/near all-time lows – throughout the emerging market investment universe. With explanations of what caused this market event as numerous as the number of strategists who didn’t see it coming and as bountiful as those that are calling for it to end purely as a function of “attractive valuations”, we don’t believe our bearish bias on EM is fully priced in. As such, we will anchor on the findings of our proprietary, repeatable and robust processes to detail to investors why EM assets are likely to continue to be a drag on fund performance with respect to the intermediate term.

While there are plenty of market participants who have disagreed with our 2018 Macro Themes of #GlobalDivergences, #ChinaSlowing, #EuropeSlowing, #EMSlowing, #StrongDollar, etc., Mr. Market has not.

In fact, the further away you get from being long the US Dollar and pure plays on late-cycle US consumption, profits, and capex exposures, the more obvious the under-performance of global equity, credit, and currency exposures becomes.

That’s why the Dow (an internationally affected index), Industrials (XLI), and Financials (XLF) have all broken down to Bearish @Hedgeye TRENDs in the last 2 weeks. It’s probably why the SP500 broke to Bearish @Hedgeye TREND in the last 24 hours too.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND views in brackets) are now:

UST 10yr Yield 2.82-2.95% (bullish)

SPX 2 (bearish)

RUT 1 (bullish)

NASDAQ 7 (bullish)

Energy (XLE) 73.06-76.25 (bullish)

REITS (VNQ) 78.88—81.52 (bullish)

Industrials (XLI) 70.43-73.04 (bearish)

Nikkei 22101-22523 (bearish)

DAX 12071-12583 (bearish)

VIX 13.17-18.93 (bullish)

USD 93.79-95.12 (bullish)

Oil (WTI) 66.30-72.96 (bullish)

Copper 2.94--3.08 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer