Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

Today's Focus: June Builder Confidence

It’s difficult to discern whether the modest backslide in the HMI in recent months represents a trend inflection in confidence and a harbinger of forward activity or a reflection of fringe dynamics that are impacting sentiment at the margin but are running parallel to and somewhat independent from underlying fundamentals.

Mortgage rates are up (but sovereign yields are signaling lower-highs), lumber prices are up big YTD (but they’ve been falling recently), tariff tension is rising but we’re already (arguably) on the game theoretic line between skirmish (politically positive ahead of midterms) and war (negative), Purchase Application volume is down but household incomes are rising and supply-constrained volume growth in the existing market has been an entrenched reality for two years at this point.

Suffice it to say, precision parsing of the above is quixotic and unnecessary as the common sense interpretation comports just as nicely:

We are now -6pts off the cycle peak in Builder Confidence of 74 registered in December. And so long as rising raw material and input costs remain a headwind to margins, consensus remains short bonds and the specter of tariff escalation shadows the short-term outlook, it’s unreasonable to expect a breach to new highs in the HMI. It’s similarly premature to characterize the 1H18 retreat as signaling a veritable end of the housing cycle, particularly with the labor market continuing to tighten, mortgage credit availability still improving and unprecedented, late-cycle fiscal stimulus layered atop an already taut economy providing some domestic macro juice for a while longer.

For now, we’re content not to overanalyze shifting but largely sideways sentiment and look forward to the July release where we’ll also receive the updated annual survey data around extant lot and labor supply conditions among builders.

The Data:

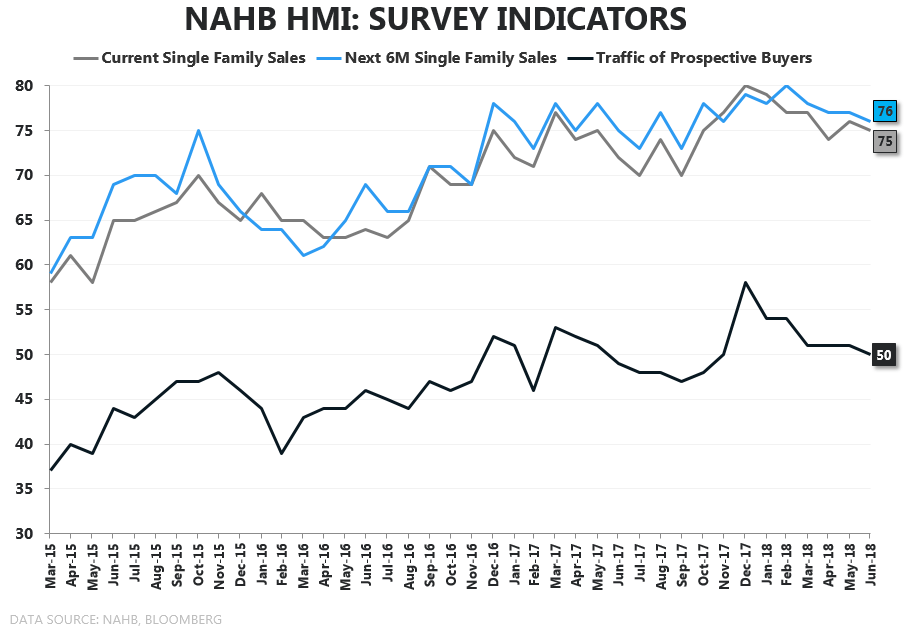

- Headline: Headline HMI fell -2pts to reading of 68 = -6pts of the cycle peak of 74 in December but largely flat with readings over the past 4 months.

- Subindices: Current Sales, 6M Expectations and Current Traffic all fell one point in June

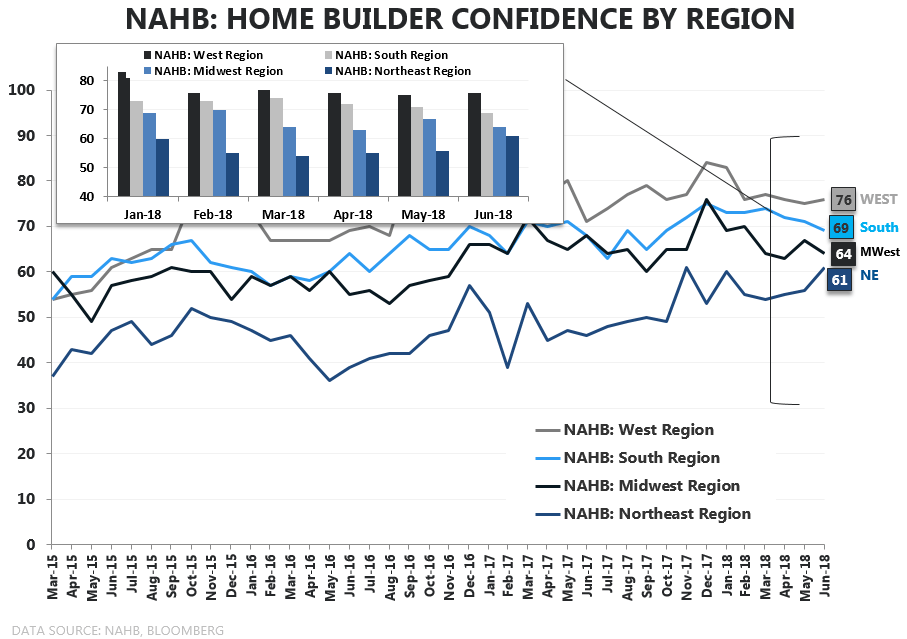

- Regional: Confidence in the South and Midwest regions fell -2pts and +3pts, respectively while rising +1pts and +5pts in the West and Northeast, respectively.

About the NAHB HMI:

The Housing Market Index (HMI) is based on a monthly survey of NAHB members designed to take the pulse of the single-family housing market. The monthly survey has been conducted for 30 years. The survey asks respondents to rate market conditions for the sale of new homes at the present time and in the next 6 months as well as the traffic of prospective buyers of new homes. The HMI is a weighted average of separate diffusion indices for these three key single-family series. The HMI can range from 0 to 100, where a value over 50 implies conditions are, on average, improving, a value below 50 implies conditions are worsening, and an index value of 50 indicates that the housing market is neither improving nor worsening.