The guest commentary below was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

During our fishing trip to Leen's Lodge last week, there was a lot of discussion about the markets and whether the Fed is going to successfully manage the return to normalcy. Our bet on that question is “no” as we noted in a missive yesterday by Jeff Cox of CNBC, “The Fed's effort to control the rise of its key interest rate is running into some problems.”

Dr. George Selgin of Cato Institute has a timely new paper appropriately entitled "Floored" that discusses this issue of the FOMC using interest on excess reserves as a “floor” for the Federal funds rate. In the paper, Selgin talks about “how the Fed’s floor-system experiment came about, what its intended and actual consequences have been, and why either the Fed itself or Congress should bring the experiment to an end as rapidly as can be done without causing further economic damage.”

Instead of reviving the private market for Fed Funds, the FOMC has used Basel III and paying interest on excess reserves or “IOER” to turn the trading of short term funds into a lab experiment. Instead of creating a traditionl “corridor” system for managing short-term rates, with IOER near the bottom of the policy range and the discount window rate at the top, the FOMC opted for a more radical experiment. Selgin notes:

|

“Had [the FOMC] actually employed interest on reserves to establish a proper corridor system, as it planned to do in 2006, and even had it allowed interest to be paid on excess reserves with that aim alone in mind, paying interest on reserves wouldn’t have constituted a radical change. But as we shall see, when the Fed actually put its new tool to work, a corridor system was no longer what it had in mind.” |

Selgin cites some revealing passages from former Fed Chairman Ben Bernanke, who justifies the need for paying interest on excess reserves to prevent interest rates from falling too low. “[By] setting the interest rate we paid on reserves high enough, we could prevent the federal funds rate from falling too low, no matter how much [emergency] lending we did,” stated Bernanke in 2015.

Was Bernanke’s comment an admission that negative rates are as a general matter undesirable? Perhaps. Selgin notes: “Although they were keen on providing emergency support to particular firms and markets, Fed officials recognized no general liquidity shortage calling for further monetary accommodation. The challenge, as they saw it, was that of extending credit to particular recipients without letting that credit result in any general increase in lending and spending…. for the most part the Fed was counting on IOER to encourage banks to accumulate excess reserves instead of lending them.”

Selgin’s paper makes clear that the FOMC had no firm idea how the use of IOER as a floor for interest rates would impact the markets and the US economy. In particular, the idea of using IOER as a way to dissuade banks from lending illustrates the speculative and, indeed, irrational nature of FOMC deliberations. As the renowned physicist Richard Feynman states: “It doesn't matter how beautiful your theory is, it doesn't matter how smart you are. If it doesn't agree with experiment, it's wrong. In that simple statement is the key to science.”

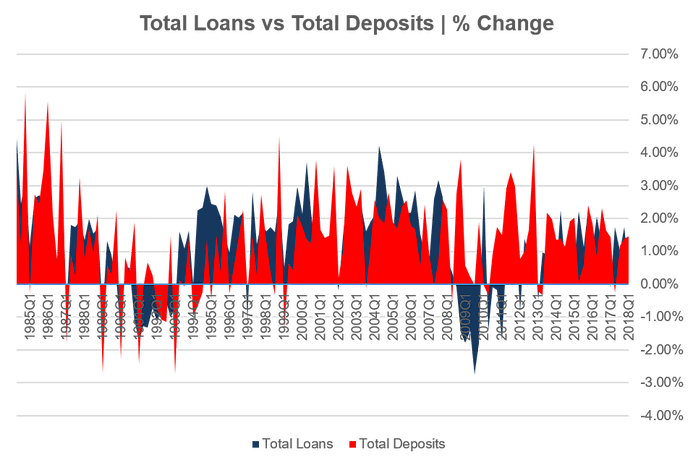

But of course economics is not a science, a fact illustrated by the Fed’s decision to pay IOER in combination with massive open market purchases of Treasury paper and mortgage backed securities. There is some support for the idea that the decision by the Fed to use IOER as a floor for interest rates negatively impacted bank lending and economic growth, as shown in the chart below.

There are many factors affecting the growth rate for loan portfolios, but what the data from the FDIC clearly suggests is that the surge in bank deposits seen from 2012 onward was not matched by a commensurate increase in bank lending. Also, as we’ve discussed previously, sales of loans by US banks have declined 10 fold since the mid-2000s. Again, Selgin:

|

“The Fed’s decision to switch to a floor system at a time when equilibrium market interest rates were collapsing, and to do so with the aim of propping-up its policy rate to keep it above the zero lower bound, contributed to the severity of the recession, while limiting the Fed’s options for promoting recovery. Thanks to it, the U.S. economy has been in the grip of an above-zero liquidity trap since the trough of the Great Recession.” |

Although the impact of the Fed’s policies with respect to paying interest on excess reserves has generated a great deal of debate in the economics community, the other aspect which has received far too little attention is how quantitative easing impacts long-term interest rates. The Federal Open Market Committee was sold a bill of goods by the staff of the Board of Governors and FRBNY chief Bill Dudley.

Specifically, we hear that Simon Potter, Head of the Markets Group at the Federal Reserve Bank of New York, (and Dudley) told the FOMC that they could hold any quantity of reserves indefinitely as long as they could do reverse repo operations to set a rate floor to accompany the ceiling rate system (interest on excess reserves or IOER). The Potter-Dudley assertion that short-term REPOS can suffice to manage any amount of excess reserves seems to be refuted by experience, however, especially given the combination of IOER with aggressive open market operations (aka “QE”).

“The correct strategy all along would have been for the Committee to pause at 1.5% for Fed funds (2 hikes ago),” notes former Fed researcher officer Walker Todd. “The Fed could then begin to sell off the mortgage backed securities until the resulting long end rate increases began to put upward pressure on the Fed funds rate. Then the Fed would be in the more comfortable situation of following the market upward instead of trying to lead against market résistance, which is what is happening now.”

As Chairman Powell and the FOMC raise the interest rate floor, the size of the Fed’s portfolio seemingly prevent long-term interest rates from rising. The securities holdings of the Fed and other global central banks are entirely passive, with no trading or hedging operations to influence long rates to rise, thus the spread between short term rates and longer maturities is shrinking rapidly. Unless the FOMC relents and starts to actively manage longer-term rates by selling securities and/or swaps and futures, the Treasury yield curve is likely to invert by year-end.

In the event, the financial markets will react negatively and force the FOMC to delay any further rate hikes until long-term interest rates actually start to rise of their own volition. Until then, the short-term liquidity trap created by the Fed’s misuse of IOER will be a continued obstacle to policy normalization, on the one hand, while the Fed’s massive QE portfolio will act as a cap on long-term bond yields. And the FOMC has yet to admit publicly that they indeed have a problem of their own special creation.

EDITOR'S NOTE

Christopher Whalen is Chairman of Whalen Global Advisors LLC, a Wall Street insider who understands the intersection of politics and finance, and says what he means. He has worked in politics, at the Federal Reserve Bank of New York and as an investment banker for more than 30 years. He is the author of three books Inflated (2010), Financial Stability (2014) and Ford Men (2017).

In 2017, he resumed publication of The Institutional Risk Analyst and contributes to many other publications and media outlets. He recently launched the first volume of The IRA Bank Book, a review of the operating and credit performance of the US banking industry written for institutional investors.